Tax-filing season tends to roll around faster than expected each year, often leaving taxpayers with additional admin and last-minute pressure. While the process may feel familiar, the tax landscape evolves each year. In light of this, it is worthwhile to pause and take stock before getting started. As the 2025/2026 tax-filing season approaches, tax specialist Lihle Khumalo answers some common tax-filing season questions to help investors prepare for a smooth submission process.

What are the tax-filing season dates to diarise?

Diarise the applicable dates to ensure you submit your 2025/2026 return (for the period 1 March 2025 to 28 February 2026) on time.

What do the tax changes announced in the Budget speech mean for your 2025/2026 tax return?

The Budget speech delivered in February 2026 introduced several tax changes, which may leave you wondering how these will affect the personal tax return you are about to file. The key point to keep in mind is that all of the changes affecting personal income tax will only take effect from the 2026/2027 tax year. This means they will only impact next year’s tax-filing season, not the return you are currently preparing, and you do not need to factor these announcements into your current submission.

Who needs to submit a tax return?

Not everyone is required to file a tax return, so it is important to understand whether you are obligated to file one. The South African Revenue Service (SARS) may levy administrative penalties against you if you fail to meet your filing obligations.

You are generally required to submit a return if you earned income above certain thresholds, carried on a trade or have more complex tax affairs beyond standard employment. For the 2025/2026 tax year, this includes situations where:

- Your gross income exceeded the applicable age-based threshold

- You earned additional income beyond your salary, such as rental income or other business income

- You realised capital gains above R40 000

- You held foreign assets or funds above the prescribed limits

- You are involved in more complex structures, such as a trust

You may also be required to submit a return if SARS specifically requests it, even if your income falls below the threshold.

While auto-assessments mean that some individuals are not required to actively file, it is still advisable to confirm whether you meet the criteria for submission, particularly if your tax affairs are not straightforward.

Who may not need to submit a tax return?

You may not be required to submit a tax return, particularly if your tax affairs are straightforward and your income tax has been paid over to SARS by your employer.

For the 2025/2026 tax year, you may not be required to file a return if your income for the year consisted solely of one of the following income streams:

- Salary from a single employer (not exceeding R500 000 for the year, where PAYE has been correctly deducted)

- Local interest income within the exemption thresholds (other than tax-free investment interest)

- Tax‑free investments

- Exempt dividends (for non‑residents)

- A single lump sum withdrawal or retirement benefit, where tax was correctly applied via a SARS directive

In addition, if you are selected for auto‑assessment, you may not be required to submit a return – but only if the information used by SARS is complete and accurate.

What if my tax affairs are more complex?

If you have multiple income streams or your tax affairs are more complex, you will likely need to submit a return. For example, you will still need to submit a return if you:

- Received allowances that require reconciliation (e.g. travel allowances)

- Earned foreign income or rendered services outside South Africa

- Received taxable fringe benefits

- Have multiple sources of income

SARS auto-assessments – what you need to know

SARS continues to expand its use of auto‑assessments, using third‑party data from employers, financial institutions, retirement fund administrators and medical schemes to pre‑populate your tax return. If you are selected, you will receive an assessment directly from SARS without needing to submit a return upfront.

Between 1 July and 12 July 2026, SARS will notify taxpayers via SMS or email if they have been auto-assessed. The notification will also tell you whether you are due a refund or need to make a payment.

Next steps:

- If you agree with your auto-assessment

If you receive a notification, have reviewed your assessment in detail and are satisfied that the information is accurate, no return is required as the assessment is issued automatically. However, if the assessment reflects an amount payable, you must ensure that the tax liability is settled by the due date indicated on the assessment.

- If you disagree with your auto-assessment

If your auto-assessment contains incorrect or incomplete information, you should update and submit your tax return via eFiling or the SARS MobiApp.

Can pre-populated information be corrected on your return?

