A lot has changed in the tobacco industry in the last decade or so. Despite the changes in what used to be a stable industry, the attractive aspects of tobacco economics still hold, with a cheaper valuation compensating for the increased uncertainty and disruption. Siphesihle Zwane and Varshan Maharaj provide an update on the current landscape and the industry’s prospects.

When we wrote about British American Tobacco (BAT) in our Q2 2010 Quarterly Commentary, the company had recently been listed on the JSE and represented a significant holding in the Allan Gray Equity Fund. Today, we are still investors in the stock, despite the disruption facing the global tobacco industry.

Industry fundamentals

Of the companies we research, the tobacco industry has some of the best structural fundamentals. Tobacco consumption is relatively price-inelastic, which means that price increases can make up for falls in sales volumes. Taxes make up a large portion of sale prices. This creates price leverage, causing consumer prices to rise by less than net revenues received by the business when excise rates do not change. In addition, specific taxes in some countries and efficient distribution make it difficult for new entrants to compete on price, especially since marketing is not allowed in most countries.

Combine all of this with a business that doesn’t need to reinvest a large portion of its earnings, given a simple product and falling volumes, and you get companies that are able to grow while paying out a large portion of their earnings in the form of dividends.

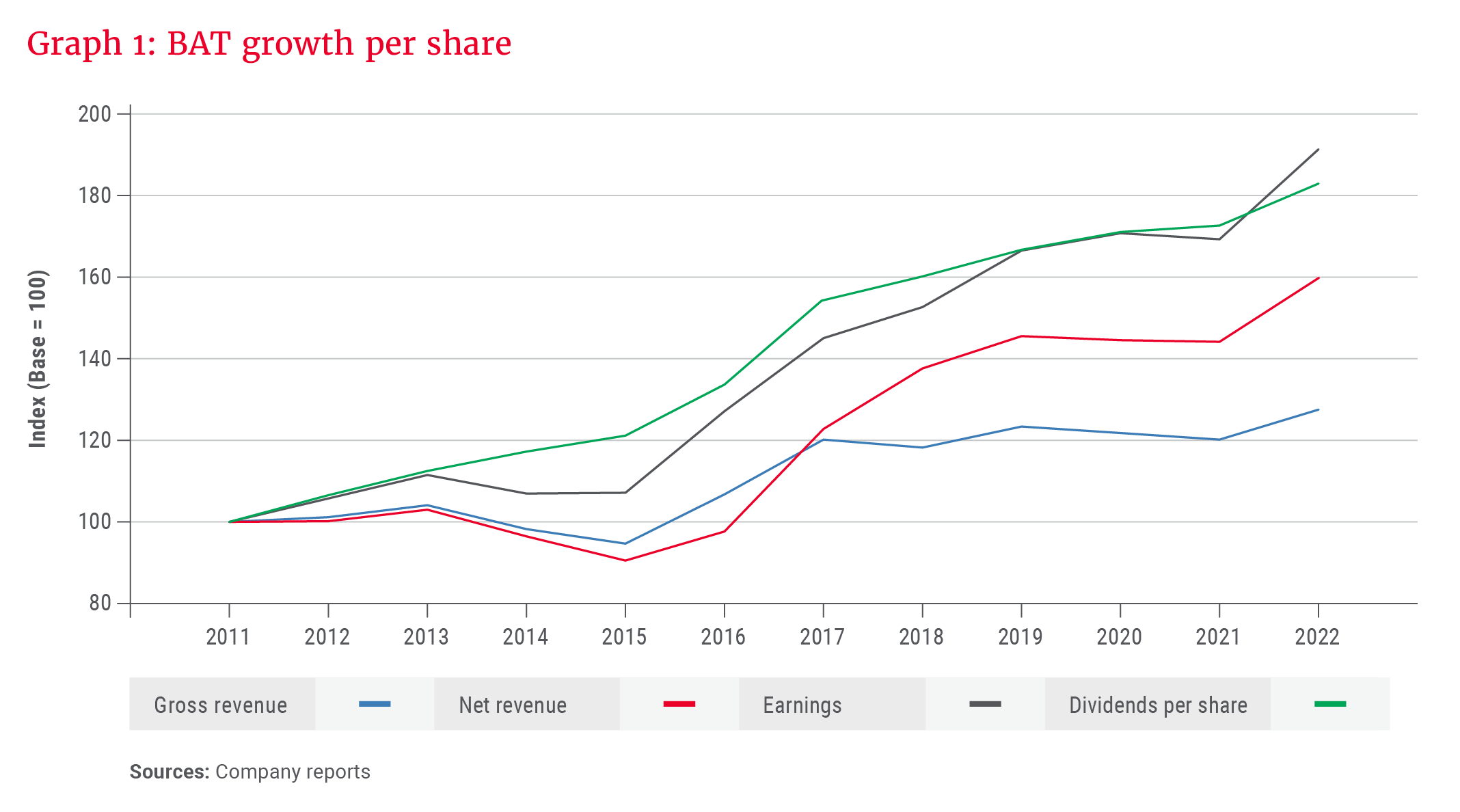

BAT is a good example of how these fundamentals have played out. Earnings have grown faster than net revenues, which have grown faster than gross revenues, with consistent dividends keeping up with earnings growth, as shown in Graph 1. These economics have hardly changed, despite changes in sentiment around the sustainability of profits.

