In the past 12 months, global inflation has surged. Sandy McGregor discusses the increasingly turbulent response of the financial markets below, and in our latest podcast.

In Sir Arthur Conan Doyle’s short story Silver Blaze there is the following conversation between Sherlock Holmes and Mr Gregory, a Scotland Yard detective:

Gregory: “Is there any other point to which you would wish to draw my attention?”

Holmes: “To the curious incident of the dog in the night-time.”

Gregory: “The dog did nothing in the night-time.”

Holmes: “That was the curious incident.”

The dog that did not bark

When one contemplates the response of interest rates to the biggest surge in inflation in more than 40 years, the dog that did not bark in the night comes to mind. In the 12 months to February 2021, US consumer prices increased 1.7%, equal to the average inflation rate of the previous decade. By June 2022, US inflation had reached 9.1%. The yield on 10-year US government bonds, which was at a low of 0.55% in August 2020, responded by moving inexorably upwards, and surged to 3.5% in the week after the May inflation print was announced on 10 June, before retreating to about 3.0%.

Europe faces similar inflationary pressures, with eurozone inflation reaching 8.6% in June. Its bond yields have reacted similarly. However, after adjusting for current inflation, real bond yields are at historical lows only equalled immediately after the end of the Second World War. Given the magnitude and widespread nature of this inflation, the response of the bond markets must be regarded as muted. The bond market dog has started to bark, but not very loudly. This raises the question: Are developed economy bond investors presciently anticipating a return to price stability or are they delusional?

Central banks abandon the transitory narrative

During 2021, as month after month the prices of goods and services rapidly increased, there was a growing debate among market participants as to whether this inflation was going to be transitory or prove persistent. Initially, developed economy central banks were firmly in the transitory camp and downplayed inflationary risks. Probably a significant reason for their complacency was that they were inappropriately positioned for an inflation shock, with short-term policy rates at zero or even negative.

Investors often persist with an investment strategy in which they strongly believe long after it has proved to be wrong. Central banks are very conventional organisations and are equally prone to such mistakes. Most developed market central banks have been operating on models that have been totally discredited by events. By the middle of 2021, as inflation continued to surprise on the upside, doubts started to emerge and in October, the Federal Reserve Board (the Fed) announced that by March 2022 it would end its US$120bn per month asset purchase programme and then embark on a cycle of rate hikes. This it has done. The pace at which rates are being increased has been accelerated from the originally envisaged 0.25% at each of the Federal Open Market Committee (FOMC) meetings. An increase on 4 May of 0.5% was followed on 15 June by a 0.75% hike, which together brought its policy rate up to 1.5%.

The language emanating from the Fed is becoming increasingly hawkish. At the 15 June meeting, members of the FOMC were forecasting that their policy rate at the end of 2022 would be 3.4%. In testimony to Congress on 22 June, Fed Chairman Jerome Powell said rate increases would continue until there was compelling evidence that inflation was returning to the Fed’s 2% target.

The Bank of England (BoE) has also initiated a series of rate hikes and the European Central Bank (ECB) has done the same, bringing its policy rate back to zero, ending eight years of negative rates. Among major central banks, only those in Japan and China persist with an easy money policy. The Bank of Japan (BoJ) has continued its asset purchase programme to keep the long-term Japanese government bond yield at 0.25%. However, as this has caused serious depreciation of the yen versus other currencies, increasingly the policy stance of the BoJ is being questioned.

Neutral rates

With most central banks abandoning a flawed zero interest rate policy, the debate is now about what is an appropriate short-term rate in current circumstances. Interest rates at or below zero no longer have many proponents outside Japan and China but there is no agreement as to what rates should be.

Economists postulate that there is a neutral rate, at which monetary policy is neither expansionary nor contractionary. Currently the Fed thinks that in the United States, if output is close to potential and inflation is 2%, an appropriate neutral rate will be somewhere between 2% and 3%. The BoE and the ECB also target inflation at about 2%. The BoE assumes the neutral nominal rate required to achieve this target lies between 1.25% and 2.5%. The ECB believes that in the eurozone the real neutral rate is negative and that its nominal neutral rate is somewhere between 1% and 2%.

Prior to the 10 June announcement of US inflation, in May 10-year government bond yields were roughly equal to these neutral rate assumptions, which suggests large numbers of investors believed these rates to be the ultimate endgame and that current inflation will indeed prove transitory. The turbulent market response to unexpectedly high inflation in May suggests doubts regarding this optimistic prognostication are increasing.

When money lacks value, it is used imprudently, promoting an inefficient allocation of resources, which further contributes to inflation.

