The 2023 Budget speech was delivered against the backdrop of high living costs, a dismal unemployment rate and intensive loadshedding crippling businesses, all of which are placing severe strain on South Africa’s economic recovery and growth.

Finance Minister Enoch Godongwana provided some relief by proposing no significant tax increases to the major revenue-generating categories, such as personal income tax and value-added tax, for the 2023/2024 tax year. This signals continuity from the 2022 Budget and echoes the government’s commitment to economic growth, while acknowledging the adverse impact of tax increases.

The 2023 Budget includes several tax proposals designed to support businesses and individuals in coping with the higher cost of living. Tax relief of R13 billion is proposed to promote investments in green energy and to support businesses and individuals. Around 60% of government expenditure is allocated to the social wage to provide support to the most vulnerable and help alleviate poverty and hunger. Existing social grants have been increased to cushion against rising inflation.

Tax revenues have remained strong as a result of higher commodity prices and growth in corporate tax collections, but the profitability in the resource sector is declining, leading to lower corporate income tax revenue forecasts. We are also yet to experience the full impact of loadshedding on the country’s economic activity and the significant risk it poses to corporate income tax revenue collection.

Government spending continues to face an uphill battle, specifically in relation to public sector wage negotiations, additional spending pressures associated with state-owned enterprises (with little to no return on investment) and the country’s mounting debt-servicing cost. The success of this Budget will be determined by how effective government is in prioritising and tightening expenditure and putting resources to good use, while stimulating economic growth.

Below, we highlight some of the 2023 Budget tax proposals that may impact investors. These changes come into effect on 1 March 2023, unless otherwise indicated.

What were the highlights?

The key take-outs from this year’s Budget are summarised below:

- The personal income tax brackets and rebates have been adjusted in line with the expected inflation rate of 4.9%.

- An upward adjustment of 10% has been made to the tax brackets for retirement fund lump sum benefits (both before and at retirement) and transfer duties. The applicable tax rates remain unchanged.

- Individuals who install rooftop solar panels will be entitled to a tax rebate of 25% of the cost of the panels, up to a maximum of R15 000, to promote additional electricity generation. This incentive will only be available for one year and is not available for inverters or batteries.

- No changes have been made to the general fuel levy or the Road Accident Fund levy to reduce pressure on households and businesses.

- Excise duties on alcohol and tobacco (known as sin taxes) will increase by 4.9% in line with expected inflation.

- The diesel fuel levy refund will be extended to food manufacturers for a period of two years, from 1 April 2023 to 31 March 2025, to limit the impact of power cuts on food prices.

The following applies for the period from 1 March 2023 to 29 February 2024, unless otherwise stated:

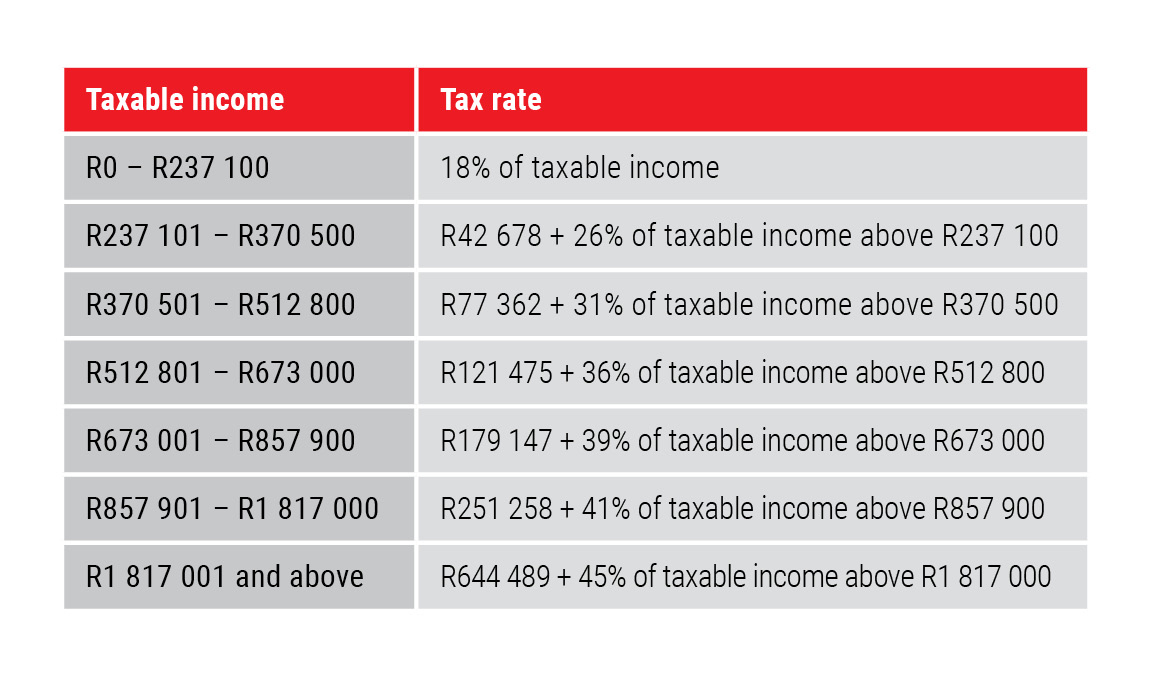

Individuals and special trusts

Personal income tax brackets will be fully adjusted for inflation for the 2023/2024 tax year. The highest marginal tax rate for individual taxpayers remains unchanged at 45%. The personal income tax rates for the 2023/2024 tax year are listed below.

Tax thresholds

The tax-free thresholds for personal income taxes will also be adjusted for inflation for the 2023/2024 tax year to the following:

- R95 750 for taxpayers younger than 65

- R148 217 for taxpayers age 65 to 74

- R165 689 for taxpayers age 75 and over

Rebates

The primary, secondary and tertiary rebates (deductible from tax payable) will increase to the following:

- R17 235 per year for all individuals

- R9 444 for taxpayers age 65 and over

- R3 145 for taxpayers age 75 and over

Medical tax credits

Monthly tax credits for medical scheme contributions will increase to the following:

- R364 per month per beneficiary for the first two beneficiaries

- R246 per month for each additional beneficiary

Companies

Reminder: Corporate tax rate reduction

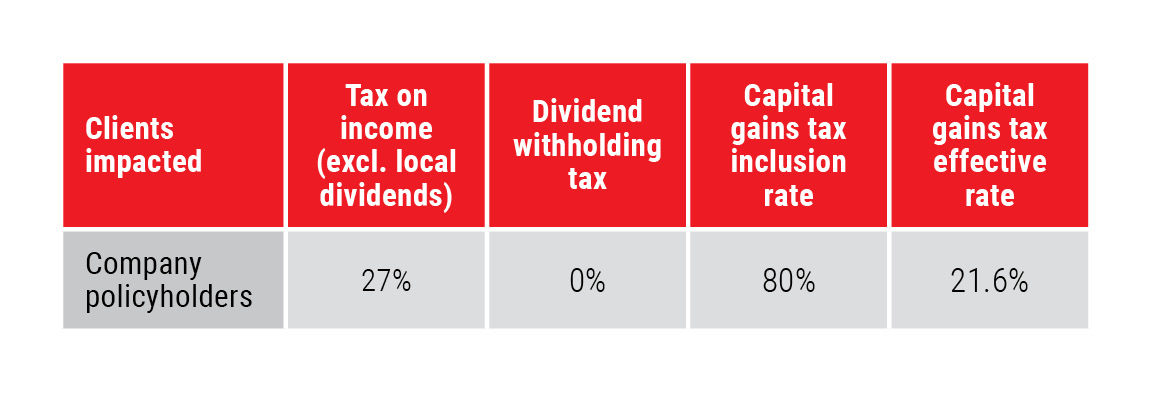

In the 2022 Budget speech, it was announced that the corporate tax rate would be decreasing from 28% to 27%, effective for years of assessment ending on or after 31 March 2023.

This change becomes effective for company policyholders in the Allan Gray Endowment from 1 March 2023, and Allan Gray will withhold tax at the following rates:

Capital gains tax (CGT)