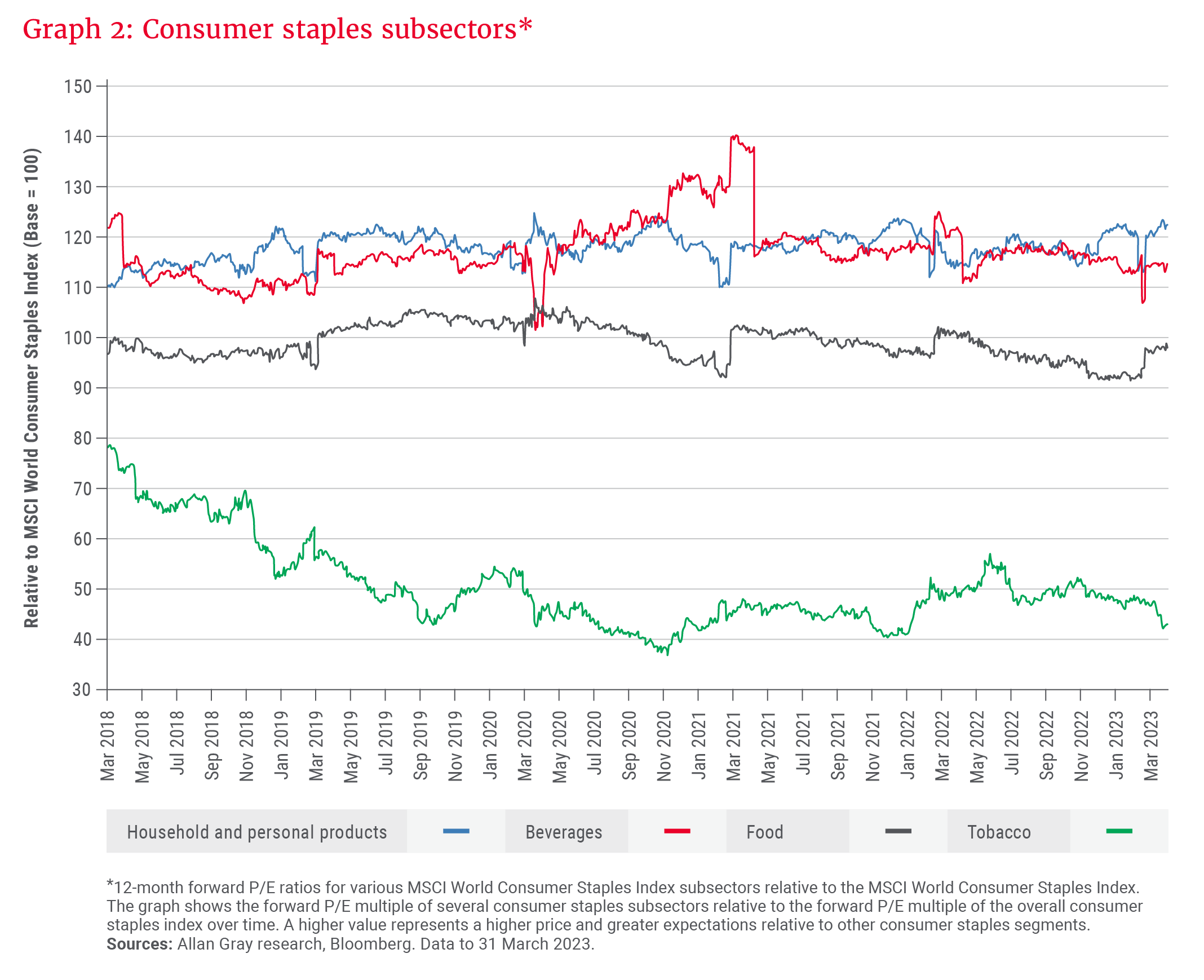

High barriers to entry have historically made it difficult for new entrants to disturb the incumbents, with investors happy to pay up for this. In fact, the tobacco industry used to trade at only a small discount to consumer staples – difficult to believe, given the large discount it trades at now, as shown in Graph 2.

Disruption

To protect attractive cigarette economics, the industry never invested aggressively in new ways to consume nicotine. This changed when JUUL, a vapour brand, began to significantly grow in the United States by introducing innovative products with flavours and marketing that turned their brand name into a verb. This uptick in “JUULing” forced incumbents to increase their investment in next-generation products (NGPs), a major shift from the stable nature of the industry.

Harm from smoking mostly comes from burning tobacco, with non-combustible vapour reducing the risk of exposure for users compared to smoking traditional cigarettes. NGPs are therefore attractive due to their improved long-term business sustainability, despite the shorter-term uncertainty of their economics and market shares.

We invest as business owners, considering the sustainable cash flow that a business can generate over the long term.

While JUUL captured significant market share initially, they did so in an irresponsible manner that helped spark a surge in underaged vaping, subsequently leading to significant litigation. For “Big Tobacco”, a history of litigation has taught them to be more measured and responsible when launching new products and in their marketing efforts. In the case of BAT, they reacted to the disruption by launching three different devices/products, believing that preferences built on differences in regional tobacco products and cultural norms are best served by a menu of products. These are described below.

- Vapour products: These products use vapourised liquid with nicotine salts and, in many instances, different flavours. BAT has the highest market share in the major markets for these products, including the US.

- Tobacco-heating products: These products heat a tobacco stick inserted into the device at a high enough temperature to release nicotine, but not high enough for combustion. BAT is a far second to Philip Morris International (PMI)’s brand in this market, IQOS, which was introduced in 2014.

- Modern oral products: These products come in the form of a teabag-like pouch that is placed between the upper lip and gum, releasing nicotine over time. They are inconspicuous and most popular in Scandinavian countries, where BAT has an incredibly high market share.

