Many investors are still reeling from the COVID-19 rollercoaster ride and are grappling with how to position their portfolios when they value both capital preservation and growth. Tamryn Lamb and Sean Munsie discuss how to balance risk and reward and explain why the Allan Gray Stable Fund could offer a potential solution.

In 2012 we published a piece discussing some of the ideas of author/financial adviser Carl Richards, who noted that most of us make the same mistake with our money over and over again: We buy high out of greed and sell low out of fear, despite knowing on an intellectual level that it is a very bad idea. This was nearly 10 years ago, and Carl’s piece was written in the wake of the global financial crisis. Fast forward a few years, and into another crisis, and it is interesting, albeit sobering, that we don’t seem to have learnt much from our mistakes: When it comes to our response to financial markets, we seem set on following the same patterns, taking comfort from the fact that others around us are doing the same.

The behaviour of investors on our local investment platform over the past 16 months illustrates this point. As Marise Bester noted in an article on risk perception in October last year, local high-equity funds experienced their highest net switch outflows in March 2020, when the FTSE/JSE All Share Index (ALSI) was at its lowest and fear was at its highest. This behaviour seemed to abate towards the end of 2020, and into the first four months of 2021, as the market staged a recovery and investors’ appetite for higher equity offerings, both locally and offshore, increased. While investors may have felt better exiting the market when they did, and re-entering when optimism returned, in the end they lost out on the recovery that ensued in their absence.

Looking specifically at investors in the Allan Gray Stable Fund: Those who invested in January 2020 and remained invested through the crash until the end of April 2021 would have earned an annualised return of 7.6% (after fees and with distributions reinvested). Meanwhile, those who invested in January 2020, switched into the Allan Gray Money Market Fund at the end of March 2020, and reinvested in Stable in January 2021, would have earned 0.36% as at end April 2021. Notwithstanding the pain, resisting the urge to act in the short term was the better course of action.

Of course, if one had had a crystal ball and could have predicted the market crash, one would have looked good being parked 100% in cash. However, this strategy would only have worked over a very short period as the market drawdown was sharp, but brief. Cash returns over the last 15 months have been lower than equities and bonds, reversing the trend we have seen over the past few years.

Is equity exposure essential?

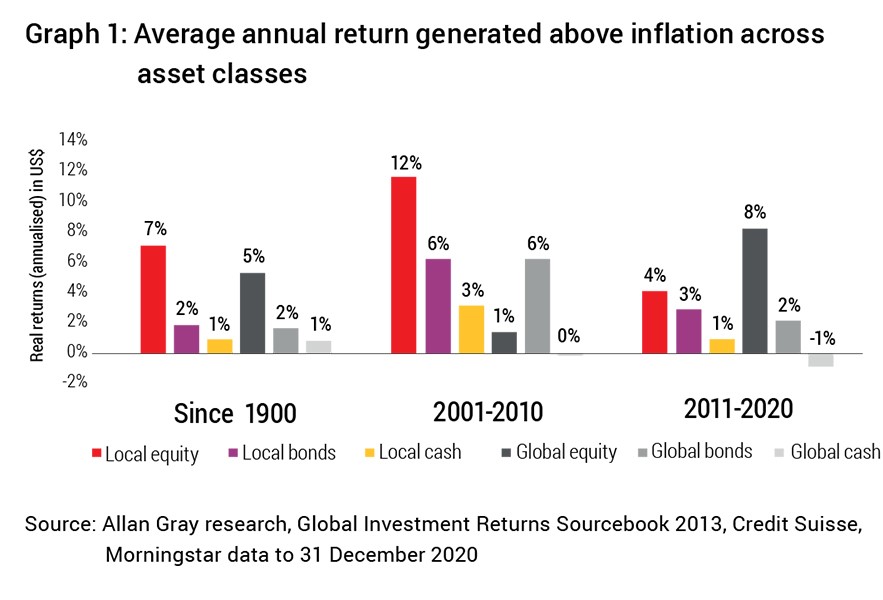

In the five years until end 2020, the annualised return of the ALSI was 6.0%, compared to the Allan Gray Money Market Fund’s 7.6%, understandably leaving investors somewhat disillusioned with the more volatile asset class. However, history reveals the only asset class that has consistently delivered returns in excess of inflation is equities – as shown in Graph 1. Over the last 100 years, on average, cash has given investors 1% real return and bonds 2%, while local equities have delivered 7% and global equities 5% after inflation is accounted for. The takeaway: Long-term investors need an allocation to carefully selected equities to protect and grow their wealth.

