In this commentary, Stefan Sommerville from our offshore partner, Orbis, examines the growing concentration risk in emerging market indices and explains how the Orbis Emerging Markets Strategy seeks to achieve genuine diversification through high-quality businesses with different long-term return drivers.

A passive investor buying the MSCI Emerging Markets Index today is not buying a diversified collection of businesses, spread across the developing world’s most promising economies. They are, in large part, buying a bet on semiconductors and artificial intelligence – concentrated in a handful of companies in Taiwan and Korea whose combined weight in the index has grown to levels that may give any prudent portfolio manager pause.

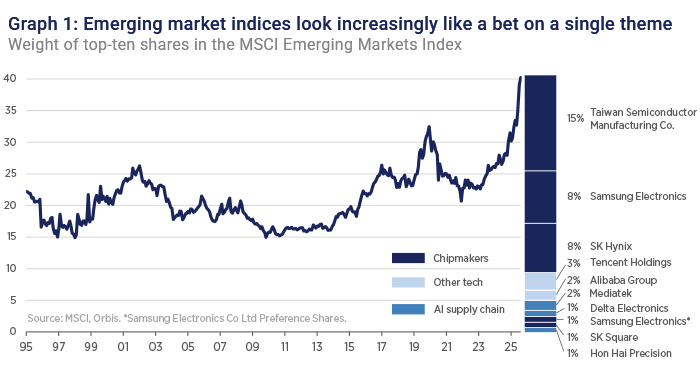

Taiwan Semiconductor Manufacturing Co. (TSMC) alone now accounts for over 15% of the MSCI Emerging Markets Index, as shown in Graph 1. The top ten names account for more than 40% of the entire index, with eight of those ten – TSMC, Samsung Electronics (including preference shares), SK Hynix, Mediatek, Delta Electronics, SK Square and Hon Hai Precision – all players in the AI infrastructure buildout. The index thus provides an illusion of broad geographical diversification. In reality, a passive investor buying EM exposure today is making a concentrated wager on the AI investment cycle, dressed up as a diversified allocation to the developing world.

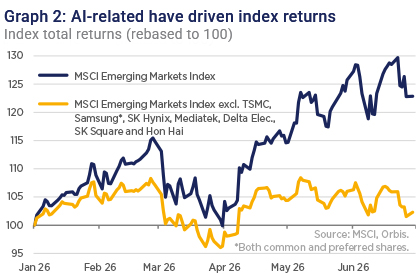

In recent months, that concentration has been both driven and fed by extraordinary returns. The race to build out data centre capacity has created a voracious demand for semiconductor chips, turbocharging the earnings and share prices of the companies that make them. The impact of this AI rally has been stark: just those eight mega-cap AI-related names account for 90 percent of the index returns so far in 2026, as shown in Graph 2.

To be clear, this is not a criticism of these businesses – far from it. TSMC is the largest holding in the Orbis Emerging Markets Strategy and Samsung Electronics is also a top-five position. We think both are excellent businesses – well deserving of their place in your portfolio and still attractively valued despite the recent sharp increase in share prices. Like every share in the portfolio, the position sizing of these names is driven by our conviction in each stock’s risk-adjusted return profile, weighed up against the opportunities available elsewhere. We pay little attention to a stock’s weight in the benchmark.

But despite owning both TSMC and Samsung, the levels of concentration in the index and the outstanding relative performance of AI-related stocks has meant the Strategy has lagged its benchmark so far this year. While underperformance can be uncomfortable, we believe that being highly selective – building a concentrated portfolio of excellent businesses with diversified drivers of returns – gives us the best chance of delivering attractive long-term returns for our clients. Our portfolio today reflects that conviction.

We own a collection of businesses, selected not because of their index weight but because of the quality of their competitive positions, the integrity of their management, and the price at which their shares are available. Some of those businesses are large. Others are absent from most investors’ radars, tucked into corners of the index that passive flows have largely ignored. What they share is that we understand them, we trust the people who run them, and we believe we are paying a price that is below what they are genuinely worth to own them. Crucially, where they differ is in what each business needs to go right to deliver returns.

We own TSMC and Samsung, and for those holdings returns are indeed tied, in part, to the AI investment cycle. Both are central to the global semiconductor industry and are exceptionally well positioned within their respective segments. We are comfortable with that exposure at the valuations we paid. Beyond those holdings, however, the portfolio looks very different from the index.

Consider Nu Holdings. Nu is a Brazilian digital bank whose fortunes are tied to financial inclusion in Latin America, the Brazilian interest-rate cycle, and its ability to underwrite consumer credit at scale responsibly. It serves more than 135 million customers across Brazil, Mexico and Colombia, and continues to take share from incumbent banks that have historically underserved consumers.

While also a financial services business, Estonian-founded payments company Wise is different again. Its opportunity lies in taking share from incumbent banks in cross-border payments. Despite offering a faster, cheaper and more transparent service, Wise’s market share remains small relative to the size of the addressable market. Its future depends far more on customer adoption than on AI spending, semiconductor demand or broader economic growth.

Our two largest Chinese holdings – Tencent and NetEase – both in the Media & Entertainment sector, demonstrate the diversification on offer, even within a single country’s sector. Tencent’s prospects are tied primarily to digital advertising, fintech and the monetisation of its ecosystem. NetEase’s depend on its ability to continue developing successful games and allocating capital prudently. Both are Chinese media businesses, but they are reliant on very different drivers to be successful.

Jardine Matheson provides yet another source of differentiated returns. Its fortunes are tied to Asian consumer spending, Indonesian infrastructure activity, Hong Kong commercial property and the capital-allocation decisions of a family-controlled owner with an unusually long-time horizon. Those drivers bear little resemblance to the factors influencing semiconductor demand or AI investment.

AI investment. Brazilian financial inclusion. Cross-border payments. Chinese digital advertising and gaming. Hong Kong office rents. Indonesian infrastructure. These businesses need very different things to go right. They serve different customers, operate in different currencies, and are managed by people with different incentives and time horizons.

That, to us, is genuine diversification. Not simply a large number of stocks spread across multiple countries, but a collection of businesses whose long-term outcomes are driven by fundamentally different factors. Periods of underperformance are uncomfortable, but for portfolios built with little regard for index weights, they are inevitable in environments where a narrow group of stocks drives market returns.

The portfolio today trades at roughly 11 times this year’s estimated earnings – at close to a 20% discount to the index. Yet we believe our businesses and the entrepreneurs who run them are, on average, of higher quality than the index as a whole: stronger competitive positions, better balance sheets, higher returns on equity and more attractive long-term growth prospects. In our view, that discount reflects areas of the market where sentiment remains weak, not businesses whose long-term prospects have deteriorated.

Emerging markets indices increasingly have a concentration problem. For passive investors, that is simply the hand they are dealt. For us, it is a reminder of why we invest the way we do – selecting businesses one at a time, on their own merits, without regard for what the index tells us to own. The portfolio that results looks different from the index, performs differently from the index, and is valued differently from the index. In our experience, that difference – a focused collection of good businesses bought at attractive prices – is precisely what creates the conditions for strong long-term returns.

Article

Offshore investing