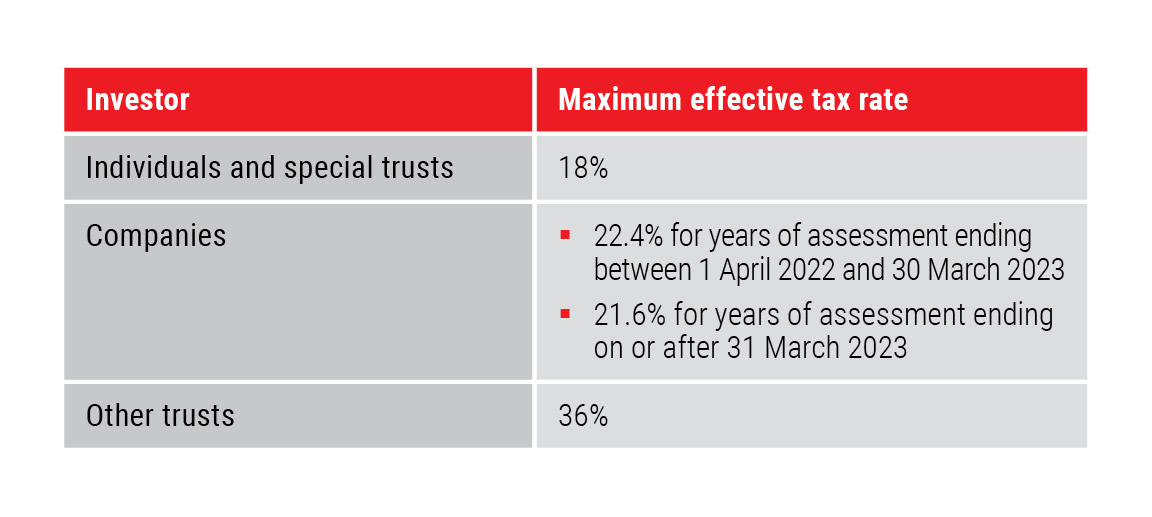

The CGT inclusion rate for individuals and special trusts remains at 40%, and for other taxpayers at 80%.

The annual exclusion for a capital gain or loss granted to individuals and special trusts remains at R40 000. The exclusion granted to individuals remains R300 000 in the year of death.

Trusts

The income tax rate for trusts (other than special trusts) remains unchanged at 45%.

Interest exemptions

The local interest exemptions remain unchanged:

- The exemption on interest earned for individuals younger than 65 years remains R23 800 per annum.

- The exemption for individuals 65 years and older remains R34 500 per annum.

Foreign interest remains fully taxable.

Dividends tax

Dividends tax remains at 20% on dividends paid by resident and non-resident companies for shares listed on the JSE.

Foreign dividends received by individuals from foreign companies (shareholding of less than 10% in the foreign company) are taxable at a maximum effective rate of 20%.

Interest withholding tax for non-residents

Interest withholding tax remains at 15% on interest from a South African source payable to non-residents. Interest is exempt if payable by any sphere of the South African government, if payable by a bank or if the debt is listed on a recognised exchange.

Tax-free savings account

The annual cap on contributions to tax-free savings accounts remains at R36 000 from 1 March 2023, with the lifetime limit also remaining at R500 000.