Of course, this presents somewhat of a conundrum. Investors need equities to deliver their required level of real growth, but many struggle to stomach the ups and downs to stay the course. If capital preservation and growth are equally important to you, or your client, one way of solving for this is to consider a low equity fund. Low equity funds have a maximum allocation of 40% to equities and can invest in other asset classes, including foreign assets, property, cash and bonds. The allocation across these classes is carefully managed by professional fund managers. This includes those decisions like trying to figure out the best time to enter and exit the markets, and weighing up the opportunities offered within and across the various asset classes. The Allan Gray Stable Fund is an example of such a fund.

Why the Stable Fund?

When we launched the Stable Fund back in 2000, we were looking to meet the needs of risk-averse investors who wished to preserve their capital, but also wanted to achieve real returns. The Fund is constructed based on our bottom-up assessment of the opportunities available across the asset classes, supported by a top-down view on macroeconomic and other risks. We don’t build portfolios betting on any single macroeconomic outcome; instead, we prefer to be positioned to do well in a range of potential outcomes, while aiming to protect clients against extreme events.

The equity component is key to our ability to deliver real returns, and while the Fund can invest up to 40% in equities (and at times has maximised this opportunity), our average exposure to equities has been approximately 25%. The lowest exposure to equities was 12.4% which occurred in January 2010 when we felt the market was very expensive. By having the bulk of the Fund’s assets in cash and bonds, the Fund is also able to generate an income, with the rolling 12-month average yield at 4.3%.

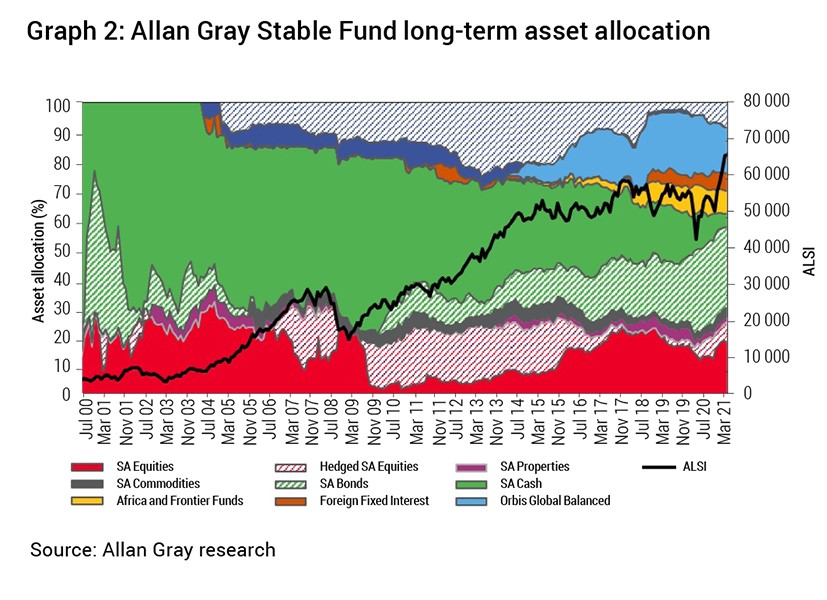

In our view, optionality is the Fund’s greatest asset: We believe having the flexibility to switch to where we see the best risk-adjusted opportunities is extremely valuable. See Graph 2 for an idea of how the Fund’s positioning has changed over time and read “Performance and positioning” for more information on our current asset allocation.

