Defensive shares are normally a safe place to “hide” when valuations look high, but Orbis is currently finding more opportunities among cyclical shares where prices have remained more depressed. Ben Preston looks at consumer staples and the autos sectors, including a fascinating look at electric cars, as he explains where Orbis is currently finding value.

The current environment is quite unusual. In past stock market booms, cyclical shares have usually outperformed defensives. This is because booms tend to happen when the economy is strong and cyclical companies with greater economic sensitivity do better. As the economy contracts, stock markets fall and less economically sensitive or “defensive” shares often outperform the cyclicals. However, the current stock market advance has been led by defensive shares, which means that they are no longer a safe place to hide. Instead, it’s the cyclical shares that are more depressed today and which appear to offer better value.

The perception of risk versus actual risk

Like Allan Gray, Orbis believes risk is something very different from volatility. We define risk as the probability of losing money over the long term as a result of overpaying for assets rather than short-term market gyrations. To Orbis, cheap cyclical stocks may currently feel riskier than their defensive counterparts, but given the price discount, might actually prove safer in the long run.

Autos vs consumer staples

A look at the autos and consumer staples sectors illustrates this point. Historically the autos sector has been viewed as a low-quality, economically sensitive sector with cyclical earnings and low margins. The consumer staples sector, on the other hand, has been seen as a high-quality sector with less earnings sensitivity, lower volatility and higher margins.

In the past there hasn’t been much of a gap between the valuations of the two sectors. But over the last two or three years, the gap has become very large – per unit of earnings, you now pay about half as much for a car company as for a consumer staples company. In Orbis’s view, this makes the autos sector a more attractive prospect.

There are a few reasons why investors in general are pessimistic about car companies. Firstly, global demand for automobiles is already relatively high, so investors – particularly those with a short-term perspective – are worried about earnings declines. Secondly, investors are concerned about the growth of electric cars, produced by the likes of Tesla – they are worried that traditional car manufacturers, like Honda, won’t manage the transition well. But it’s not quite that simple, and an opportunity emerges when one looks more closely.

Honda vs Tesla

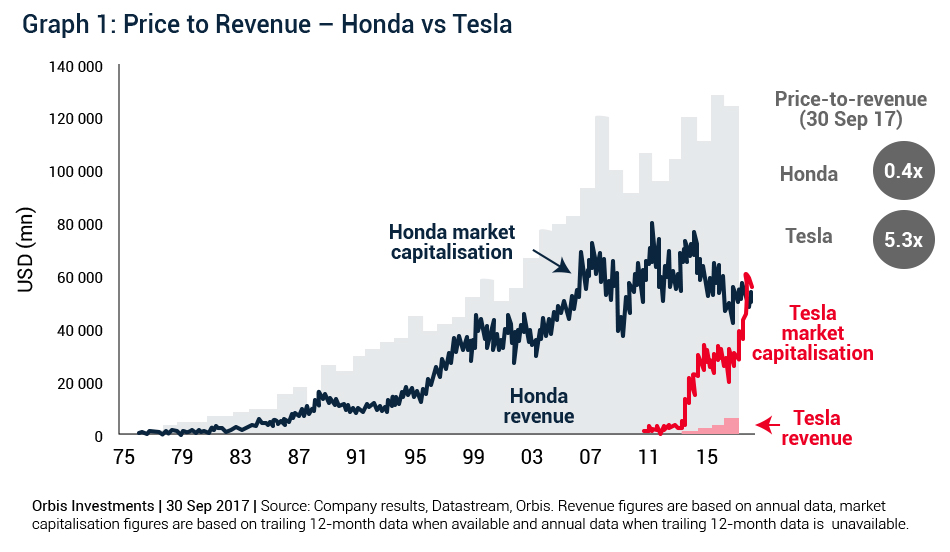

Graph 1 compares the market capitalisation and revenue of Honda and Tesla. It is remarkable that investors have allowed themselves to be so convinced of Tesla’s future success that they are now saying Tesla is worth more than the whole of Honda, even though Honda has 10 times the revenue. Bear in mind that in a decade of existence, Tesla has never been profitable. And, in the last four decades, Honda has never been unprofitable.

It is important to acknowledge that Honda’s earnings have historically been cyclical. The company experienced a big decline in earnings from the mid-80s to the mid-90s, and again in the global financial crisis. But even during those periods, Honda’s shares have only rarely – and only very briefly – traded for less than tangible net asset value. On average, its shares have traded at a 50% premium to net asset value, but today investors can buy them at a 10% discount. In the context of a stock market that looks quite expensive overall, Orbis believes that Honda shares look like pretty good value.

What about the edge Tesla has over Honda when it comes to electric cars?

The future of electric cars is highly uncertain, but Orbis’s research indicates there is a lot of growth to come. But Tesla won’t be the only beneficiary. In fact, most of the big auto manufacturers – Honda included – are now developing electric vehicles of their own, and Tesla will face far more competition in the future than it does today.

Another thing to consider is that Honda doesn’t only make cars—it also makes motorcycles and has a finance division. When looking at Honda’s intrinsic value, one needs to look at the different parts of the business and add them together. Roughly speaking, the car business is worth about JPY3 trillion, JPY2 trillion for the motorbikes, and another JPY2 trillion for the finance division – about JPY 8 trillion in total. This is considerably greater than the current stock market price of just JPY6 trillion.

But do electric cars specifically offer opportunity?

