The first step is often the most difficult to make, but it does not have to be so with investing. Follow these tips to start off on the right foot.

Our research shows that most people take over a year to go from making a commitment to invest, to actually starting their investment. Some people forget their best intentions or are so intimidated by the options out there that they never start. While investing is not something to rush into, procrastination can cause you to miss out. Follow these steps to get started.

Start with yourself

The way you choose to grow your money must fit you and match your goals, not the other way around. In Part 1 of this series we discussed thinking about the things that you truly value. Hopefully from that you came up with a few goals to target and some idea of when you want to reach them. That thinking should form the basis of your plan, which you can build on by answering the questions below:

Understand the difference between saving, investing and trading

There are a number of ways of growing your money, not all of which will suit your purposes. Three options to consider are saving in a bank account, investing in a unit trust product, and investing or trading in individual shares.

Saving with a bank is perhaps the most simple: you deposit money, and the bank promises you a certain level of return after a specified time. Fixed deposits are safer than most other options. The downsides to watch out for are that your money may be locked in for a time and you may not be able to get returns that are ahead of inflation. This means that your money isn’t worth much more than you put in when the fixed deposit matures.

On the other the end of the spectrum you may also consider investing or trading directly in the shares of companies on the stock market. It is possible to get fantastic returns on the stock market, but it is also possible to lose all of your money. Direct share investors need the time to research and analyse stocks, and they compete with professional managers in an unforgiving environment. Even an enthusiastic and experienced amateur with lots of time will struggle to match the efforts of the best investment professionals. On the other hand, DIY share investors can save on management fees.

In between these two are investment products like unit trusts. Unit trusts pool together money from many investors, allowing them to administer and diversify their investment cheaply. A ‘passive’ unit trust simply invests in a basket of shares or bonds on an index like the FTSE/JSE Top 40. An ‘actively managed’ unit trust has a professional investment manager making decisions about which specific shares or other investments to include. There are many flavours of unit trusts: from more conservative money market unit trusts to equity-only unit trusts that offer a higher return ceiling - but also a bumpier ride.

Think about how much up and down you can handle

Another way to frame this is: can I handle losing some of this money over the time that I am invested? Investment returns never come in a straight line. The squiggly rollercoaster of returns will test your constitution and you should be prepared to have some down months and years. As long as you remain invested these losses are theoretical. It is only when you withdraw that you make real losses.

If you feel you can’t handle this, you may consider picking from more conservative options – but remember that they offer lower returns. Like jumping out the rollercoaster as its plummeting down, withdrawing from an investment at the wrong time will leave you in a worse off place even if it was headed in the right direction.

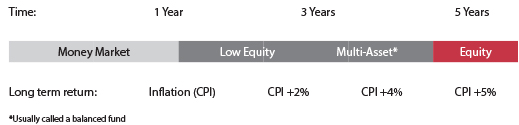

Consider your timeframes

How long you need to invest will be dictated by the goals you set yourself in Part 1, but it is equally important to be reasonable about the amount of time it will take to get returns. Generally, the higher the returns you need the longer you need to stay invested.

An example of how this plays out may go something like this

GOAL: I want to put down a deposit on a house in three years’ time.

Q1: Fixed deposits don’t offer enough returns and I do not have the time to dedicate to investing directly in shares, so I choose to use unit trusts.

Q2: I am comfortable with some volatility, but I can’t bear being in an investment that will go up and down regularly.

Q3: I was hoping to only be invested for three years, but I can see that I should probably extend that to five years or increase the amount of money I am investing to make up for the shortfall. Something with some equity - like a balanced fund – will help me get the returns I need.

Now that you have a clear list of requirements, you can start researching products – discussed in next week’s instalment – and looking for an investment management company to partner with, which we will cover in part 6.

This article forms part of a series that you can access here.

Find this article useful? Please let us know.