How financial advisers use the Stable Fund

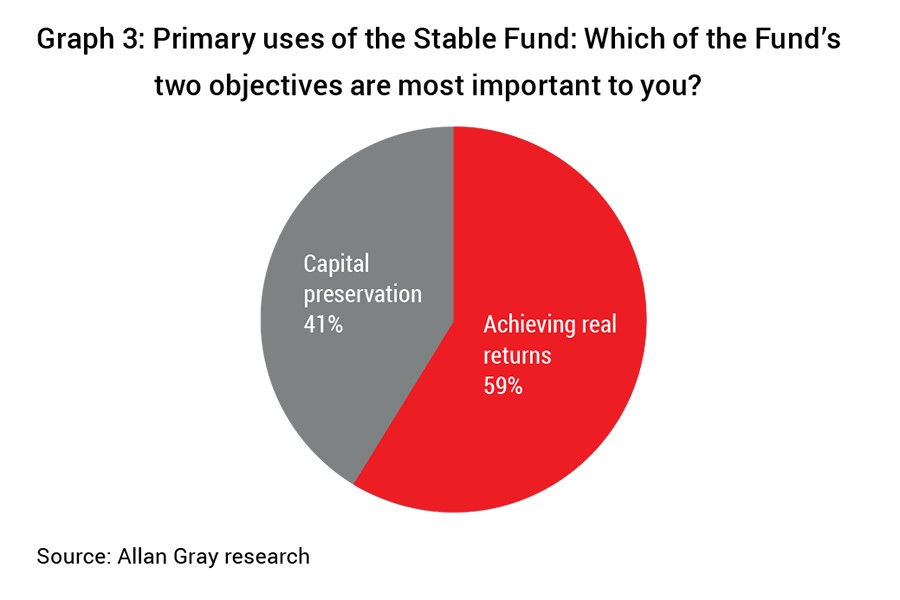

A survey of some of the financial advisers who invest in the Stable Fund on behalf of their clients showed that the primary uses of the Fund are in-line with its mandate: to preserve and grow clients’ wealth (see Graph 3). The Fund’s long-term track record has demonstrated that it fulfils this ambition, making it useful for both risk-averse clients and for those looking to draw an income in retirement – which is what advisers commonly use the Fund for. While investors have had to endure some volatility from time to time, many financial advisers say their clients are prepared to accept this in their bid to achieve real returns.

While many clients use the Stable Fund to draw an income, it is important to remember that drawing too high an income can deplete one’s capital. Most financial advisers surveyed believe that a reasonable drawdown percentage is 4-5%.

When asked what would be the most compelling alternative for a Stable Fund investment, almost 70% of advisers said they would pick another fund in the multi-asset low equity category, with about one-third of respondents saying they would pick an income fund.

Performance and positioning

Theory is all well and good but, at the end of the day, performance and capital preservation are what matters most to clients. So how has the Fund performed and how is it positioned for future performance?

Capital growth

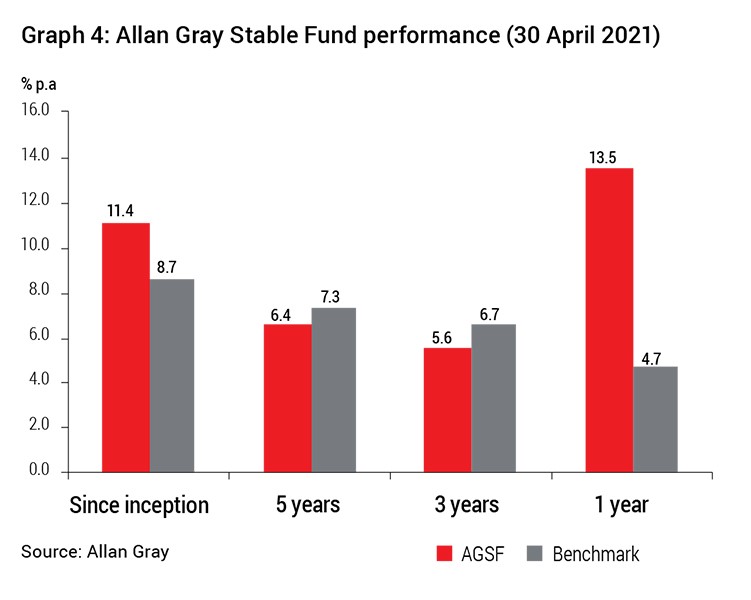

A look at the Stable Fund’s performance shows pleasing returns since inception and over the last year. Over a three- and five-year view, however, the Fund is behind its benchmark – as reflected in Graph 4. Over the last few years until the COVID-inspired crash, the local market generated lacklustre returns, with the exception of a narrow band of shares that did well. We were largely underweight the shares that outperformed and, as a result, our equity selection detracted from relative performance, while returns were boosted by fixed interest and cash. However, the same shares that underperformed over that period, such as Glencore, Sasol and Sappi, have boosted returns more recently, which we believe supports our view of their attractiveness.

