It can be difficult for investors to choose an investment manager when many of us seem to sound and look the same. Using Woolworths as an example, Andrew Lapping asks investors to judge us on what we do and not only on what we say.

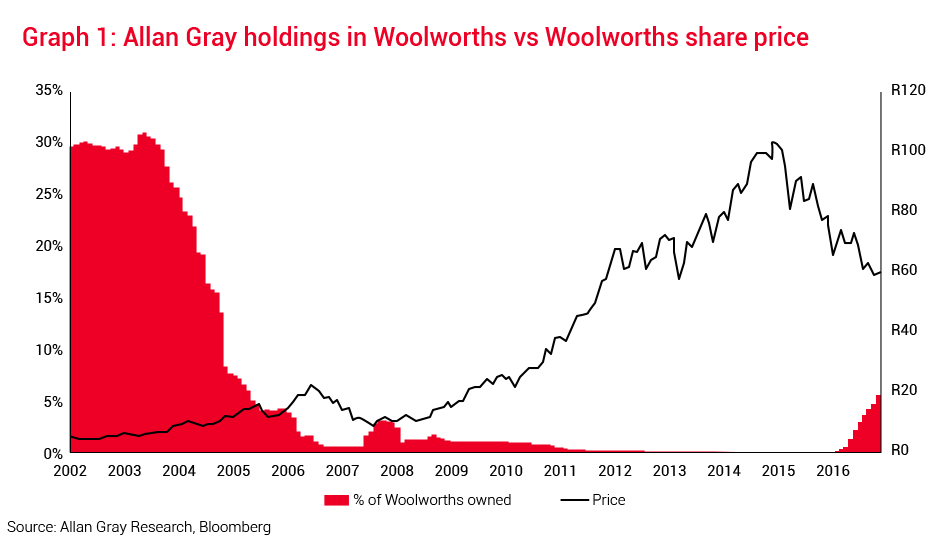

Allan Gray’s approach in practice is best illustrated by looking at our history with Woolworths since 2002. In the early two thousands our clients owned approximately 30% of the company. At the time, earnings were low and investors were only willing to pay about ten times these depressed earnings. Investors were concerned about weak consumer spend and the potential impact of spending moving to cell phones and gambling.

So, what did we see in Woolworths? To quote a portfolio manager at the time:

“Strategically, we believe Woolies is a solid company holding a secure position in the South African retail market. Our expectations are for a sustained improvement in earnings and ROE as management successfully implements its stated strategies.” - Quarterly Commentary 3, 2002

Two years later the story had changed as retailer earnings recovered strongly as consumer spending picked up. As the stock approached our fair value (R16) we began selling and sold out in 2006, as shown in Graph 1.

And so it remained for ten years.

Over the period from 2006 through 2016 Woolies traded above our estimate of fair value so we did not hold a position (except for brief period in 2008). Over this time the business performed well, growing sales and margins, taking market share in food and expanding into Australia. Our estimate of intrinsic value grew steadily but not to the extent priced in by the market: At one stage in 2015 the share traded at 26 times earnings and a 2.4% dividend yield as investors priced in perpetual growth. Over the past two years the South African consumer has fallen on tough times and the Australian acquisition has not performed as management hoped. Investors are now pricing in very little future growth and the share now trades on 13 times earnings and a 5.6% dividend yield. Most importantly the price has moved below our estimate of fair value and we have begun to accumulate a position.

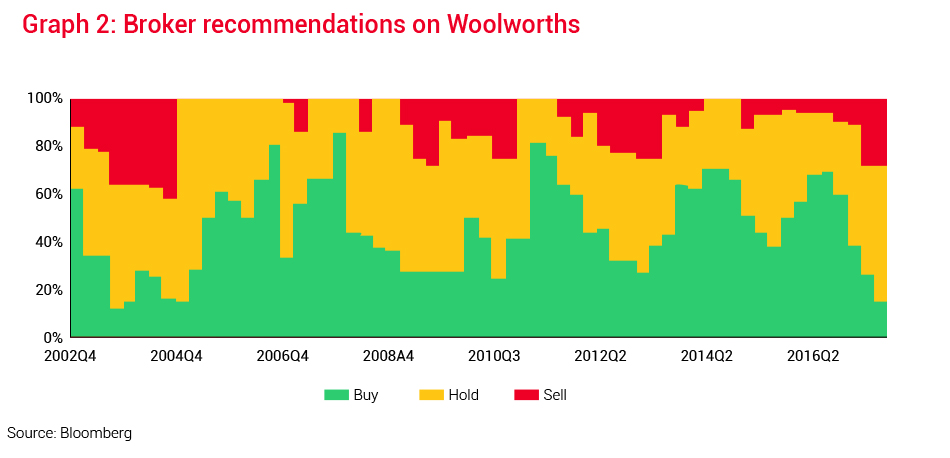

Our contrarian approach can be seen in the comparison of Graph 1 and Graph 2. The latter is a representation of how stock brokers were advising their clients on Woolworths. You will notice that following conventional wisdom is not a route to above-market returns. In 2002-2004, up to 40% of brokers were recommending their clients sell the share, while in 2014-2016, as the share price peaked, the majority of brokers were advising their clients to buy the share. Now that the share price has almost halved from the 2015 peak, only a small minority of brokers are advising their clients to buy.

Today

It takes discipline to wait a decade for a stock to dip under fair value, but our patient approach and long-term philosophy gives us the freedom to do just this. Of course, this neat story is only clear in hindsight and we may prove to be wrong buying the share now. The Woolies business may deteriorate far more than we expect, but at least the odds are in our favour as the share price is not pricing in much hope for the future. Sticking to our investment philosophy – in word and in deed – allows us the opportunity to outperform and create wealth over the long term.