The post-pandemic bounceback of the global economy is losing momentum, and many fear that developed economies may slip into recession. Sandy McGregor discusses some of the important changes impacting the outlook.

A notable achievement of mathematicians in the second half of the 20th century was to establish theoretically that, in the long term, we cannot accurately predict either the weather or the economy, because both are complex systems in which a small, unpredictable random event can have profound consequences for the system as a whole. This insight is well expressed when it is said that a butterfly flapping its wings in the Himalayas can trigger a hurricane in the Caribbean. Perhaps the most dramatic example of this was the 1914 assassination of Archduke Franz Ferdinand in Sarajevo, which precipitated a succession of events leading to the First World War, the rise of communism, the Great Depression of the 1930s, the Second World War and the Cold War.

The turbulence of the past two years could be the new norm.

In our times, the COVID-19 pandemic may prove to be a similar game-changer. While hopefully we do not have a world war in our future, the pandemic may have set us on a very different path from the one we have followed since the early 1980s, when market liberalisation and globalisation became the key determinants of global growth.

An uncertain world

I have been involved in financial markets for more than 50 years and have never sensed such uncertainty among market participants as I do today. This is not just a South African phenomenon. It is everywhere. It is as if people have sensed things are changing but do not know where we are headed. While there are occasional outbreaks of old-style exuberance, such as we have recently witnessed when the prices of companies expected to benefit from artificial intelligence soared, generally the mood is not joyful. The days when US President Ronald Reagan could be triumphally re-elected on the slogan “It is morning in America” are long gone.

A widely anticipated recession

Currently, there is the widely held view that developed economies are about to enter either a recession or at the very least a serious economic slowdown. This is in itself unusual. Normally the market ignores prophets of doom until disaster is about to strike, often citing the adage “this time it is different”. Since 1980, economic expansions following a major recession have lasted between eight and 10 years. This time the consensus is that the recovery following the pandemic disaster of 2020 is already petering out. Consensus forecasts are that in 2023 the US, European and Japanese economies will all only grow by about 1%. The slowdown is already visible in Europe, but the US and Japan remain fairly buoyant. The Chinese growth outlook is also being questioned, as its bounceback after the ending of draconian COVID-19 restrictions seems less sustainable than expected.

There are strong arguments supporting the view that we are entering a new world … which will have aspects very different from what we have experienced over the past 40 years …

