Periods of change are uncomfortable, but they are rarely unprecedented. Markets, economies, and geopolitical landscapes often swing between extremes. As bottom-up, valuation-oriented investors focused on the long term, we look to understand the rules of the environment in which we are investing rather than predict the next shift. Horacia Naidoo-McCarthy offers a structured way to think about today’s investment landscape and the behavioural pitfalls that often accompany regime change.

“Mind the gap” is a famous safety warning used on the London Underground advising passengers to be careful of the gap between the train door and the platform edge. The familiar phrase is often used as a reminder to heed potential risks, differences or oversights, and navigate with care – a worthwhile warning in today’s investment environment.

In perpetual motion

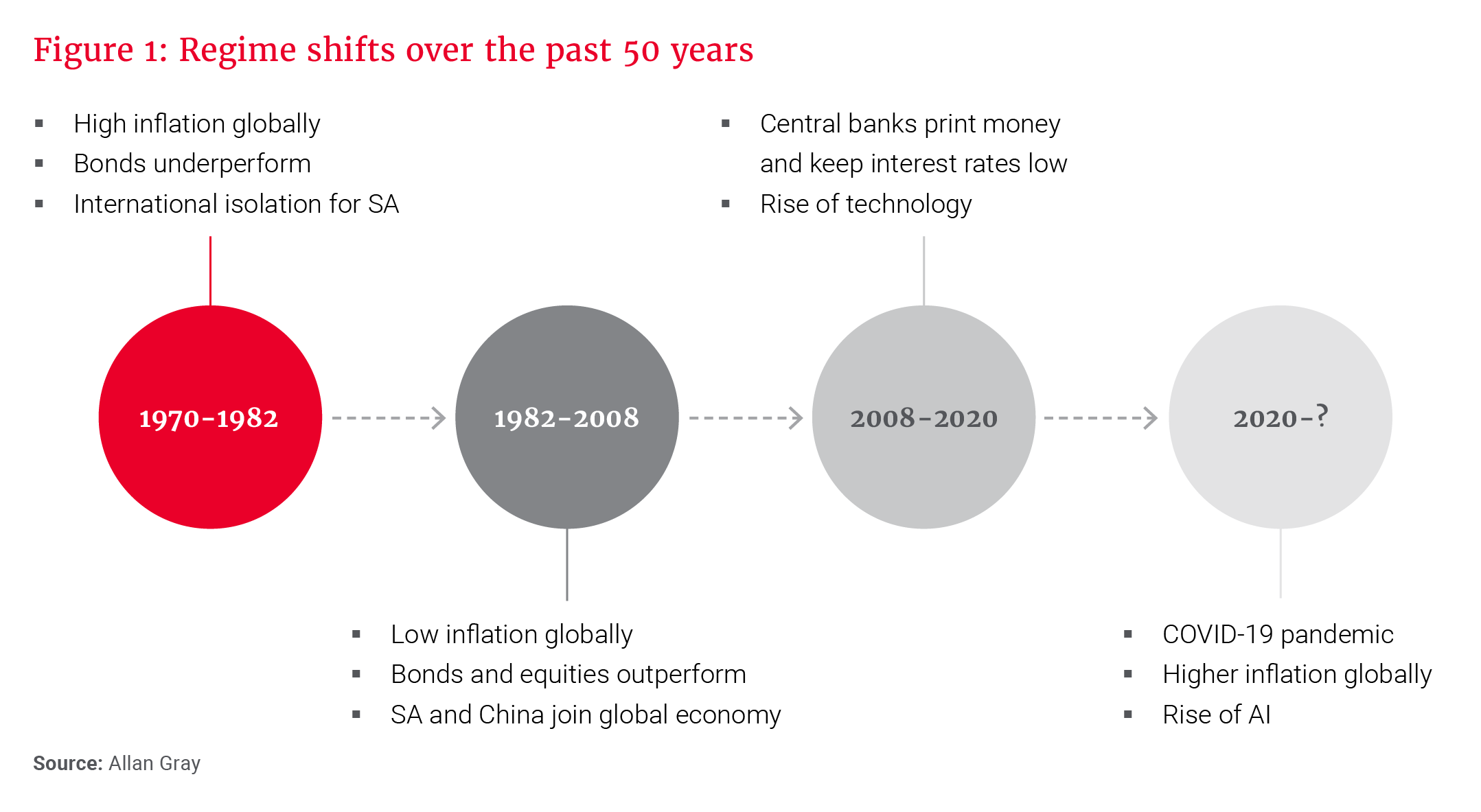

Change is a constant factor in life and investing, and while we know this intuitively, it nevertheless stirs up feelings of uncertainty. The investment environment is constantly shifting, as shown in Figure 1 below. The past 50 years have included times of high and low inflation, rising and falling bond and equity markets, and phases of global integration followed by fragmentation.

These shifts are not anomalies; they are features of long-term market history. Each market cycle brings new reasons to believe “this time is different”, yet the contributing factors – changing expectations, where money flows, and human behaviour – are similar. Recognising this can help investors avoid overreacting to short-term noise and remain anchored to long-term principles.

… markets do not reward prediction; they reward robust processes applied consistently over the long term.

