Finding great businesses at a fair price is not always easy, especially given that the resource and banking sectors currently dominate the FTSE/JSE All Share Index. However, our deep research process is designed to uncover opportunities. Jonty Fish shares why we believe Dis-Chem, one of the largest retail pharmacies in South Africa, meets the definition of a great business at a fair price, and potentially a great business at a great price.

It was Charlie Munger who famously said, “A great business at a fair price is superior to a fair business at a great price.”

What makes a great business?

There is not necessarily one definition, but broadly, a great business should have:

- A long runway for growth

- Stable or non-cyclical earnings

- High returns on capital, protected by a durable moat

- A sound balance sheet

- Strong free cash flow conversion

We believe Dis-Chem meets all five criteria and is in the process of strengthening an already solid position.

1. A long runway for growth

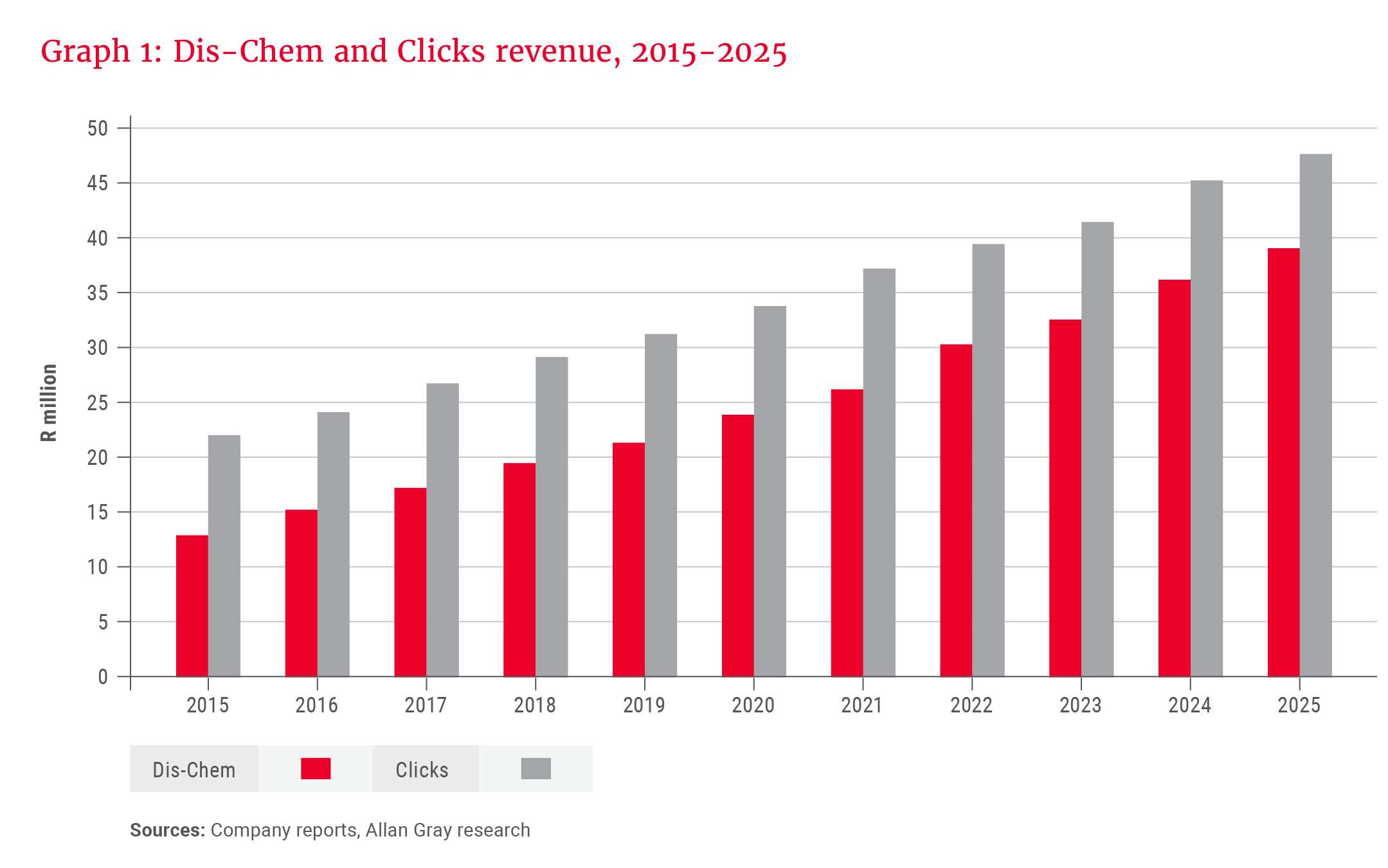

Since the pharmacy market was liberalised in South Africa in 2003, corporate pharmacies have grown market share rapidly. The two main players, Dis-Chem and Clicks, now make up about half of the total dispensary market, having squeezed out many of the smaller players. This consolidation has translated into strong and consistent revenue growth for both businesses. Over the past decade, Clicks has grown revenue at approximately 8% per annum. Dis-Chem, starting from a smaller base and effectively playing catch-up, has grown faster at 11.7% per annum over the same period, as illustrated in Graph 1.

