A surge in enthusiasm for AI-related companies has created an unusually narrow Japanese equity market, with a small group of stocks driving a disproportionate share of returns. Alex Bowles and Brett Moshal from our offshore partner, Orbis, discuss the positioning of the Japan Equity Strategy and why they remain focused on uncovering high-quality businesses trading at attractive valuations beyond the market's dominant AI theme.

A symbol of Japan's export-led, industrial economy, Toyota Motor held the title of Japan's most valuable company for over 20 years. But in recent weeks the carmaker was dethroned by SoftBank Group – Masayoshi Son's technology giant – reclaiming the top spot it last held at the peak of the dot-com bubble in 2000. SoftBank's huge investments in British semiconductor designer Arm and in OpenAI, the maker of ChatGPT, drove the stock to new highs as investor excitement around AI continued to build. By early June, shares in SoftBank had risen more than threefold since the start of 2025, with OpenAI's widely anticipated IPO, expected to value the company at over a trillion dollars, yet to come.

But SoftBank's reign at the top was short-lived. Kioxia – a memory chip manufacturer that was spun out of Japanese giant, Toshiba, in 2017 – in recent weeks has eclipsed both SoftBank and Toyota to claim the top spot. Remarkably, Kioxia only listed in late 2024, with an IPO that garnered little investor attention. More remarkable still is the fact that the listing had been delayed due to concerns around the lack of investor interest.

Despite a tricky start, Kioxia's subsequent rise has been extraordinary. Explosive demand for Kioxia's memory chips has sent company profits soaring and sent the share price stratospheric. Over the past 18 months, shares in Kioxia are up more than 50-fold.

Even outside the obvious AI beneficiaries, almost any company that touches the AI supply chain has seen its share price soar. Specialist manufacturers of materials such as silicon, ceramics, and glass fibre cloth have seen their fortunes rise as supply-chain bottlenecks tighten. SUMCO, a producer of silicon wafers used in semiconductors, and Nitto Boseki, a manufacturer of the specialist glass fibre cloth used in AI chip substrates, are two such examples. Both companies' share prices were up more than threefold in the last 18 months.

Perhaps more unexpected still are Ajinomoto – best known for producing MSG – whose shares have surged on the basis that its amino acid technology has applications in semiconductor packaging and Toto, the toilet maker, whose specialist ceramic electrostatic chucks are used to handle silicon wafers during semiconductor manufacturing. These are not obvious AI winners, but the market has been quick to handsomely reward any business with links to the AI supply chain.