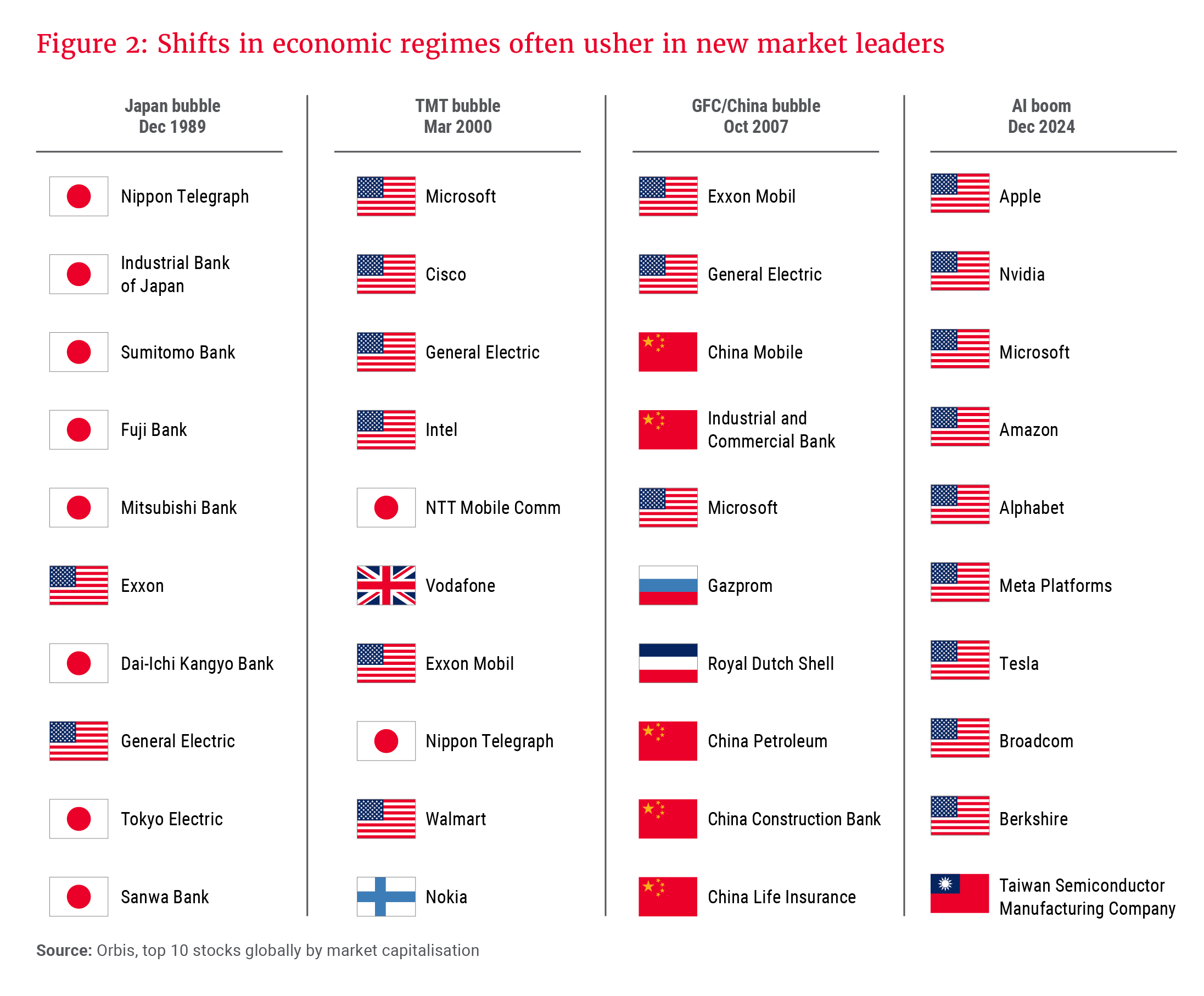

History shows regime shift is usually accompanied by the ascendancy of an asset, sector or geography. Looking back over the last 40 years or so, a pattern emerges: Market leaders in one cycle rarely dominate the next. As shown in Figure 2 below, over time, market leadership has rotated from Japanese financials during the late-1980s bubble to US technology during the technology, media and telecommunications (TMT) era, to China-linked banks and commodities around the global financial crisis, and most recently to US megacap growth stocks during the AI boom.

The point of looking back is not to try to predict exactly what comes next, but to challenge the instinct to carry recent patterns forward without question – a common behavioural trap that can impact investor outcomes. Nshalati Hlungwane discusses some fascinating examples of investing through disruption in her piece.

Why do investors keep falling into the same behavioural traps?

Behaviour, shaped by recent experience and generational memory, often overrides data, history, and fundamentals. In today’s shifting environment, it is important to be aware of these behavioural biases and not succumb to them.

1. Recency bias in a shifting market environment

Investors tend to project today’s dominant themes into the future – not because the evidence supports it, but because human psychology leans towards continuity. Several forces in the current environment create fertile ground for this behavioural trap:

Persistent inflation and higher-for-longer rates

For much of the last four decades, investors have been accustomed to global inflation and interest rates trending downwards. However, post COVID-19, inflation has proven to be stickier than expected, driven by geopolitics, policy choices, defence spending and supply constraints.

Rising inflation often leads to higher interest rates, and investors reasonably expect greater compensation for taking on more risk in holding shares. This is particularly true of companies whose earnings and profits are expected far into the future. This also means inflation does not affect all companies equally – some sectors, business models and countries are less vulnerable than others. Today, in the US, despite persistent inflation, stock market performance has been resilient, and this may reinforce the belief that “this time is different” when the underlying trend may be reversing.

US exceptionalism and market concentration

2025 was the first year since 2017 that markets outside the US outperformed the US. Nevertheless, the MSCI World Index remains dominated by a narrow group of US megacap tech stocks, as shown in Figure 2. Concentration has skewed index performance, widening the gap between prices and fundamentals, and has been further amplified by passive flows. This exceptionalism has spilled beyond markets into foreign policy, further entrenching the belief that the US is uniquely insulated from global pressures.

