Shaun Duddy discusses how to meet and manage risks while drawing a stable income in retirement. He explains why investing at least 50% in growth assets is a necessity and why drawing more than 4% is not advisable.

Retirees drawing an income face three key risks: Longevity risk, i.e. the risk of living longer than expected; inflation risk, i.e. the risk that the rising cost of living eats away at their investment and investment risk, i.e. the risk of their investment return not being high enough to compensate for the other two risks.

With the first two risks being largely outside of your control, it’s crucial to focus on the third. To do this, you are advised to:

- Plan for a long lifespan

- Structure your retirement portfolios for growth

- Make sure you draw a sustainable level of income

These are explained in more detail below

1. Plan for a long lifespan

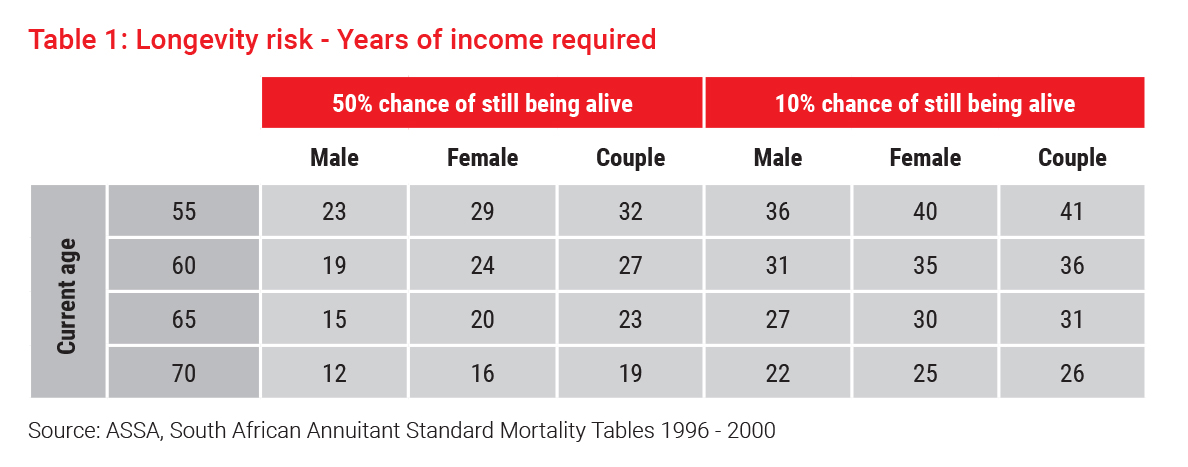

Improved medical technologies and lifestyle have seen life expectancies increase, and they are likely to increase further moving forward. Table 1 can be used to get a rough sense of how many years of income to plan for if you want to be either 50% or 90% sure that you will not outlive your planned income stream. A caveat is that these time horizons will continue to evolve as life expectancies improve.

As an example, consider a male aged 65. To be 50% sure that he won’t outlive his income, he should be planning for at least 16 years of income, at which point there is still a 50% chance that he will be alive and that he will need more than what has been accounted for. On the other hand, if he wants to be 90% sure, he needs to plan for at least 28 years of income. At that point there is about a 10% chance that he will still be alive and need more income than he planned for. Of course we are all different, but if you want a reasonable level of certainty, you need to plan for at least 30 years in retirement.

And that is only half of the story: in each of those years, you will need to increase your income with inflation to maintain your income in real terms. Inflation therefore determines the level of income required in each of the 30+ years and determines the nominal returns required for that income to be sustainable. While we have become quite accustomed to relatively low inflation levels and a reasonably stable inflationary environment, this has not always been the case and may not be the case in future. Portfolios need to be resilient in the face of inflation to generate the necessary real returns.

2. Structure your retirement portfolios for growth

Retirement is not a time to shy away from growth assets.