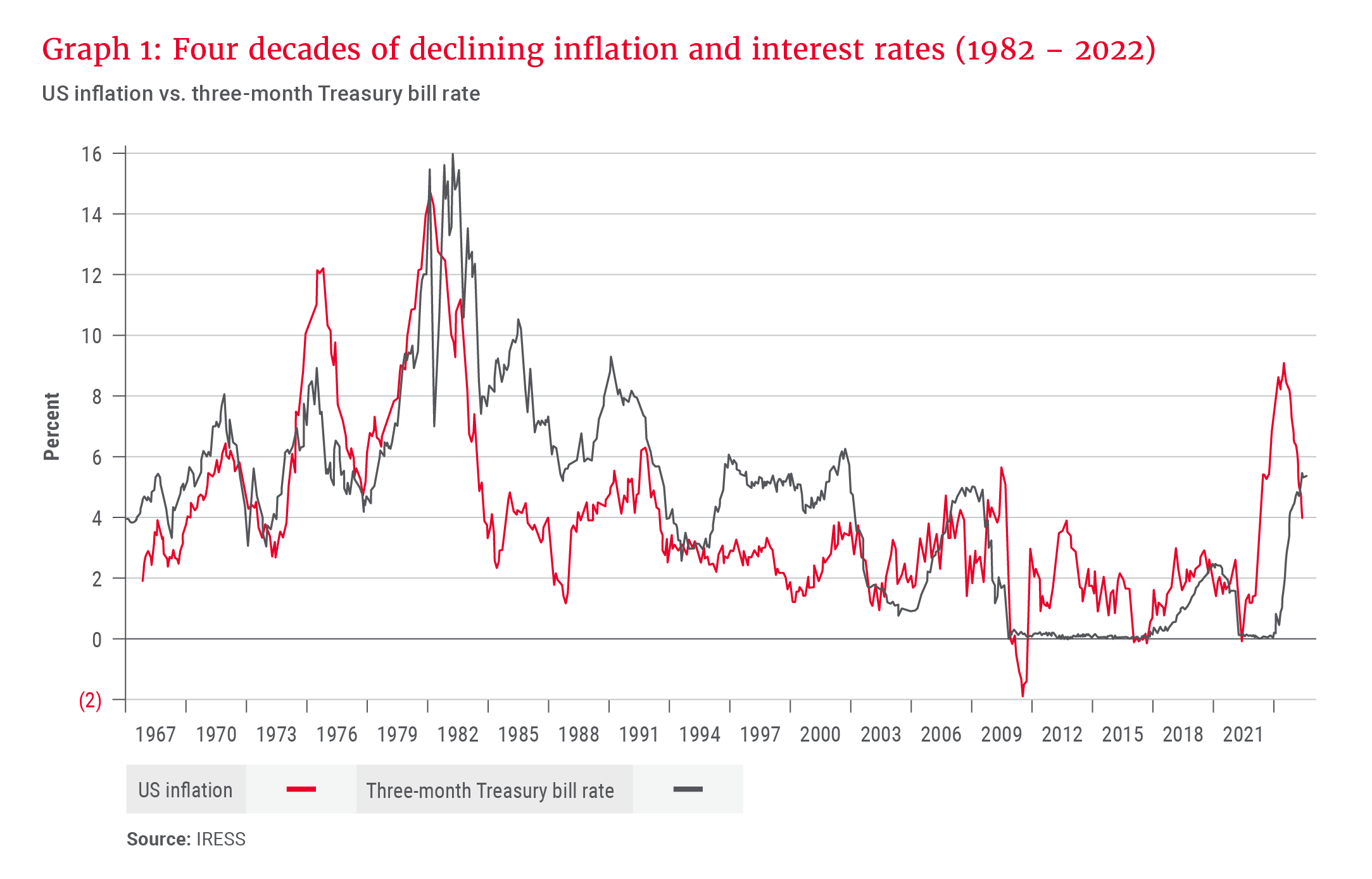

The important question is whether this slowdown is simply a readjustment as the world recovers from the dislocations caused by the pandemic, after which more sustainable growth will resume, or the start of a very different economic order. There are strong arguments supporting the view that we are entering a new world, whose workings we shall only understand in time, but which will have aspects very different from what we have experienced over the past 40 years, a feature of which was declining inflation and interest rates (see Graph 1 for the US experience).

The end of quantitative easing

Central banks responded aggressively to the banking crisis of 2008/9 to protect financial stability. However, once the crisis had passed, within developed countries they responded to what were regarded as unacceptably low economic growth rates by slashing interest rates to zero and in some countries even below zero. They also embarked on programmes of quantitative easing (QE), which involved printing money to buy financial assets, mainly government debt.

QE failed to produce the growth central banks expected, and its proponents had to retreat to the common argument in support of failed policies that without QE, things would have been much worse. However, while QE failed to produce growth, it had a dramatic impact on asset prices. As real estate is financed by debt to a greater extent than other asset classes, it is the asset class whose prices have been the most inflated by low interest rates. More than a decade of zero rates has promoted a reckless overpricing of property. History suggests deflating these property bubbles could take another decade.

In response to the dislocation caused by the pandemic, governments and central banks expanded fiscal deficits and printed even more money. In the US, where the Federal Reserve had started to raise interest rates, they were rapidly returned to zero. During the previous decade inflationary pressures had been benign, despite QE. Indeed, central banks were complaining that inflation was too low. Accordingly, there was widespread complacency about the possible inflationary consequences of the aggressive response to the pandemic.