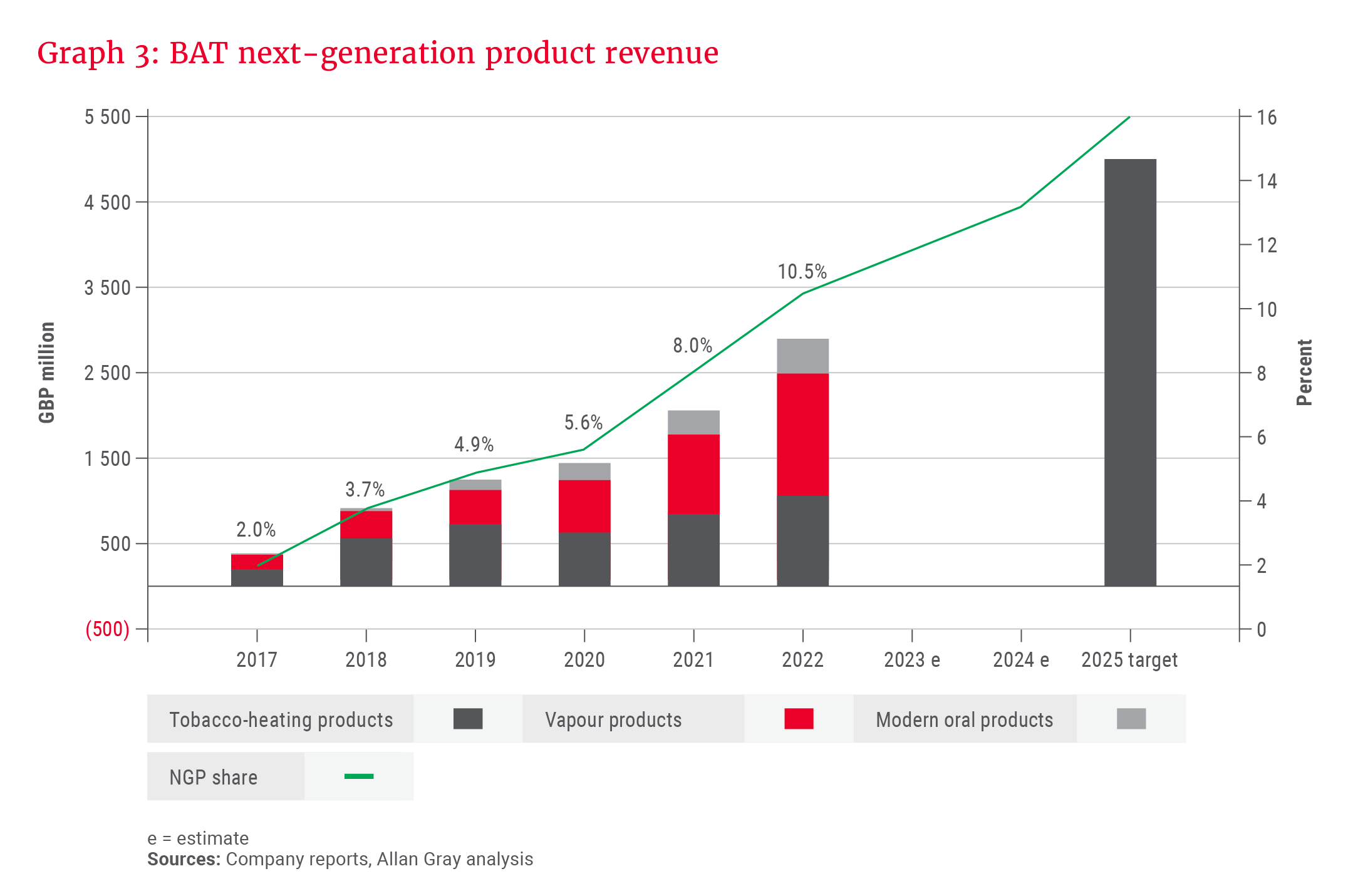

All the options described above looked to pose significantly less harm to the consumer, but with untested economics and often deep investment cycles. BAT’s NGP losses peaked at as high as 4% of total group sales in 2020, or 9% of adjusted operating earnings. This has been improving as the business realises the unit cost benefits of scale, with most recent reported losses reducing by two-thirds to just under 1.5% of group sales.

Most large market regulators have accepted the principle of harm reduction, differentially taxing NGPs versus cigarettes. While this advantage is unlikely to stay forever, it supports the industry while it builds scale to lower unit costs. Even if profitability at market maturity is lower than that of the cigarette market, the reduced harm of these products to consumers and those around them will likely mean more sustainable cash flows over the long term, deserving of a higher valuation multiple.