A problem is that a neutral rate is a theoretical construct, the value of which is impossible to determine with any accuracy. No one knows what the neutral rate is. The economy is a complex feedback loop, which makes such certainty impossible. Neutrality is a moving target. Between 1980 and 2020 there was a secular decline in inflation, which implied neutral rates also declined. This virtuous trend has come to an end and neutral rates are on the rise. Furthermore, merely increasing policy rates to the prevailing estimate of neutrality is unlikely of itself to bring the current surge in prices under control; much higher rates probably will be required. This was the experience in the 1970s, when inflation was elevated for a decade, and aggressive action by Fed Chairman Paul Volcker was needed to restore price stability.

Inflation in the United States in the 1970s

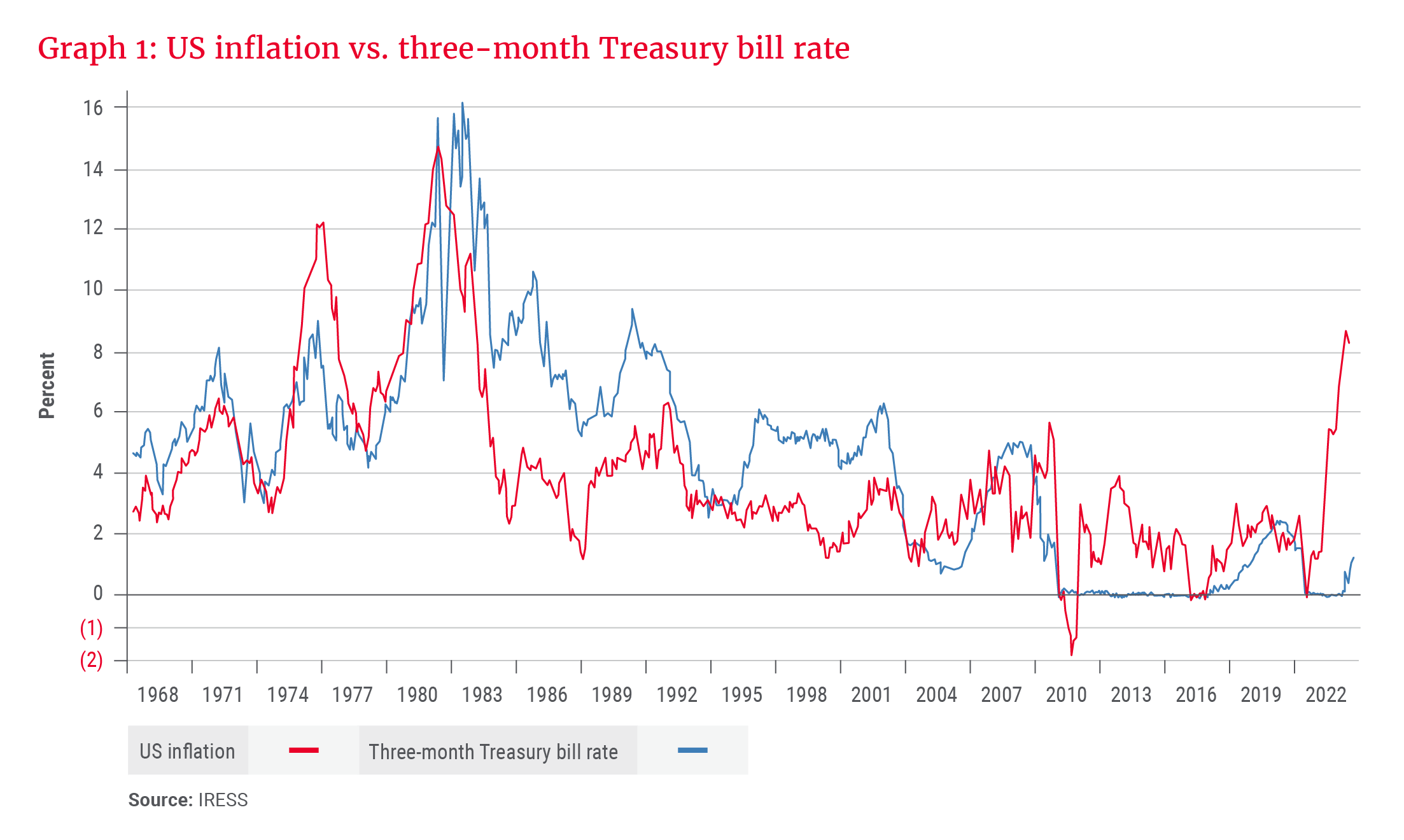

As can be seen in Graph 1, inflation in the United States in the 1970s came in three waves. The first wave commenced in 1968 and peaked at 6.4% in 1970, the second peaked at 11.7% early in 1975 and the third peaked at 14.3% in 1980. While oil price shocks were important causes of the second and third waves, spiralling wages in response to an increased cost of living were also to blame. It was normal practice to index wage agreements between employers and employees to inflation, which automatically created an inflationary spiral. Business responded to higher operating costs with increased prices. Inflation generated more inflation.