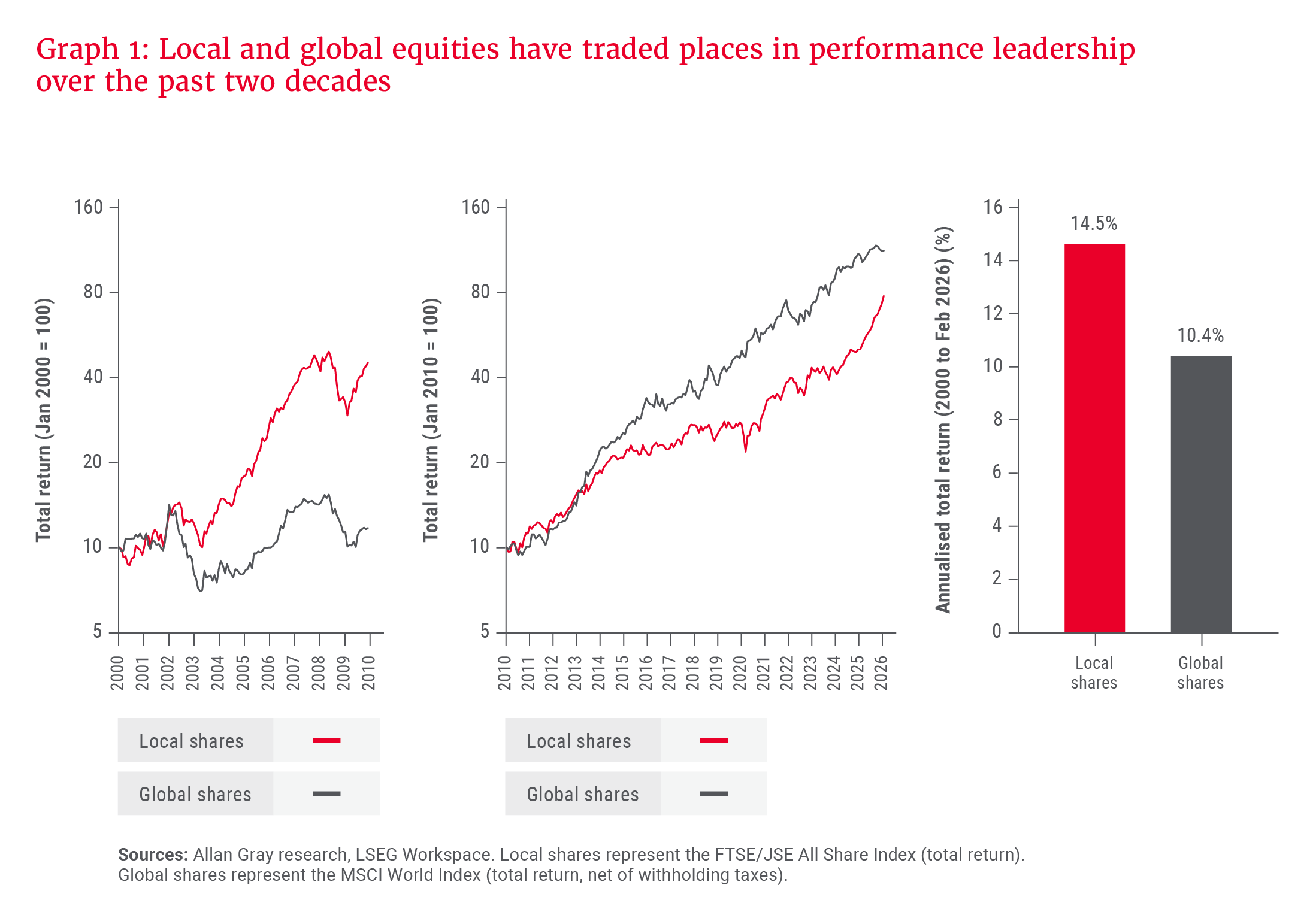

South African investors favour global over local equities

The exceptional run in US equities has anchored expectations of what “normal” returns look like. Over and above the performance, given the relatively small size of the South African market, the inherent local risks and the fact that many sectors and companies are simply not available, South African investors see offshore markets as superior.

While global shares have indeed outperformed local shares over the last decade and a half, and the other factors cannot be ignored, the prior decade tells a different story, suggesting there is opportunity for considered stockpicking. From 2000-2010, local shares, largely driven by the global commodities boom and supportive foreign flows, outperformed global shares. This culminated in local shares outperforming global shares by 4.1% over the longer than two-decade period, as shown in Graph 1.

