The 2026 National Budget, delivered on 25 February, offered good news for investors, with no major tax increases and stronger-than-expected revenue collection. National Treasury introduced measures designed to encourage long-term investing, including an increase in the annual tax-free investment (TFI) contribution limit, an upward bump in the tax-deductible retirement fund contribution limit, and the doubling of the single discretionary allowance for offshore investing. In addition, all income tax brackets, thresholds and rebates were adjusted for inflation, offering welcome real relief after two consecutive years of unchanged tax tables. Shaun Duddy homes in on the TFI and retirement fund limit increases, explaining how they create meaningful opportunities for investors to take practical steps to strengthen their long-term investment outcomes.

From 1 March 2026, you can contribute up to R46 000 per year to a TFI, up from R36 000 previously, although the lifetime contribution limit remains unchanged at R500 000. At the same time, investors can enjoy an additional tax break on retirement fund contributions, with the annual cap increasing from R350 000 to R430 000.

… now is an opportune time to review your personal budget and financial plan and assess whether you can take advantage of any of the recent changes.

While monthly expenses can sometimes make it difficult to take advantage of these increased limits, if you do have space in your budget, or receive an unexpected windfall, these changes make a big difference over time. Specifically, they allow investors to allocate capital earlier and access tax benefits sooner. Over the long term, additional time in the market can have a meaningful impact on investment outcomes.

Why tax matters for long-term investors

Investment returns are typically subject to various forms of tax. In a standard local discretionary unit trust investment, this may include interest taxed at marginal rates (subject to exemptions), dividends subject to withholding tax, and capital gains tax when assets are sold. Over time, these taxes reduce the amount of capital available for reinvestment. This lowers the base from which future returns compound, leading to materially different outcomes over long investment horizons.