While the initial financial actions in March 2020 were totally appropriate to preserve financial stability, governments operated under the illusion that ultra-low interest rates would be a sustainable feature of the financial system for many years to come. When inevitable inflationary pressures developed, central banks initially argued that these would be transitory and did not require tighter monetary conditions. They realised too late that they had triggered the biggest outbreak of inflation since the 1970s, which they are now struggling to control with ever-higher interest rates. Events have totally discredited the policies of QE and zero rates. We are returning to a world of higher interest rates such as prevailed in the 20 years that followed the 1982 recession, which crushed the inflation of the 1970s.

Unsustainable fiscal pressures

Almost all governments are facing ever-increasing obligations to provide healthcare and pensions. Generally, households’ accumulated savings are inadequate to fund retirement, especially as people are living longer. The pandemic seems to have accelerated demographic changes, notably a decline in birth rates. A contracting cohort of those of working age who pay taxes and rising numbers of retirees who receive benefits is a fiscal time bomb, which will increasingly dominate the political discourse over the next decade. Politicians have made promises which are unaffordable, but to which the beneficiaries of this largess are deeply attached. Recently in France, President Macron faced huge opposition when he forced through a relatively small increase in retirement ages. This is a precursor of struggles to come.

When central banks were printing money seemingly without adverse consequences, it was argued that this offered a solution to the fiscal challenges facing governments. The sudden return of inflation has discredited this argument. Expenditures will be restricted to what is affordable. Difficult choices will have to be made as to where fiscal spending is to be directed. There will be no easy choices.

The decarbonisation project

The decarbonisation project is gaining momentum. Regardless of its merits, it is going to cost a lot of money. It requires huge investment in the generation and distribution of electricity and the introduction of new technologies, which often are less efficient than what is being replaced. It is inherently inflationary.

The path to a low-carbon world is going to be long, difficult, and acrimonious.

Already governments are paying substantial subsidies to kickstart the process. However, given other fiscal challenges, the scope to increase these subsidies is limited and the cost will have to be paid by consumers. This financial burden will reduce what is available for other expenditures, disrupting traditional spending patterns. In Europe, the surge in energy prices last year has angered voters, who could well turn against incumbent governments. For example, polls indicate that in the past year in Germany, support for the Green Party has declined from 24% to 16%. The path to a low-carbon world is going to be long, difficult, and acrimonious.

Slower growth in China

In the first two decades of this century, China has been the locomotive of global growth. Its gross domestic product (GDP) has grown from US$1.2tn in 2000 to an expected US$19.4tn this year. However, this era of rapid Chinese growth is drawing to an end. It is facing increasing economic challenges. Its population is no longer growing. Prior to the pandemic it was expected that China’s population would peak in 2028. It now seems that its population already peaked in 2021. The country’s one-child policy has left a demographic legacy, which has serious adverse consequences. China may get old before it gets rich. Its growth has largely been driven by investment; normally as an economy reaches maturity, growth is increasingly driven by consumption. In China, consumer spending has never grown large enough to replace investment as the main source of growth.

Investment in housing has been a key driver of the Chinese economy. Estimates of the contribution of housing to its GDP range between 20% and 30%. Houses account for more than 60% of household wealth. However, the Chinese property sector is now in deep trouble and the government is intervening to prevent a collapse of house prices. Housing is expensive relative to incomes and there is no longer the spending power to support ever-rising prices. Potential buyers are approaching the market with more caution. Housing can no longer contribute to Chinese growth as it has up to now.

… there are not enough countries doing well to compensate for the impact of slower growth in China and the developed nations.

China has disappointed expectations that, with the ending of pandemic lockdowns, it would bounce back strongly. While the People’s Bank of China has cut interest rates, these are already too low for even lower rates to have a big impact. Aggregate debt is about 280% of GDP, the largest amount of which is owed by state-owned companies. It is no longer possible to drive the Chinese economy by perpetually increasing borrowings.

Japan reached a similar situation of overindebted companies in 1990 and it took 25 years of stagnation to fix the problem. Japan’s response was to invent the modern policy of QE. China may have to do something similar, which, given its low rate of inflation and the protection to its exchange rate provided by capital controls, it can do. However, its contribution to global growth will be much reduced compared to the recent past.

Which countries are doing well?