… we do continue to monitor the science as population studies are conducted to better understand the longer-term impacts.

Big Tobacco is encouraging smokers to quit or, if they are unable to do so, switch to NGPs via various consumer education initiatives, such as stores in malls. These products are all relatively new and the current science regarding harm reduction has been positive, showing as high as a 90%-plus reduced risk of exposure to harmful substances. However, we do continue to monitor the science as population studies are conducted to better understand the longer-term impacts.

Extensive global distribution networks, existing customer bases, and available funds to finance the large investment required to reach scale give incumbents an edge in the NGP market. In addition, as the regulation around these products becomes more closely aligned with that of cigarettes, barriers to entry should start to more closely resemble those of the pre-NGP tobacco landscape.

The competitive landscape

BAT is currently targeting GBP5bn NGP revenue by 2025, as shown in Graph 3, and break-even by 2024, with 50 million NGP consumers by 2030. Further out, they expect at least 50% of group revenues to come from NGPs by 2050. This won’t be easy, as the overall industry also sees the benefits of these new products:

- PMI’s focus is on tobacco-heating products, which form the largest and fastest-growing NGP category, offering the best economics. BAT, Japan Tobacco International and Imperial Brands moved more slowly and are trying to catch up in this space.

- Japan Tobacco International is accelerating its Ploom X brand and aiming to reach NGP break-even by 2028.

- Altria recently announced the acquisition of NJOY in the US, after continued issues with JUUL. The device will be integrated into their strong distribution channels in the country.

- Imperial Brands is the laggard, having pulled back initial investment.