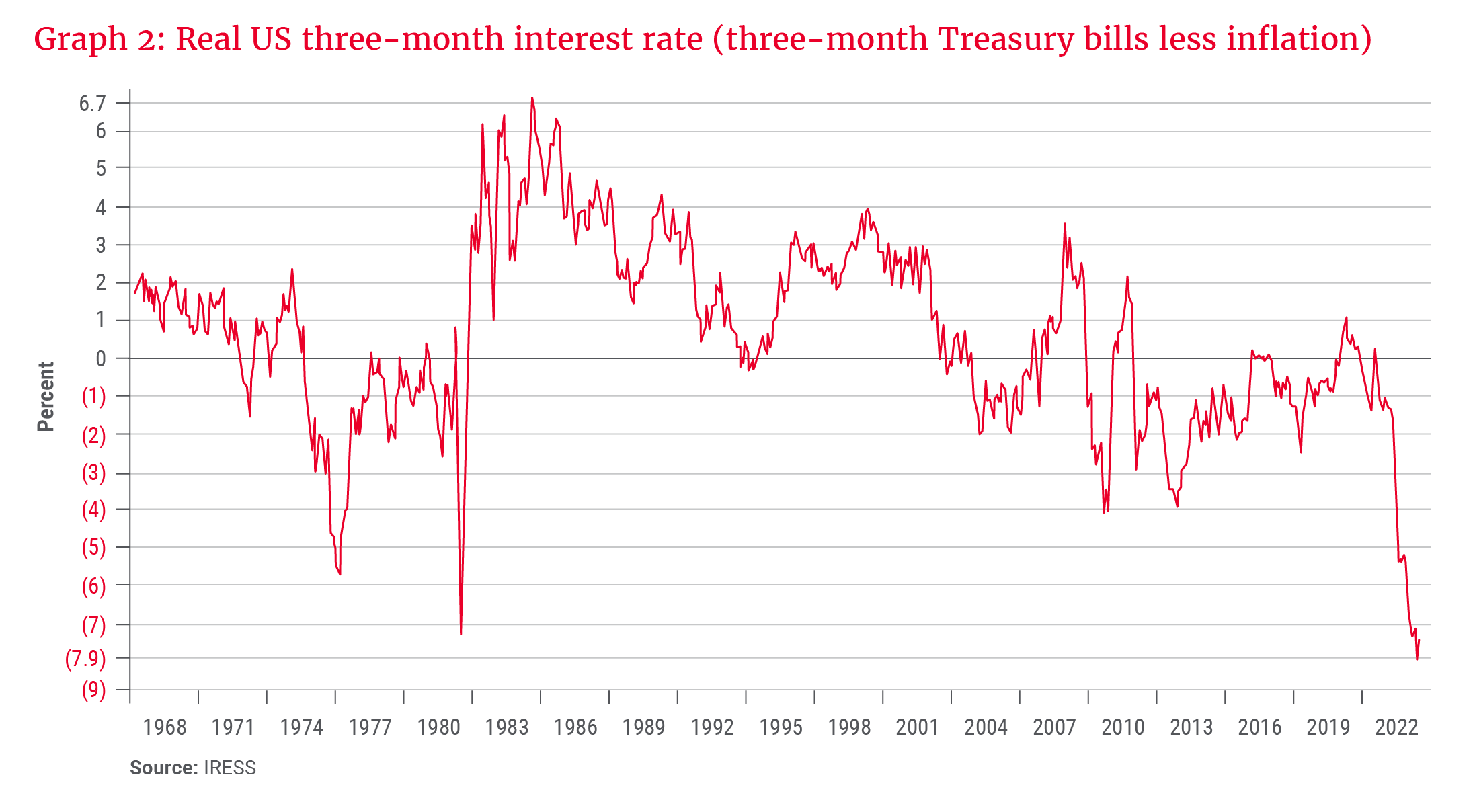

While at any one time a particular cost increase may have predominated, the upward pressure on prices became widespread. Between 1973 and 1979 this was aggravated by the Fed keeping its policy rate substantially lower than inflation (see Graph 2). When money lacks value, it is used imprudently, promoting an inefficient allocation of resources, which further contributes to inflation. An inflationary mindset had become totally entrenched and economic decisions were being made assuming that inflation was a permanent reality.