SARS relies on third-party data to pre-populate your return. In the 2025/2026 filing season, taxpayers are unable to remove or overwrite this information where it is incorrect, specifically in relation to IRP5 certificates. If you identify errors in pre‑populated data, you may need to engage with the relevant third‑party provider (such as your employer or fund administrator) to have the information corrected at source. This may delay the finalisation of your return, so it is advisable to review your pre-populated information as early as possible.

Auto‑assessments are designed to simplify the process, but they don’t absolve you of your responsibility to ensure your return is complete and accurate. A quick review can make the difference between a smooth filing experience and a costly correction later.

Convenience doesn’t always mean accuracy: It remains your responsibility to review your assessment in detail before accepting.

Make sure you have the right documents on hand

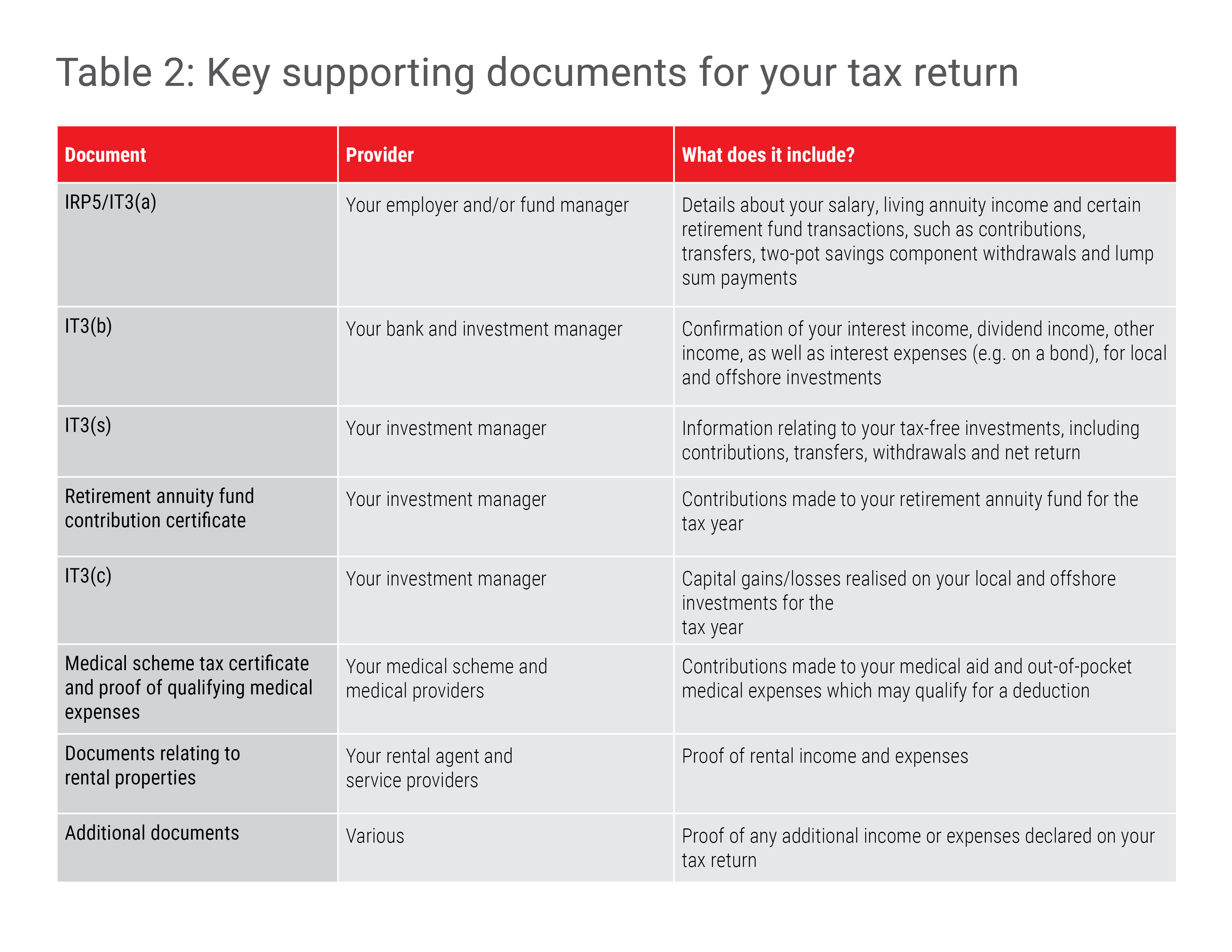

Before you submit your return or review your auto‑assessment, make sure you have all applicable supporting documents on hand from all your relevant service providers, not just Allan Gray. This information forms the basis of what is reflected on your return, whether pre‑populated by SARS or captured by you.

While some information may already be included, you should still verify it against your source documents and ensure that nothing has been omitted. Examples of key documents to consider are outlined in Table 2.

Remember, you are required to retain supporting documentation for five years from the date of submission, as SARS may request these to verify the accuracy of your return.

Understanding the impact of two‑pot withdrawals

If you made a withdrawal from the savings component of your retirement fund over the past tax year, it is important to understand how these withdrawals affect your tax position.

Withdrawals from the savings component are taxed at your marginal income tax rate.

How does this reflect on your tax return?

Your retirement fund administrator should have issued you with an IRP5 or IT3(a) tax certificate reflecting the withdrawal amount, together with the tax withheld and paid over to SARS. The withdrawal is treated as income, and the gross amount must be included in your gross income. The relevant source codes required for your return will be included on the IRP5/IT3(a) tax certificate provided.

Don’t be caught off guard

It’s easy to assume that the tax on your two-pot withdrawal has already been taken care of by the fund administrator through PAYE, but that is not always the case. If you had other income during the year, like a bonus, rental income or investment returns, your total taxable income may be higher than expected. This can push you into a higher tax bracket and leave you with additional tax to pay when you submit your return.