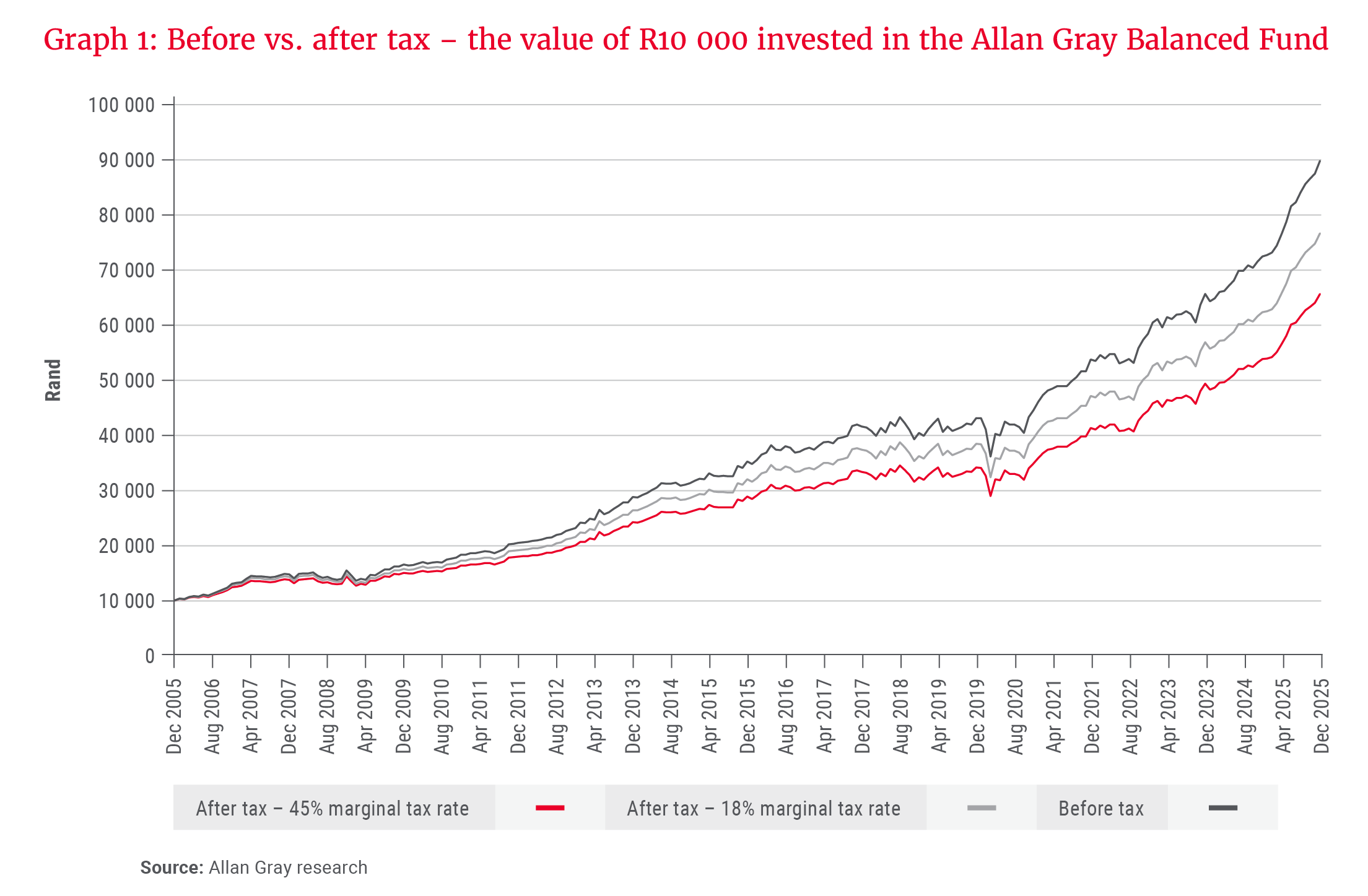

By way of example, consider Graph 1 below, which shows how an investment of R10 000 in the Allan Gray Balanced Fund at the end of 2005 would have grown to R89 587 (11.6% annual return) by the end of 2025 before tax. For an investor in the lowest marginal tax bracket (18%), the investment would have grown at approximately 10.7% per year to around R76 490 after applicable taxes. For an investor in the highest marginal tax bracket (45%), the same investment would have grown to only R65 487 over the same period (9.8% annual return) – a reduction of 26.9% overall or 1.7% per year.

Tax-efficient investment structures, such as TFIs and retirement funds, are designed to reduce or eliminate this drag, allowing a greater proportion of returns to remain invested and compound over time.

TFI contributions: The benefit of reaching your lifetime limit sooner

National Treasury introduced TFIs in 2015 to encourage higher levels of household savings in South Africa. These vehicles allow investors to earn returns free from tax on interest, dividends and capital gains, within specified limits. The increase in the annual contribution limit from R36 000 to R46 000 is the first adjustment since 2021.

As the lifetime limit has not been adjusted, the increased annual TFI contribution limit means that you are able to invest more every year and therefore reach your lifetime limit around three years earlier (in around 11 years rather than 14), giving your contributions more time to compound over the long term.