Something had to be done. On 6 August 1979, President Jimmy Carter appointed Paul Volcker to be chairman of the Fed, replacing William Miller, who had totally lost the confidence of the financial markets. Volcker acted rapidly to increase the Fed’s policy rate. In June 1981, the federal funds rate reached 20% and the prime lending rate of banks 21.5%. The US economy entered a severe recession. Unemployment soared, reaching 10.8% at the end of 1982. But the inflationary spiral was broken. In August 1983, US inflation was 2.4% and it remained subdued for 37 years until our present troubles started in 2021.

An important lesson relevant to our present crisis is that in 1982 inflation was brought under control not by higher interest rates themselves, but by a recession triggered by higher rates.

Volcker realised that inflation was caused by demand for goods and services exceeding the economy’s ability to supply them. He used high interest rates to force a recession, which reduced demand, thereby eliminating the imbalances causing inflation. He subsequently kept the federal funds rate substantially higher than inflation, so ensuring that monetary policy continued to promote price stability. An important lesson relevant to our present crisis is that in 1982 inflation was brought under control not by higher interest rates themselves, but by a recession triggered by higher rates.

The current outlook for inflation

Currently inflationary pressures are extremely widespread and diverse. They include the war in Ukraine, elevated energy prices, a global food shortage, supply chain disruptions, notably a shortage of computer chips and fertilisers, transport congestion, and labour shortages. Among the larger economies, inflation is highest in the United States, whose fiscal response to the pandemic exceeded that of any other country. This created a pool of excess savings waiting to be spent. US banks have over US$1.3tn excess reserves deposited with the Fed, which they can use to boost lending. However, this is not only an American phenomenon. Globally there is still a lot of money on the sidelines, which can sustain spending. The combination of robust consumer demand and supply disruptions has had a dramatic impact on prices. Eliminating inflation requires the cooling of an overheated economy, possibly a recession.

There are signs that a global slowdown has commenced. Elevated energy prices are crowding out other expenditures and promoting stagflation (a toxic combination of rising prices and slowing growth). Expenditures by governments to compensate for the adverse consequences of the pandemic have largely ended and fiscal deficits, while still large, are contracting. The consumption of certain goods which boomed during lockdowns, for example electronics, is slowing because the consumer is satiated. Global trade is slowing. Higher interest rates are having an adverse effect on property markets. China, which has been the largest contributor to global growth over the past 20 years, is now struggling to meet its 5.5% growth target. While recent draconian Chinese lockdowns to contain the spread of corona infections are now being eased, two sectors which have been key drivers of its growth, exports and housing, have been negatively impacted by weaker demand. In contrast to the rest of the world, China will probably try to reverse these adverse trends with greater government spending, but it will be unable to revert to its former higher rates of growth.

A decade of inappropriate monetary policy is taking its toll. The inflation genie is out the bottle.

The important question is, will this slowdown be sufficient to tame inflation? I believe the answer is no and that there is a significant possibility that stagflation will become prevalent. A decade of inappropriate monetary policy is taking its toll. The inflation genie is out the bottle. As was the case in the 1970s, inflation has developed a life of its own, where it pushes up business costs and business responds by increasing prices. In many countries a long period of wage stability has ended. Past experience is that spiralling wages are difficult to control and as wages tend to be set annually, it takes a number of years to do so.

All this is happening in a world where a previous declining secular trend in inflation has reversed. For 40 years globalisation promoted price stability. Efficient supply chains spanned the world and provided an abundant supply of cheap goods, which reduced the cost of living everywhere. In 2020, globalisation was already in retreat due to the erratic policies of Donald Trump, but the pandemic and the war in Ukraine have now focused the attention of business and governments on its risks.

Security of supply is the new mantra and achieving this will come with higher costs. Critically, there will be an increased demand for local skills, which will inflate labour costs. Demographic trends and rising popular hostility to migration will aggravate labour shortages. In addition to the cost of deglobalisation is the cost of decarbonising the global economy. Recent events have forced governments to postpone their aggressive climate change agendas, but these will not go away. Their cost is widely underestimated and will be paid for by the consumer through higher prices. If this is not enough, there is also the rising cost of underfunded retirement and health obligations.

There is a prevalent complacency about future inflation, but these secular trends suggest that, in coming years, it will be more persistent than is currently expected. Restoring the price stability we enjoyed prior to 2020 will require a far deeper recession and greater economic adjustments than will be politically acceptable.