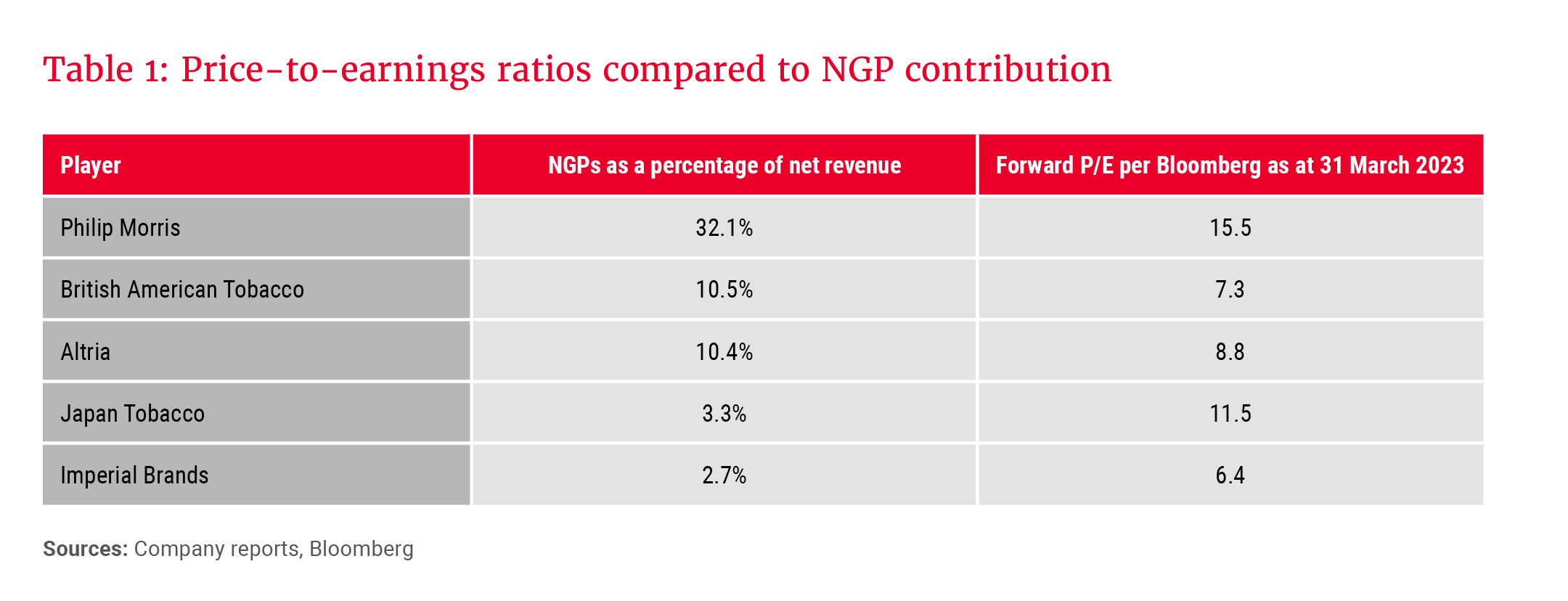

Players with a larger share of their revenues coming from NGPs have better revenue growth and margin prospects, and the market is rewarding them with higher earnings multiples, as shown in Table 1. The value to trade buyers is also reflected in PMI’s recent acquisition of Swedish Match, which was done on a multiple of 28 times trailing earnings. Swedish Match derived 69% of its net revenue from NGPs at the time of the acquisition.

PMI’s progress is an indication of the upside potential if BAT can successfully execute its NGP strategy. Once smokers fully convert to PMI’s IQOS product, very few go back, as it closely matches the taste, experience, nicotine delivery and rituals of cigarettes at a lower cost and risk to the user. PMI’s NGP results are improving as they have already spent heavily on advertising, leading to declining acquisition costs and rising retention. While BAT is still at a loss-making investment stage, PMI’s IQOS already seems to be twice as profitable as cigarettes on a unit basis due to similar manufacturing costs and lower taxation rates.

Some of the risks associated with tobacco investments

The sector does, however, come with some significant risks, the largest of which are regulatory. These risks have not had a large noticeable impact on earnings yet, but have caused the sector to trade on a lower multiple of earnings. Outsized excise-driven price increases could lead to a large-scale shift to illicit trade, which currently makes up 9% of total volumes and costs governments around US$40bn per year in taxes. Big Tobacco is an efficient tax collection and regulation enforcement machine, which is preferable to the industry being controlled by illicit players.

Our research-intensive approach, combined with a longer-term outlook, allows us to buy great businesses at low valuations, especially in times of heightened risk and disruption.