There is reason to believe that this consolidation theme will continue well into the future, as it is incredibly hard for independent pharmacies to compete with large groups. Lack of scale to reinvest in price, low front-shop percentages (where higher-margin products are sold), no loyalty programmes, and no succession planning are just a few reasons why the consolidation theme should continue to play out.

Dis-Chem itself has large store roll-out plans. In 2023, it shifted its plans (partly as regulations changed) from opening roughly 20-25 new stores per year to 40-50 new stores per year, which will essentially double the store base by 2030. While execution has been slower than expected, there is still plenty of opportunity to increase the store base.

2. Stable or non-cyclical earnings

Pharmacy sales are generally resilient through economic cycles. Medicine is non-discretionary, and consumers are unlikely to reduce essential healthcare spending even when under pressure.

The front shop further enhances defensiveness, with a significant portion of sales coming from staple categories such as personal care, hygiene and cleaning products. This combination results in earnings that are more stable than those of many other retail formats. As shown in Graph 1, there are no negative swings in revenue.

3. High returns on capital, protected by a durable moat

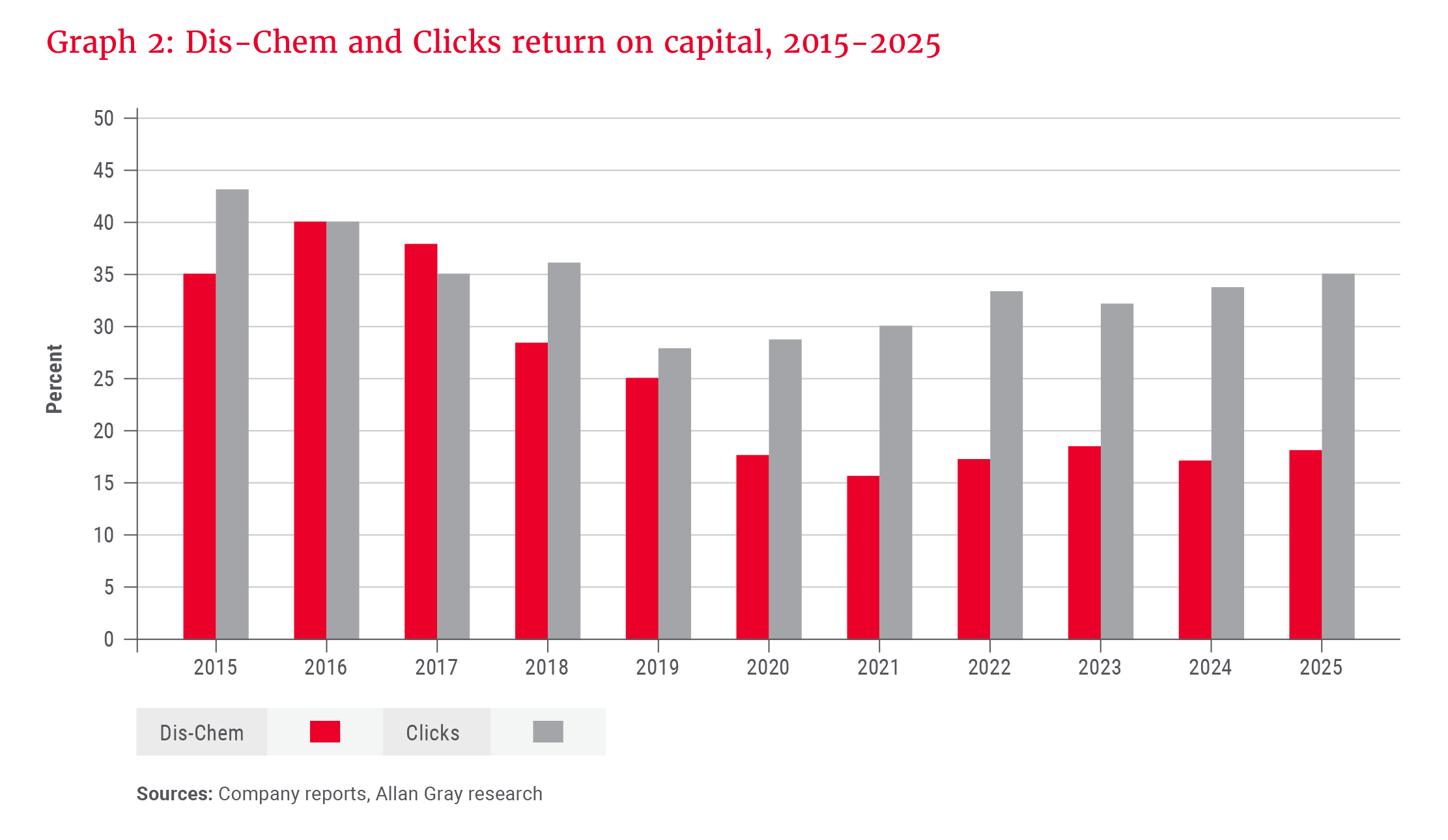

Dis-Chem’s return on capital has dropped over the last decade, as shown in Graph 2 below, which may concern some investors. However, we believe this decline is due to fixable issues, rather than a structural decline in the quality of the business.