It is important to remember that there are always some countries which are prospering despite global economic difficulties. India is now the country with the largest population. It has been transformed in recent years by more effective infrastructure investment and the pro-business policies of the Modi government. It looks set to grow more than 6% this year and its growth path seems sustainable. The Middle East is booming on the back of high energy prices. Indonesia, which has a population of 274 million, is also set on a path of longer-term growth. However, there are not enough countries doing well to compensate for the impact of slower growth in China and the developed nations.

A bipolar world

The increased integration of the global economy after 1982 accounted for much of the prosperity of the four decades prior to the pandemic. Communism collapsed in Eastern Europe and Russia, and China became a market economy and the world’s biggest trading power. Sophisticated global supply chains reduced the costs of traded goods, increasing the well-being of consumers everywhere.

The pandemic caused supply disruptions, which have caused business and governments to question the robustness of these supply chains and manufacturing is moving back to be closer to key markets. This process has been accelerated by increasing tensions between China and the US and by Russia’s invasion of Ukraine. The world is dividing into two blocs. One is made up of the democracies of North America, Europe, Japan, Korea and Australasia. The other is Russia and China. As tensions rise, more money is being spent on armaments. The global trading system still operates but not as efficiently as it did in the past.

The ending of the savings glut

From 2003 onwards there was an increasing glut of global savings. Certain countries had significant current account surpluses which were recycled mainly into the dollar, the world’s reserve currency. In aggregate, savings exceeded the requirement for investment, which depressed interest rates. However, the major source of excess savings since 2008 has been the creation of money by central banks (QE, as explained earlier). In this period, the assets of the Federal Reserve System, the European Central Bank and the Bank of Japan have increased from US$4tn to US$22.2tn. Between them they have added US$18.2tn to the global savings pool. Most of this went to funding government deficits. Over the past year, as their primary policy objective has shifted from promoting growth to taming inflation, central banks, with the notable exception of the Bank of Japan, have reduced their funding of governments and are contracting their balance sheets.

… it looks as though the days of cheap money are over.

The immediate impact of this important policy change has been reduced by the availability of excess savings accumulated during the pandemic. There are various estimates of the size of the pool of excess savings, but it seems probable it will be exhausted within six to 12 months. This would place the full brunt of funding government deficits on private sector savings and the market could experience significant liquidity problems. Central banks will respond to ensure that markets have the liquidity they require to operate efficiently, but they do not wish to create too much money for fear of reigniting inflationary pressures. We have yet to see the full consequences of the ending of QE, but it looks as though the days of cheap money are over.

A Minsky moment

Hyman Minsky was an economist, who would surely have won the Nobel Prize if he had lived slightly longer. His key insight was that long periods of stability create instability. Stability allows market participants to take on more risk, notably by taking on more debt. It allows people to do crazy things, paying inflated prices for assets. The longer the stability lasts, the greater the excesses. Then there is a sudden collapse, often for some trivial reason, and the whole edifice comes crashing down. The Minsky moment is the point when this implosion commences.

A good example was the US subprime crisis, which blew up the world’s financial system in 2008. Years of increasingly irresponsible mortgage lending suddenly became unsustainable. That was a Minsky moment. Like most regulators and central bankers, Minsky thought stability was a good thing and that policy should promote it. He saw regulation as the solution to the problem he had identified. However, regulation is seldom effective because the regulators are always fighting the last war. The best solution is to allow a degree of instability, which eliminates excesses before they become threatening. That has not found favour among governments, which remain committed to maintaining stability.

Central banks used low interest rates and QE to maintain stability in the decade following the 2008 crisis. This was accompanied by an unsustainable absence of inflation. Our present Minsky moment was when inflation exploded out of control in 2022. This heralded the start of a new more turbulent time, characterised by higher inflation and interest rates and increasingly acrimonious political discourse, both between and within nations.

As the world emerges from the current economic slowdown, we should not expect that we shall return to the relatively stable conditions which prevailed between 2010 and 2019. We face challenges which governments and central banks will find difficult to control. The turbulence of the past two years could be the new norm.