BAT has a high debt burden at 2.9 times EBITDA (earnings before interest, taxes, depreciation and amortisation). This is, however, well protected against the short-term impact of higher interest rates. BAT’s average cost of debt is 4%, 97% is fixed rate and the average maturity is 9.9 years. The business has paused share buybacks to allocate funds to debt repayment as the outlook for longer-term rates has increased. One of the elements driving higher rates, namely inflation, also benefits the revenue line, given strong pricing power, with the associated interest rate cost coming over a longer time, given the above-mentioned protection.

The risk of declining volumes is always top of mind. Smoking prevalence is declining, and the population is growing. The net effect is that the number of smokers has remained between 1 billion and 1.1 billion since 1990. BAT is likely to grow revenue and margins, assuming that long-term combustible volumes do not fall rapidly, low single-digit real price increases per year are achieved and profit-per-stick improves as the mix changes in favour of NGPs.

Integrating environmental, social and governance (ESG) factors into our research is intrinsic to our investment philosophy. There are several nuances and complexities, and emerging news headlines and trends have to be examined in the context of each company, and the sector and country within which it operates. A rational approach is key. A good example is the fine that BAT will have to pay to the US over North Korea sanction violations – an issue that has just hit the news, but has in fact been under investigation since 2019. BAT has conveyed tangible steps to deal with this and other governance-related matters, but we continue to monitor the situation closely. For in-depth details of our approach, see our Stewardship and Business Sustainability Reports.