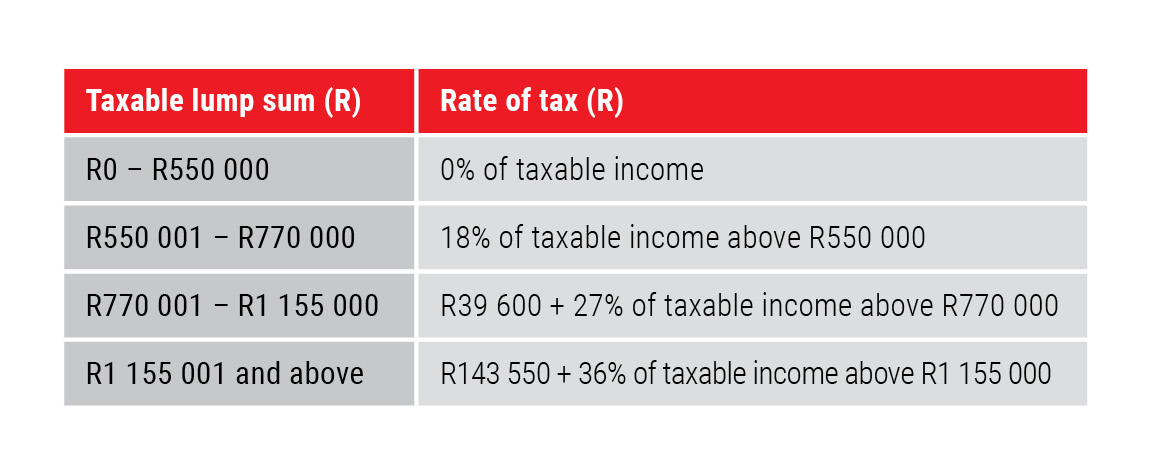

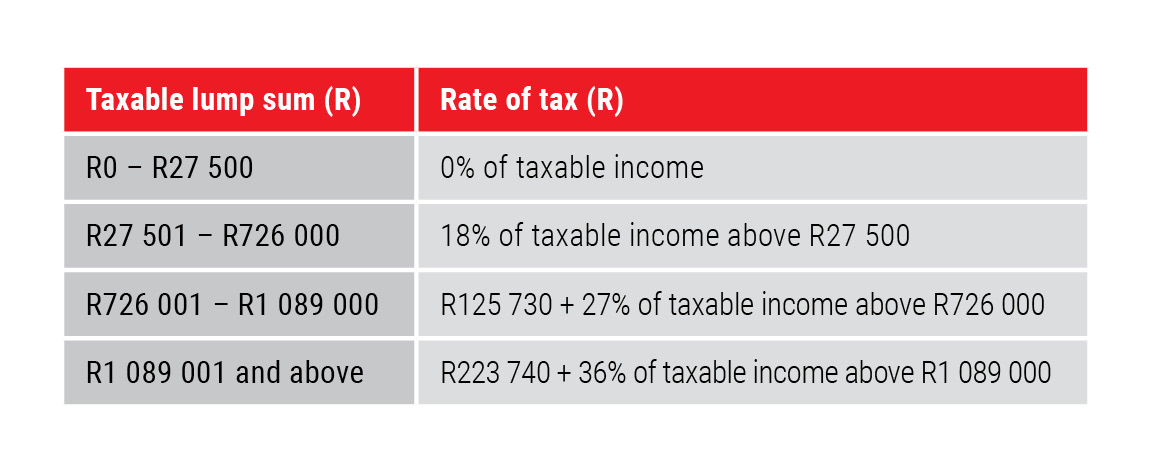

Retirement lump sum taxation

At retirement

The first R550 000 of a retirement lump sum will be tax-free. The table below illustrates how retirement lump sums will be taxed:

Pre-retirement

The first R27 500 of a pre-retirement lump sum withdrawal will be tax-free. The table below illustrates how withdrawal lump sums will be taxed:

Value-added tax

Value-added tax is charged on the supply of goods and services provided by registered vendors. It remains at 15%.

Estate duty

Estate duty is levied on property of residents and South African property of non-residents, less allowable deductions. The duty is levied on the dutiable value of an estate at a rate of 20% on the first R30 million and at a rate of 25% above R30 million.

A basic deduction of R3.5 million is allowed in the determination of an estate’s liability for estate duty. The tax rates and deductions remain unchanged from last year.

Donations tax

Donations tax is payable on the value of property disposed of by donation. It is levied at a flat rate of 20% on the cumulative value of property donated since 1 March 2018 not exceeding R30 million, and at a rate of 25% on the cumulative value of property donated since 1 March 2018 exceeding R30 million.

The first R100 000 of property donated each year by an individual is, however, exempt from donations tax. The tax rates remain unchanged from last year.

Additional tax proposals for the 2023 legislative cycle and beyond

Two-pot retirement system

The first phase of the legislative amendments to the retirement system is due to take effect on 1 March 2024, following extensive public consultation. The purpose of the amendment is to enable pre-retirement access to a portion of a member’s retirement assets (this portion will be called the “savings pot”), while protecting the balance for retirement (this portion will be called the “retirement pot”). The tax deductibility of contributions will remain unchanged. Withdrawals accruing before 1 March 2024 will still be taxed according to the pre-retirement lump sum tax tables, while pre-retirement withdrawals from the savings pot will be taxed at marginal tax rates. At retirement, any remaining amounts in the savings pot will be taxed according to the retirement lump sum tax table (in other words, with the first R550 000 retirement lump sum being tax-free).

Additional work is still required on the following: A proposal for seed capital; legislative amendments to incorporate defined benefit funds; legacy retirement annuity funds; and withdrawals from the retirement pot if a member is retrenched. The first three items will be clarified in the upcoming draft legislation, while the last matter will be addressed in the second phase of implementation.

Apportioning the tax-free investment contribution limit and limiting retirement fund contributions when an individual ceases to be a South African tax resident

An individual’s year of assessment ends on the day immediately before the day on which they cease to be a resident for tax purposes in South Africa. Their subsequent tax year commences on the day on which they cease to be a tax resident. This effectively creates two years of assessment during a 12-month period in this scenario.

The Income Tax Act was amended in 2022 to provide for the apportionment of the annual interest exemption and to limit the CGT annual exclusion when an individual ceases to be a South African tax resident, so that they do not benefit twice in one 12-month period. Similarly, it is proposed that changes be made to apportion the tax-free investment contribution limit and the annual limit on the deduction of retirement fund contributions in a 12-month period for individuals ceasing to be South African tax residents.