Are you missing out on a deduction for excess contributions?

Contributions to your retirement funds that do not qualify for a tax deduction in a particular year are carried forward to future tax years. These are referred to as excess contributions.

All current-year retirement fund contributions are reflected on your tax return. While the full amount you contributed is shown there, the deduction may be limited in terms of section 11F of the Income Tax Act. The balance (i.e. your excess contribution) is then carried forward to future years and appears on your notice of assessment (ITA34) as a “brought forward” or “carried forward” amount.

Review your ITA34 carefully to ensure that excess contributions are correctly recorded and applied to avoid missing out on a legitimate tax deduction. If you find yourself in this situation, it may be worthwhile to file a dispute with SARS or contact your nearest SARS branch for assistance.

Living annuities and SARS third-party appointments

SARS has the legal authority to instruct a third party, such as your bank, employer or investment provider (such as Allan Gray), to settle your outstanding tax debt, including associated interest or penalties, using funds held on your behalf. This includes income streams such as living annuities. This process is referred to as a third-party appointment.

Once such an appointment is issued, the third party is legally obliged to comply and must pay the specified amount to SARS. This can have serious consequences, particularly where income streams such as living annuities are affected. Keeping your tax affairs up to date helps avoid scenarios where SARS recovers debt directly from your income sources.

Proactively monitor and settle any outstanding tax liabilities or make appropriate payment arrangements with SARS to avoid enforcement action.

Your simple tax-filing checklist

As you prepare to submit your return, the following checklist can help ensure that you have covered the key steps:

- Confirm your income sources

- Collect all your supporting documents

- Review your auto-assessment (if applicable)

- Review your deductions (if applicable)

- Submit your return before the deadline

As the tax-filing season approaches, a little preparation can go a long way. Even with more information being pre‑populated by SARS, it is critical to review your return carefully and ensure everything is complete and accurate. Taking the time to get this right upfront can help you avoid delays, unexpected tax outcomes or unnecessary follow‑ups from SARS.