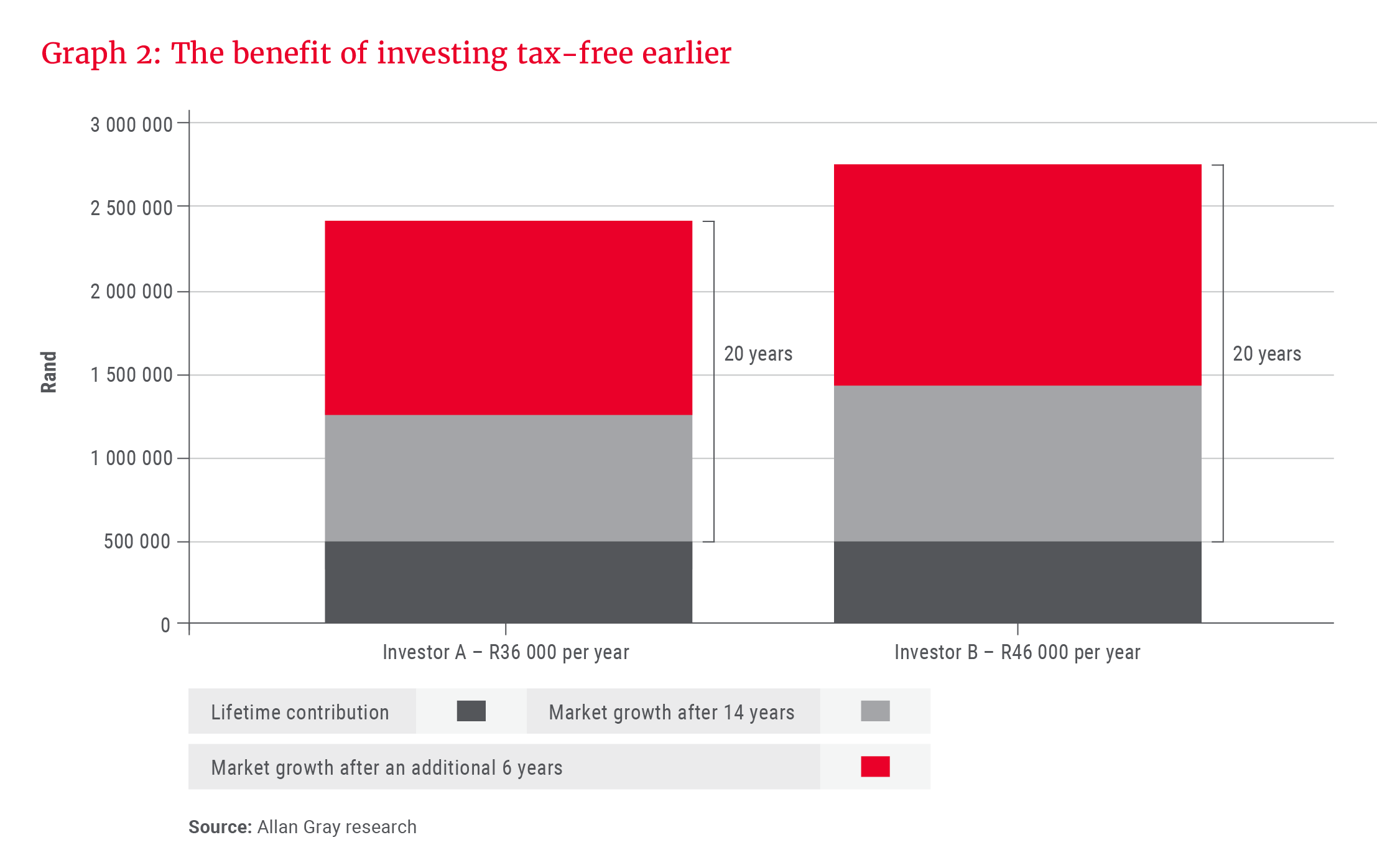

Consider two investors who both fully use the R500 000 lifetime limit and earn a return of 11.6% per year, in line with the Allan Gray Balanced Fund’s annualised performance over the 20 years ended 31 December 2025. Investor A contributes R36 000 per year and reaches their lifetime limit in just under 14 years, while Investor B contributes R46 000 per year and reaches their lifetime limit in just under 11 years.

As shown in Graph 2, despite contributing the same total amount, Investor B, who invested earlier, would have a portfolio value that is 13.8% higher after 14 years (approximately R173 080 more in rand terms), purely due to the compound effect of having contributed higher amounts earlier. This gap widens over longer periods of time, increasing to approximately R334 015 after 20 years.

The difference arises not from how much is invested, but from when it is invested. This illustrates the importance of time in the market as a driver of long-term outcomes.

Retirement fund contributions: The benefit of bringing forward tax relief

Contributions to pension, provident and retirement annuity (RA) funds are tax-deductible within prescribed limits (currently up to 27.5% of the greater of taxable income or total remuneration, subject to the annual cap), and returns within these products are not taxed while invested. These features make retirement funds a compelling proposition for long-term investors.

The increase in the annual monetary cap on tax-deductible retirement fund contributions from R350 000 to R430 000 is particularly relevant for higher-income earners (earning above R1.27m per year) who maximise their contributions, or those who previously contributed above the deductible threshold.

The new limit allows a greater portion of contributions to qualify for immediate tax relief.

Under the previous cap, contributions above R350 000 were treated as “excess contributions”, with the associated tax benefit carried forward to future years. This was covered in detail in Carla Rossouw’s piece last quarter, “The long-term benefits of maximising your retirement fund contributions”. The new limit allows a greater portion of contributions to qualify for immediate tax relief.

As with TFIs, the significance of this change also lies in timing. For example, consider an investor contributing R430 000 per year to a retirement fund. Under the old limit, only R350 000 of this amount would be tax-deductible in the same tax year, with the remaining R80 000 treated as an excess contribution. Under the new limit, the full R430 000 is deductible in the same tax year.

While deferred tax relief is not lost, its real value will likely erode over time due to inflation. Assuming an annual inflation rate of 5%, an excess contribution of R80 000 used only after 10 years would be worth just R49 113 in today’s terms. Accessing tax relief sooner preserves its real value.

Contributions made earlier in the tax year allow capital to benefit from tax-efficient compounding for longer.

Making effective use of tax benefits

The significance of the changes introduced in the 2026 Budget lies less in the absolute increases in limits and more in how they influence the timing of investment and access to tax relief – both of which can have a substantial impact on long-term outcomes.

The new tax year began on 1 March 2026, so now is an opportune time to review your personal budget and financial plan and assess whether you can take advantage of any of the recent changes. Contributions made earlier in the tax year allow capital to benefit from tax-efficient compounding for longer. TFI investors can benefit by using the R46 000 annual limit earlier in the year; retirement fund investors may consider how the higher deductible cap fits into their broader contribution strategy. Of course, budget constraints may not immediately allow this, but remember, even partial use, applied consistently over time, can be beneficial.

While tax-efficient structures offer clear advantages, they form only one part of a broader investment strategy. Factors such as liquidity needs, investment horizon, asset allocation and costs remain equally important in determining long-term outcomes.

Explore more insights from our Q1 2026 Quarterly Commentary

- 2026 Q1 Comments from the Chief Operating Officer by Mahesh Cooper

- Investing through disruption: Lessons from history for the age of AI by Nshalati Hlungwane

- Dis-Chem: A great business at a great price? by Jonty Fish

- Pan African Resources: The golden goose? by Andrew Boulton

- Higher discretionary allowance: The opportunity to invest more offshore by Daniel van Andel

- Orbis Global Equity: The art of adaptability in turbulent markets by Ben Preston

- Mind the gap by Horacia Naidoo-McCarthy

To view our latest Quarterly Commentary or browse previous editions, click here.