A reconfigured global order

COVID-19 exposed supply chain vulnerabilities and accelerated deglobalisation. Geopolitical tensions, tariff cycles and multiple conflicts have deepened fragmentation. Meanwhile, AI is reshaping global power dynamics – shifting influence towards data, computing infrastructure, semiconductor control, and the ability to set technological standards. It is not just a technological development – it is a structural force accelerating geopolitical divergence.

The behavioural takeaway: When markets appear resilient despite rising fragility, recency bias thrives. Investors focus on what has worked – US tech, offshore exposure, concentration – and underplay the possibility of regime change. Index-level strength can mask increasing vulnerability.

2. Generational anchoring: Why lived experience shapes risk perception

Best-selling author and investor Morgan Housel notes that people’s understanding of risk is shaped less by theory and more by the era they grew up in. Research also suggests that the economic and market conditions people experience early in their working lives can shape what different generations come to regard as “normal”. These mental reference points tend to persist over time and can meaningfully influence investor behaviour. The lived experiences of different age groups are reflected in Figure 3.

Two investors, two realities

A 48-year-old today, who entered the workforce in 2001 when the rand traded at R8 to the US dollar and who lived through the tech bubble, the global financial crisis and the deflation of the “everything bubble”, will naturally view volatility and currency moves differently from a 28-year-old, who has only ever known the rand to be around R17/US$ and a world dominated by US tech giants.

These lived experiences become default assumptions. They influence:

- what feels safe,

- what feels expensive,

- what feels like a risk, and

- what feels like opportunity,

even when long-term data tells a different story.

The behavioural takeaway: Generational memory is a powerful anchor. When left unexamined, it morphs into behavioural bias – especially in environments where historical patterns are breaking down.

How these factors influence investment decisions

The interplay between recency bias and generational anchoring is visible in how investors have allocated capital in recent years. These biases create illusions of inevitability, obscuring cyclical reality. There are many consequences:

- Opportunities in undervalued areas are overlooked in favour of popular, overvalued areas.

- Risk is underestimated where valuations are stretched, and overestimated where valuations have been punished, often due to poor sentiment.

- Investors misread the early signs of regime transitions, assuming that the status quo will endure indefinitely.

A valuation-driven approach aims to counter these biases by grounding decisions in fundamentals rather than narratives, momentum or generational assumptions.

Bridging the gap

Periods of uncertainty are not unprecedented; they reflect shifts in investment regimes where leadership rotates and familiar patterns lose relevance. How investors interpret these shifts depends heavily on recent and generational experience. When these go unchecked, they harden into biases that obscure opportunity and magnify risk.

By minding the gap … we position ourselves to invest thoughtfully through shifting regimes.

Ultimately, markets do not reward prediction; they reward robust processes applied consistently over the long term. Even a disciplined investment philosophy will experience periods of discomfort, and at times be wrong in outcome despite being right in process. History rarely follows the same script, yet it often revisits familiar themes, reminding us that resilience lies not in prediction, but in adaptability, the disciplined application of a consistent investment philosophy and a clear-eyed focus on fundamentals. By minding the gap – between past and present, experience and evidence, perception and reality – we position ourselves to invest thoughtfully through shifting regimes.

Explore more insights from our Q1 2026 Quarterly Commentary

- 2026 Q1 Comments from the Chief Operating Officer by Mahesh Cooper

- Investing through disruption: Lessons from history for the age of AI by Nshalati Hlungwane

- Dis-Chem: A great business at a great price? by Jonty Fish

- Pan African Resources: The golden goose? by Andrew Boulton

- Higher discretionary allowance: The opportunity to invest more offshore by Daniel van Andel

- Orbis Global Equity: The art of adaptability in turbulent markets by Ben Preston

- Maximising new tax benefits to boost long-term investment outcomes by Shaun Duddy

To view our latest Quarterly Commentary or browse previous editions, click here.