Whither interest rates?

With the notable exception of Japan, developed economy central banks now recognise they have been way behind the curve and are rapidly increasing their policy rates to what they presently consider to be neutral. By the first quarter of 2023, most will reach their neutral targets. However, these rates will still be substantially lower than prevailing inflation. Some central banks may then use a slowing economy as justification to pause, but others will continue to push upwards towards what they anticipate inflation will be in 2023. Based on their present rhetoric, the ECB will be among the former and the Fed among the latter. If inflation persists at more than 4%, which is a distinct probability, they will still be behind the curve.

If monetary policy is to play an effective role in stabilising prices, interest rates must exceed the inflation rate.

Extremely low rates, such as have been commonplace for the last two decades, have proven ineffective, either to promote economic growth or to generate the inflation central banks wanted. Mispriced low rates merely create economic distortions such as asset bubbles. There is no place for them in an inflationary world. Any central bank which persists with substantially negative real rates will simply stoke the inflationary fires, as did the Fed between 1973 and 1979. If monetary policy is to play an effective role in stabilising prices, interest rates must exceed the inflation rate. This is especially true after a surge in prices such as we are currently experiencing.

Graph 2 shows the real return on three-month US Treasury bills since 1966. In the 18 years after the Volcker recession of 1982 they were initially 5% and then about 3%. If the inflation pessimists prove correct, interest rates will have to be substantially higher than they are at present. Inflation of say 4% demands an interest rate of 6%.

Will the central banks resist demands for lower rates?

Higher interest rates inflict collateral damage elsewhere in an economy. Rising mortgage costs threaten an edifice of inflated property prices. Higher borrowing costs threaten fiscal stability. Overleveraged businesses get into difficulties. The cost of holding inventories rises. It is commonplace for borrowers to hedge themselves against higher interest rates but when rates rise, this simply passes the loss to someone else. Rising interest rates put downward pressure on bond and equity prices.

As economic pain rises, central banks will come under increasing pressure to suspend rate hikes and make debt more affordable. A good example of this was seen at the end of 2018 when an equity market decline put the Fed under pressure from Wall Street to abandon its intention to further increase its policy rate. The Fed did what the market wanted. Famously, Volcker resisted all such pressures and crushed inflation in 1982. But will the present generation of central bankers show such fortitude?

After more than a decade of zero rates, low borrowing costs have become an addiction. The pressures to keep rates low will be massive. As the monetary policy bureaucracy has been so committed for so long to low rates, it is likely to support demands to moderate hikes. Some talk about Fed Chairman Jay Powell having his Volcker moment. However, history suggests he will behave otherwise and, even though substantially higher rates may be required, the Fed and other central banks will hesitate about delivering them. In the 1970s, it took a decade of hesitation before things got so bad, the Fed had to act. The odds are that if inflation is persistently high, the rate response of central banks will be inadequate. This will entrench inflation.

What of emerging markets?

This discussion has focused on developed market central banks in North America and Europe, which are currently at the centre of the inflationary storm. The US is always of critical importance because the dollar is the world’s reserve currency and a majority of financial assets are denominated in dollars. To a significant extent China is isolated by exchange control barriers and can go its own way. Currently its inflation is benign and, in response to a slowing economy, it is likely its monetary conditions will be eased.

During the pandemic, emerging markets did not enjoy the same freedom to lavishly print money to sustain economic activity as developed countries. They had to follow more conventionally prudent policies. As global inflation accelerated, emerging market central banks took the lead in increasing their interest rates, which generally, with a few notable exceptions, now are not too distant from what is appropriate for their domestic economic conditions. However, further increases in global inflation may require even higher rates, both to contain the passthrough into domestic prices and to sustain capital inflows as developed economies respond by further increasing their rates.

Learning how to cope with new circumstances

Inflation may be much higher and more persistent than is currently priced into financial assets. After 40 years of price stability, the market has become complacent about these risks. Economic history teaches us that long periods of price stability are the norm and inflation is an abnormality associated with wars, natural disasters and gross economic mismanagement. Unfortunately, we are experiencing all three of these conditions. The biggest danger is flawed economic policy. Huge fiscal deficits funded by lavish money-printing have put us on the brink of financial disaster.

We are going to relearn through trial and error how to cope with these challenges.

That we shall ultimately navigate through these difficulties I do not doubt. The narrative of the 1970s provides an encouraging message. Inflation was tamed and a long period of prosperity followed. However, people learn from their experiences rather than history. We are going to relearn through trial and error how to cope with these challenges.