Investing is inherently forward-looking. Markets often anchor to recent history, but value is created by anticipating what a business can earn in the future, not what it earned in the past. In our view, the current return profile does not fully reflect the earnings power of a more efficient, better optimised Dis-Chem and return on capital should return to levels well above the company’s cost of capital. Several factors support this view:

Cost-cutting measures and margin improvements: Dis-Chem’s operating costs have exceeded revenue growth. Management has initiated plans to reduce these costs, some of which are already bearing fruit. These include moving to a centralised store management system, which will improve efficiency and make it easier to manage headcount, shifting to more pharmacy assistants, who can be three times cheaper than pharmacists, and reducing the headcount of a costly management layer.

These initiatives, combined with a maturing store base and increasing scale (expanding total income margins), have given management confidence that it can achieve an 8% retail margin over the longer term, which is significantly higher than its current 4.7% margin (yet much lower than that of its competitor, Clicks, at just above 10%, which is structurally higher in part due to product mix). Even if it doesn’t get to the 8% margin, our calculations suggest there is room to increase that margin by close to 2% if things go to plan.

New store sizes have better economics: Part of the decline in return on capital has been due to opening stores too large for their catchment areas. Management has shifted its strategy to opening smaller stores. These stores have shorter payback periods and higher returns on capital.

Better data and analytics: Management has strengthened its use of data through specialised teams and platforms, including initiatives under its innovation arm, X, bigly labs. This is enabling them to better understand customer behaviour, refine promotional strategies and roll out their store network with greater precision. The recent launch of Better Rewards and its early traction further reinforce management’s improved use of data to strengthen the core business. This more disciplined, data-driven approach should improve new store economics and drive greater consistency across the existing store base.

Importantly, these improving returns are protected by a durable moat built on two pillars: ownership of the script and scale:

- Owning the script is strategically valuable for two key reasons. Firstly, pharmacies are highly regulated; not just anyone can sell scheduled medication. Licensing requirements, compliance standards and regulatory oversight create meaningful barriers to entry, limiting new competition.

Secondly, the script embeds customers into the ecosystem. Chronic patients return monthly to collect medication, creating predictable, recurring foot traffic. This steady demand anchors store traffic and drives high-frequency visits, which, in turn, support sales of higher-margin front-shop products. We all know what happens: You head into a Dis-Chem or Clicks wanting to buy one item and end up coming out with 10. Sometimes those deals are just too good.

- Scale is another serious advantage, creating a powerful virtuous cycle for Dis-Chem. As store numbers and sales volumes grow, procurement volumes rise, improving bargaining power with suppliers and lowering costs. These savings are reinvested into lower pricing and better promotions, strengthening the value proposition and attracting more customers. Higher traffic then drives further volume growth, reinforcing scale advantages. This self-reinforcing loop makes it increasingly difficult for smaller competitors to match pricing without materially eroding their own profitability.

4. & 5. Balance sheet strength and free cash flow

Dis-Chem maintains modest levels of debt, providing financial resilience and balance sheet flexibility. In addition, we expect a high proportion of earnings to convert into free cash flow over our forecast period. Ultimately, shareholders receive cash, not accounting earnings. A business that consistently turns profits into cash gives management flexibility, reduces risk, and creates real value for shareholders.

… given the improvements management is implementing, we think there is significant upside to margins.

Getting better than a fair price

At first glance, Dis-Chem does not appear cheap at 23 times trailing earnings; however, given the improvements management is implementing, we think there is significant upside to margins. Based on our estimates, Dis-Chem is trading on just 16 times our normal earnings. For a defensive business with a long growth runway, strengthening returns on capital, and a durable moat, this is an attractive entry point. This also screens as attractive relative to Clicks, trading on 22 times trailing earnings, which we view as having a more limited store roll-out pipeline and less scope for margin expansion.

No investment is without risk, and execution on margin recovery and store roll-out will be key. However, the risk-reward appears attractive. If management falls short of its margin targets, we believe investors still own a great business at a fair price. If management delivers, investors are likely to own a great business at a great price. We like those odds.

Allan Gray clients now own just over 10% of Dis-Chem.

Explore more insights from our Q1 2026 Quarterly Commentary

- 2026 Q1 Comments from the Chief Operating Officer by Mahesh Cooper

- Investing through disruption: Lessons from history for the age of AI by Nshalati Hlungwane

- Pan African Resources: The golden goose? by Andrew Boulton

- Higher discretionary allowance: The opportunity to invest more offshore by Daniel van Andel

- Orbis Global Equity: The art of adaptability in turbulent markets by Ben Preston

- Mind the gap by Horacia Naidoo-McCarthy

- Maximising new tax benefits to boost long-term investment outcomes by Shaun Duddy

To view our latest Quarterly Commentary or browse previous editions, click here.