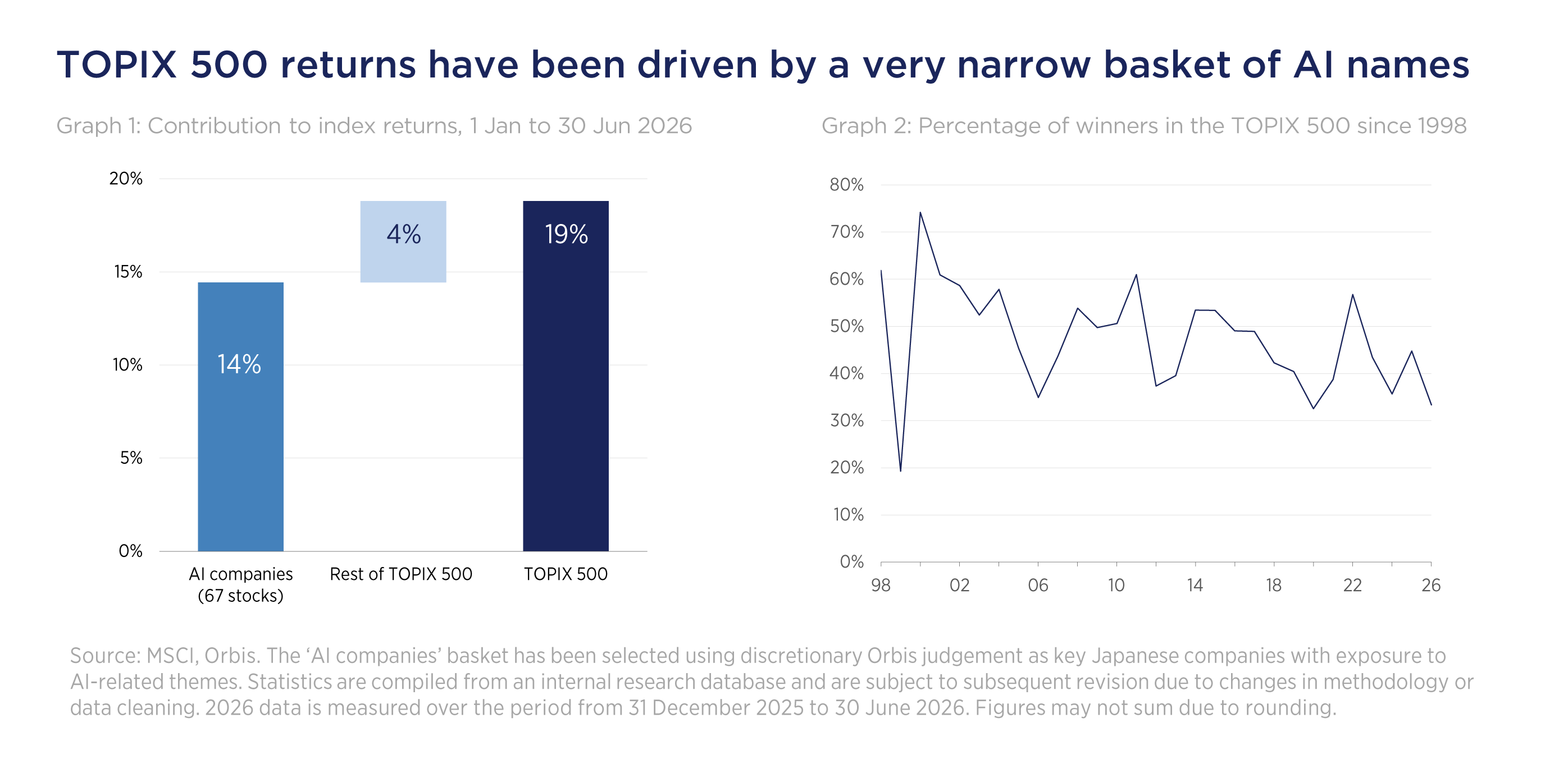

The result has been an unusually narrow, yet powerful market, as shown in Graph 1 and Graph 2 below. Year to date, only a third of stocks in the TOPIX 500 have delivered benchmark-beating returns, yet the index has enjoyed one of its best starts to the year in decades.

Meanwhile, our positioning away from the AI-related action has meant that we have missed out on much of these returns. Our hit rate has been poor, with only around 25% of names in the portfolio outperforming the index year to date Having little exposure to AI names has been painful, but in most market environments there are multiple paths to outperformance. This year, the market has rewarded AI exposure above almost everything else. Tellingly, four of our five largest winners were names related to the AI supply chain.

Leading the portfolio's winners this year is Sumitomo Electric Industries (SEI), a name we have discussed in recent commentaries and a stock we have owned consistently for over seven years. For most of that time, SEI was regarded as a supplier of automotive wire harnesses, overlooked by the market, with its share price going broadly nowhere. The company has since undergone a remarkable transition, quadrupling in value since the start of last year. Surging demand for its energy-efficient optical devices and connectors, driven by the rapid build-out of data centre capacity, has transformed both the earnings trajectory and the market's perception of the business.

Among other winners in the portfolio have been Rigaku, a company that makes X-ray-based equipment – historically for use in research labs – but more recently their technologies have been applied in the semiconductor manufacturing process. We exited the position in May with the share price having more than tripled since our first purchase just seven months earlier as the market came to recognise the value in the company.

Misumi has been another portfolio beneficiary of AI-driven infrastructure growth. The company produces bespoke parts used in factory automation and data centres – both areas seeing rising demand as AI investment accelerates. Its share price has doubled over the past year.

Looking beyond the crowd

While we have seen some extraordinary market moves in the AI-related names, the apathy towards anything outside of AI is just as striking. Such an environment – when capital floods so decisively into a single theme – can be hard for contrarian investors to keep up with in the short term. But it is precisely in such moments that the most compelling opportunities tend to emerge, for those with the courage and patience to look elsewhere.

Our contrarian philosophy means we are more than comfortable being early, so long as we are paying the right price. Overpaying, or simply following the crowd, is another matter entirely. This environment has given us the opportunity to meaningfully upgrade the quality of the portfolio, adding businesses we have long admired at valuations we have not seen in years – precisely because others are looking the other way.

GMO Payment Gateway is a case in point. The payments industry has been seen as a potential "AI loser". Consequently, the stock has underperformed the market by more than 20% this year despite continuing to deliver stellar earnings growth and now trades near a historical low valuation. We are less concerned, and GMO Payment Gateway now sits as the largest holding in the Orbis Japan Equity Strategy. In our view, the company's stellar track record speaks for itself, having compounded earnings by around 25% per annum for over two decades. In our view, the future looks bright – we forecast earnings per share to compound at around 15% per annum over the next 6 years, driven by several structural tailwinds, including rising e-commerce and a shift to cashless payments in Japan. At the helm, founder Issei Ainoura has proven himself as an outstanding executor, and we have every confidence he is the right person to navigate the company through the challenges and opportunities of the AI era.

Nintendo tells a similar story. Few companies' products are as universally loved as Nintendo, yet since peaking in August, the share price has halved, facing two AI-related headwinds in quick succession. Surging memory prices, as hyperscalers hoover up supply to build out AI infrastructure, have raised input costs and will likely squeeze near-term margins. Meanwhile, the market has grown anxious that AI could disrupt Nintendo's existing business model, making game development more accessible to new entrants and potentially eroding its competitive advantage in content.

In our view, both concerns are overblown. Mario, Zelda and Pokémon have proven resilient through decades of technological change – we don't think the introduction of AI will be any different. At half the price it fetched nine months ago, we believe the current share price represents compelling value for one of the world's most recognisable and resilient franchises in entertainment, with earnings potential of its intellectual property still largely untapped.

GMO and Nintendo are just two examples. Across the portfolio, we see the same pattern: businesses with strong fundamentals, proven track records, and clear long-term potential, trading at valuations that are too good to ignore.

Whether the ascent of SoftBank and Kioxia to the top of Japan's corporate ladder marks a permanent changing of the guard, or just the latest chapter in a long history of Japan's evolving market, is difficult to call. What we do know is that, in the shadows of these fast-moving technological giants lie plenty of overlooked, high-quality businesses trading at very attractive prices. Identifying such businesses, while the market looks elsewhere, is the essence of what we do.