Capital protection

The Fund has fulfilled its capital preservation objective over the last 20 years, except for a brief period during last year’s COVID-19 market sell-off. We carried a relatively high equity weighting into 2020 on account of attractive valuations, particularly among local shares. Many of these businesses saw sharp short-term declines in March and April, in line with the broader sell-off as investors assumed the worst-case outcome. Bonds, which traditionally provide downside protection, sold off in sympathy. We used the opportunity to buy distressed bonds and shares in March and April 2020. This opportunistic buying of undervalued assets has helped performance in the recovery.

Given the sharp rebound, it may be hard to believe that we continue to see value in a number of JSE-listed equities. However, some sectors remain depressed, and we believe that the current disparity in markets is creating an opportunity for bottom-up stockpickers like ourselves to generate meaningful returns. Yet we are not blind to the risks in SA and the high likelihood of an uncertain and drawn-out economic recovery. Much of the underlying exposure of the SA share component is in foreign businesses, including Naspers, Glencore and BAT.

When we look at yields in South Africa, the important question we need to ask is if investors are being sufficiently compensated for the risk they are taking on. One way to answer this is to look at real yields on SA long bonds, which are high compared to history, and versus those available in both emerging and developed markets. At 9.4%, the 10-year government bond yield looks optically high, but this is not an indiscriminate buying opportunity, and we are concerned about a deteriorating fiscal situation. To manage around this, we carefully construct the fixed interest component, balancing upside potential and duration risk. For example, we would rather sacrifice a bit of return and reduce risk by investing in inflation linkers and floating rate bonds, which can help protect investors from inflation or interest rate changes.

The Stable Fund is currently making use of its full 30% offshore allocation, offering diversity and building in protection for investors if the rand weakens. However, only 12% is placed in foreign shares as we are worried about valuations in certain markets – although we are seeing some pockets of value, such as in emerging markets. Many emerging market stocks are currently trading at low valuations relative to history and their developed market counterparts. We believe we are able to pay lower than-average prices and get a collective of well-above average businesses in return. Asian technology shares are one such example. The remainder of the offshore allocation is invested in a mix of hedged equities, commodities, bonds and cash.

Looking forward

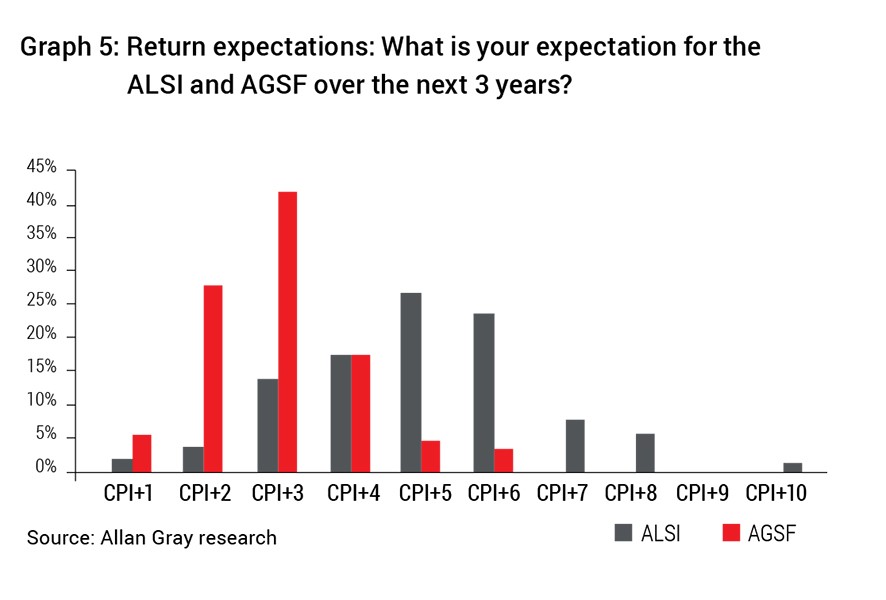

The majority of financial advisers surveyed expect the Stable Fund to deliver CPI + 3% over the next few years versus an expected ALSI return of CPI + 5% (see Graph 5). We are cautiously optimistic about the Fund’s ability to outperform CPI + 3% over the same period, supported by exposure to equities and active asset allocation decisions.

Is Stable the right solution for your clients?

The Allan Gray Stable Fund balances caution with opportunism. The Fund’s flexibility to invest where we see value is key. The liquidity from cash and bond investments allows us to take advantage of market extremes, and the conservative asset allocation minimises the risk of capital loss.

The Fund could be a good solution for those investors who want to balance the risk of losing money with the risk of losing out by not being in the market at all.