Until recently, the consensus view was that electric vehicle penetration would be a long and gradual process. However, within the industry, people are beginning to change their mind. Back in 2014 Continental, one of the world’s biggest auto parts suppliers, predicted that electric vehicle sales would reach about 1 million by 2025. But already over a million electric cars have been sold, so they’ve had to raise their estimates up massively, to 11 million.

It is quite possible that electric cars are simply a better product than combustion vehicles, in the same way that digital cameras are just better than film. Of course there are select opportunities outside of the vehicle manufacturers themselves to benefit from the shift to electric cars without paying over the odds.

Orbis has identified Samsung SDI, a subsidiary of Samsung Electronics, as one of these opportunities. Samsung SDI supplies Samsung with its batteries and also owns a stake in Samsung Display Corporation, which makes the best phone screens in the world. And, on the side, it has built on its skill in phone batteries to start making batteries for electric cars and home energy storage, because those are all based on the same chemistry. Batteries are the critical new component of an electric car.

There are various types of battery: cylindrical versus prismatic and pouch (which are similar).

Cylindrical are the easiest to produce. The anode, separator and the cathode are layered and rolled into a cylinder. The batteries have good energy density, but the chemical mix is quite unstable. To make them safe, lots of small cells are connected together, which wastes a lot of physical space. Also, because they are cylindrical, they don’t stack together very efficiently.

Pouch and prismatic batteries use a slightly different chemical mix, which has more natural stability. They are put together in flat layers, which is harder to do, but makes better use of space. Also, these batteries can be charged and discharged more times, so you get a longer life. However, they are more difficult to produce. They are also more expensive up front, but they work out cheaper per charging cycle. As the market matures, an increasing number of equipment manufacturers are choosing prismatic or pouch batteries. The big question: are there going to be enough of these batteries to meet demand?

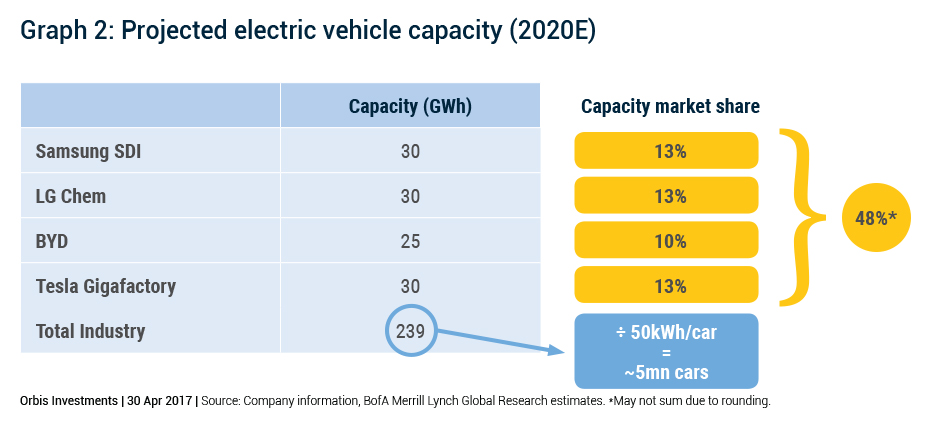

Graph 2 shows an estimate of battery capacity in 2020, with four companies that are likely to dominate. The industry overall is going to have capacity of a little under 250 gigawatt hours. But to get the required driving range, each car is going to need a battery of about 50 kWh, so we’re looking at enough capacity to supply 5 million cars. That’s only 5% of the total car market.

Samsung SDI currently makes no money from car batteries – in fact, it is slightly loss-making. While some investors feel this will persist, Orbis believes that if demand for batteries exceeds supply, as Graph 2 suggests it might, this will change. Orbis therefore sees plenty of potential.

How do these opportunities compare to the overall market?

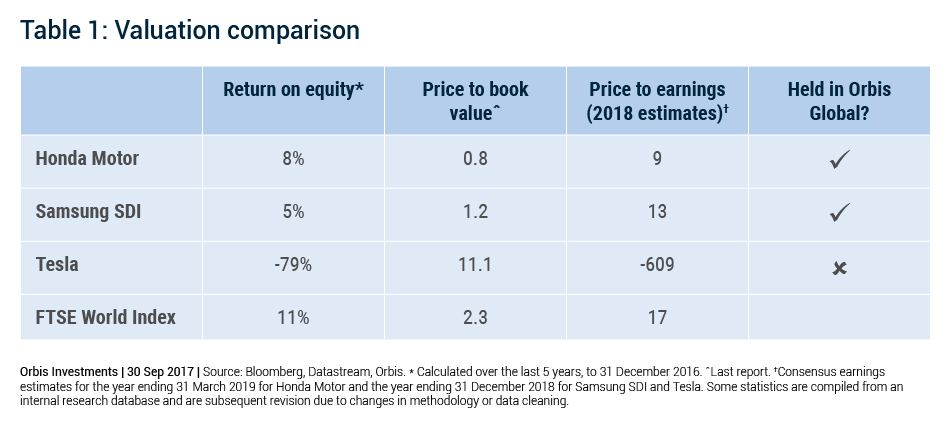

If you look at the average stock in the FTSE World Index today, you’re paying an average of over twice the net asset value, and 17 times next year’s earnings. If you compare that to Honda and Samsung SDI, you’re paying a much lower earnings multiple and around half the price per unit of book value, as shown in Table 1. Of course Orbis could be wrong but, when compared to Tesla, where investors are paying more than 11 times net asset value for a company which makes losses, the odds appear to be in our favour.