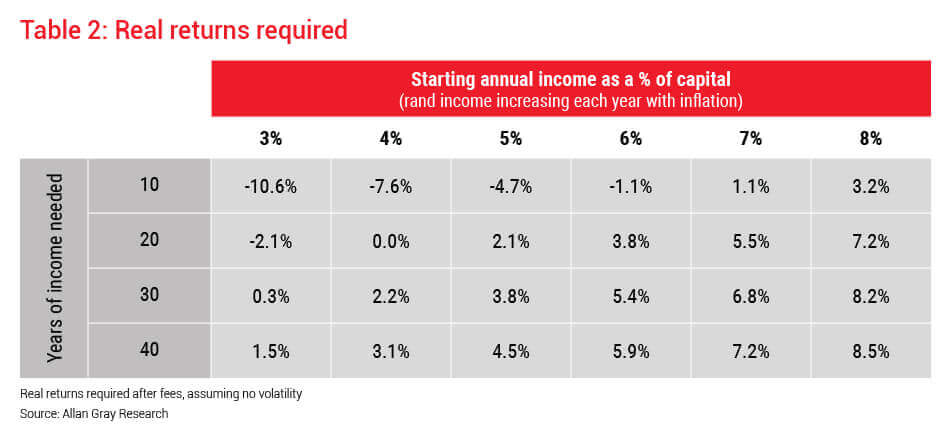

Table 2 shows the level of real returns required for different investment horizons and income requirements. If your starting income requirement is 4% of your current capital, increasing each year thereafter with inflation, and you need 30 years more income, you need to achieve at least 2.2% per annum in real returns. If your starting income requirement is 8% of capital, the required real return increases significantly to 8.2% per annum. At the higher levels of required real return, you would need to take on significant investment risk to stand any chance of achieving those targeted real returns.

3. Make sure you draw a sustainable level of income

Unfortunately investment risk means you are not always going to get the level of return you need. Portfolio returns may be lower than required over time and you may need to make income withdrawals during periods when the market is in a downturn, meaning that your personal return may be lower than the portfolio’s return and lower than required. While the average return that is likely to be generated by your portfolio over time is important, it is also very important to understand what your personal return experience in that portfolio is likely to be: the ordering of your returns, volatility and the timing of your drawdowns all influence your personal return outcome and therefore the sustainability of your income.

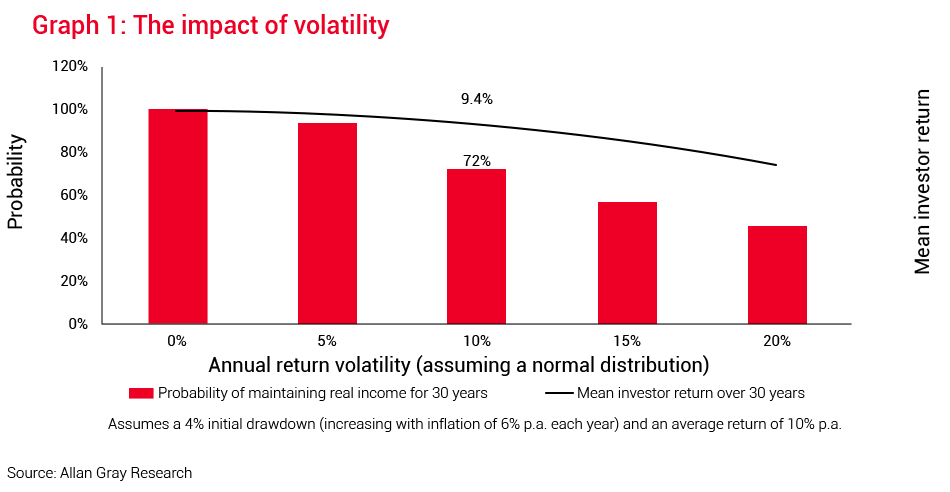

Graph 1 looks at the potential impact of different levels of return volatility on sustainability of income and personal returns over a 30-year period where the expected portfolio return is 10% per annum, inflation is assumed to be 6% per annum and you draw a starting income which is 4% of capital and increases each year with inflation.

With 0 volatility, there is 100% chance of sustainability and you would get the expected portfolio return of 10% per year. As the volatility increases, the chances of sustainability reduce, along with the personal return you could expect.

As an example, note that the Allan Gray Balanced Fund has sat near to 10% annual volatility since inception in 1999. At that level of volatility, the average client return would be approximately 9.4% per annum (i.e. 0.6% lower than the portfolio's expected return of 10% per annum), resulting in only a 72% probability of real income being maintained over 30 years.

This shows that even if a portfolio can achieve the required level of real returns over time, once volatility and drawdowns have been accounted for, you may not enjoy the required level of return. Accounting for these risks, it becomes clear that the achievable real returns and starting income levels are more limited than those shown in Table 2.

The reality is that for drawdowns of more than 4%, the odds are not in your favour.

Where income sustainability is achievable, how should you invest to manage these risks?

The key is to:

- Invest for real returns

- Actively manage downside risk

This requires an appropriate exposure to growth assets, a focus on total returns and trying not to react to short-term market movements.

Our research indicates that retirement portfolios should have at least 50% in growth assets such as equities to generate the necessary real returns.

Many believe that the best way to invest for an income drawdown is to focus on income returns over capital returns. The theory is that by having income returns cover the income drawdown, you don't have to worry about capital volatility. This argument assumes a portfolio's income returns can continue to increase consistently with inflation with no risk and that the portfolio can still generate the same total returns as other more risky assets. This is not generally the case. We therefore believe it is better to maximise total return, regardless of whether it is income or capital return, and actively manage downside risk to achieve a desirable risk-return trade off. To do this, you can either create a well-diversified portfolio using building blocks, with the help of your independent financial adviser, or you can pick an aligned multi-asset class fund like a balanced fund, where the investment manager manages the growth asset exposure and downside risk.