Parents can expect little relief in 2024, with reports suggesting that fee hikes for South African schools will yet again come in above general inflation, which is currently sitting at 5.5% (based on the November 2023 print). Parents with kids at government and private schools alike should brace themselves for fee increases of between 6% and 10%, according to various reports. This is not unusual, with an economic bulletin published by the South African Reserve Bank (SARB) noting that school fee increases in South Africa have, on average, been roughly 2.6% above inflation every year since 2012, aside from 2021. In an environment of already high consumer inflation, this packs an extra punch.

Many of us rely purely on our salaries to pay for our children’s education. We absorb the cost from month to month, tweaking our budgets to accommodate the ever-increasing expense. But the problem with this is that the cost of education typically grows at a higher rate than the average salary and inflation in general. Over time, this difference effectively means that a greater portion of your salary will have to be set aside for your children’s education.

For families who are concerned about the quality of education in the country, many are actively investing offshore to eventually access premium international education opportunities, according to news reports quoting stats from various local investment managers who offer offshore portfolios.

If sending your children overseas is a consideration, it is a good idea to invest a portion of your portfolio offshore. Costs are likely to be more palatable if you are saving and spending in the same currency.

According to cross-border specialist, Sable International, an average of 11 000 South Africans study overseas each year, with reports indicating that college tuition fees in the US are between US$32 000 and US$60 000 (approx. R587 800 to R1.1m) a year. The UK could cost anything between US$14 100 to US$38 000 (approx. R259 000 and R698 000) a year. And this is before including the average cost of living.

The above points emphasise the importance of prioritising investing for your child’s education.

Five factors to consider when investing for your child’s education

- Start saving at the birth of your children: a little goes a long way if you start early enough

Even though you may be able to afford your child’s primary school fees today, this doesn’t mean you’ll be in the same position when they reach high school or university. The good news is that if you invest to fund your child’s education – even at a nominal amount per month – the growth on an investment can lower the future impact of education costs.

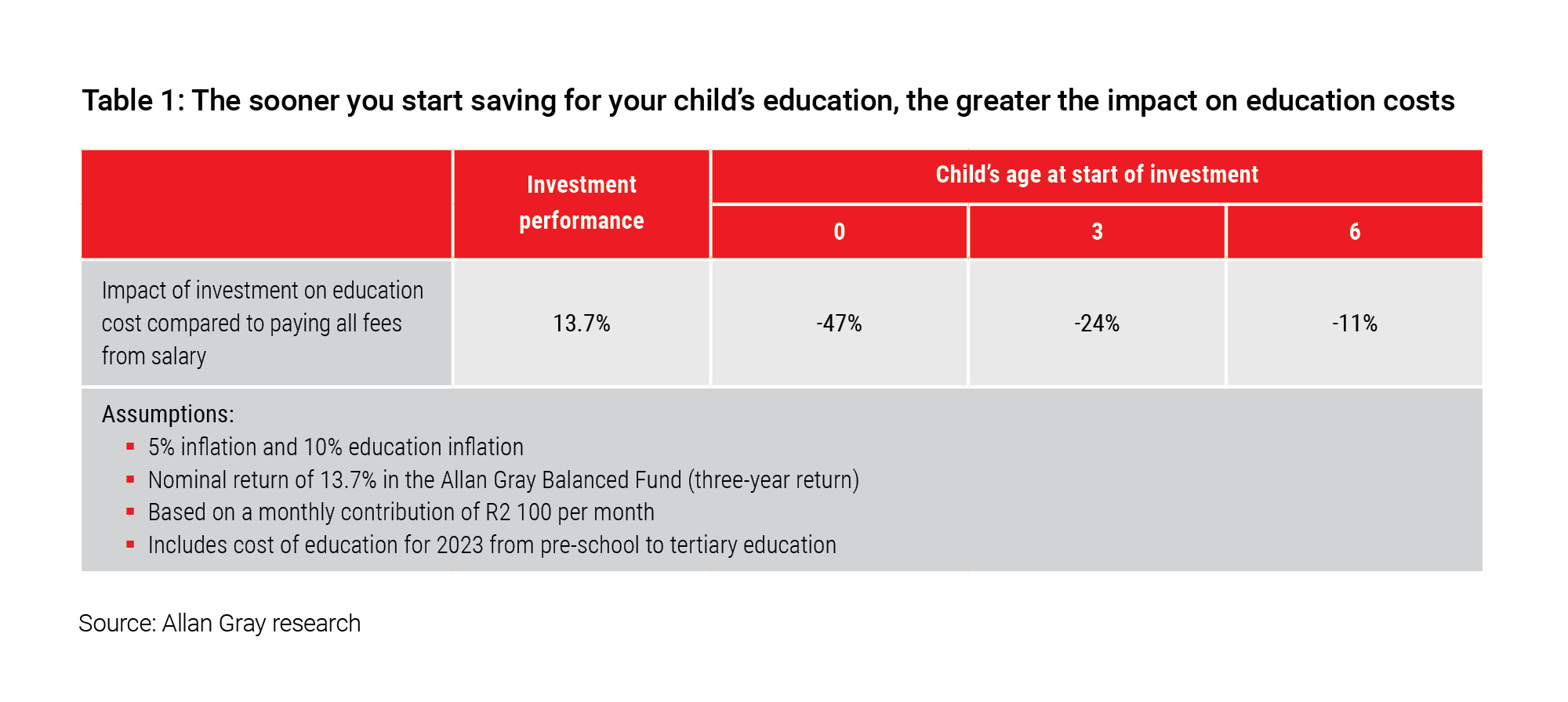

Allan Gray research suggests that you could reduce the impact of high school and university education costs by more than 45% if you invest when your child is born, and only withdraw when they start high school, as per Table 1.

The research finds that delaying investing for your child’s education to when your child is six years old, for example, reduces the cost of education by just 11%. This shows that the earlier you start investing, the greater the impact on the education costs.

- Take advantage of time – investing is a long-term journey

As demonstrated in point 1, time is an essential ingredient to successful investing. The sooner you start, the more time you have to make contributions and to benefit from the magic of compounding: earning returns today on the returns you earned yesterday.

There are many investment accounts and policies available to save for your child’s education, including education policies, unit trusts, tax-free investment accounts and endowments. The challenge for many parents is taking the first step. Starting to put some money aside as soon as you can will extend the level of financial flexibility you will enjoy in the future. - Aim for real returns to beat inflation

Education inflation typically exceeds headline inflation. This means that your education investments need to deliver a real (above-inflation) return. To achieve this, you will need some exposure to higher-risk assets like equities, which have historically delivered stronger returns than other asset classes. How much risk you can take on will depend on your time frame and risk appetite. - Avoid credit if you can

The negative implication of “pay-as-you-go” education is that you will have no capital saved up for your child’s future studies. This means you may be forced to apply for credit, which can be prohibitively expensive if you make use of an unsecured personal loan. The effects of compounding, which work for you when investing, work against you when you have accumulated debt. - Investing offshore to finance international education? Consider the impact of currency

If you are going to be spending on tuition and living expenses in foreign currency, it is useful to understand the profound effect exchange rates have on the returns of international investments – and your overall budget. If you are paying fees in dollars and the rand drops 10% against the dollar overnight, your fee bill will be 10% heftier in rands. A well-diversified offshore investment portfolio can help protect you against these fluctuations.