A long-term opportunity for patient investors

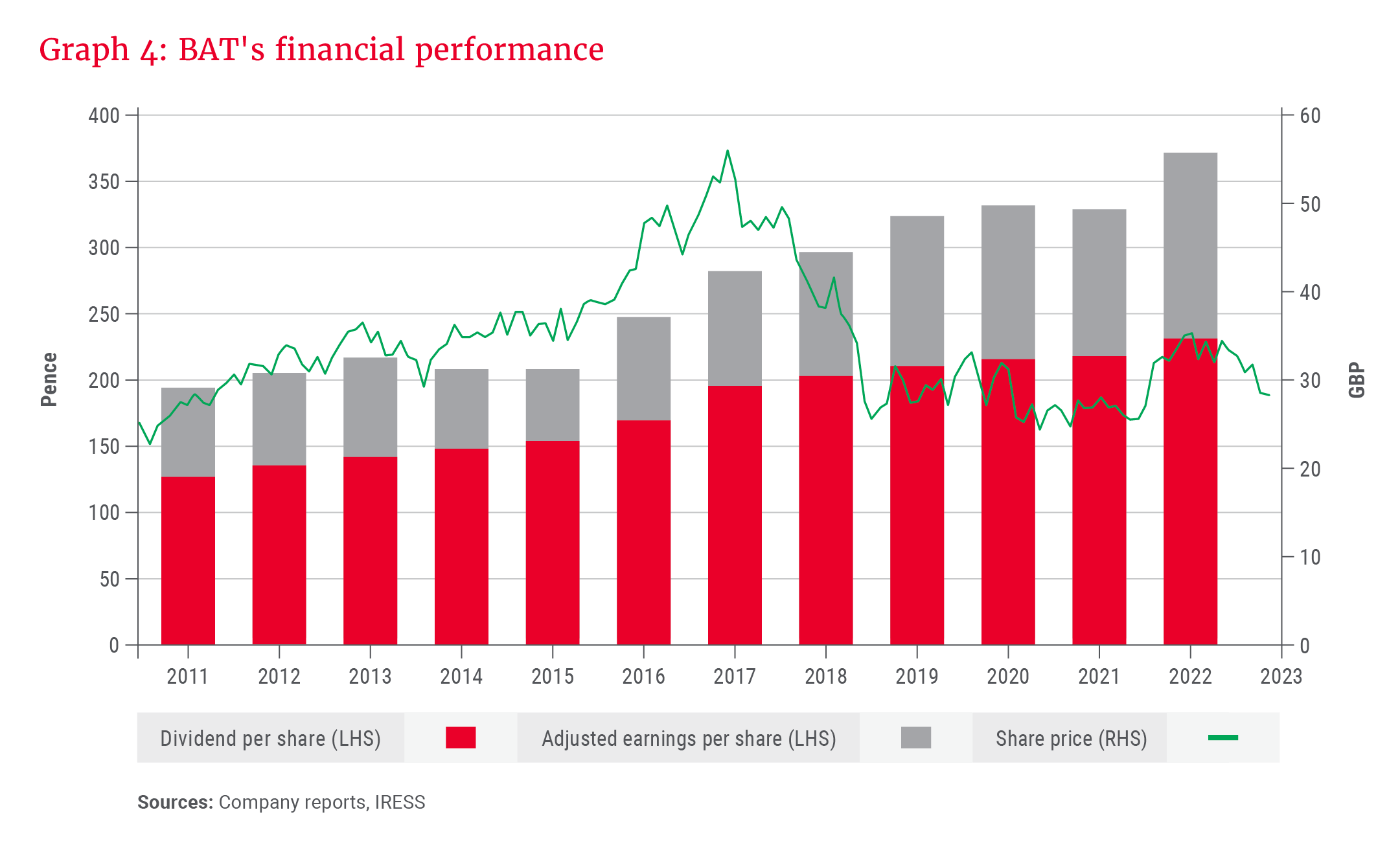

Our research-intensive approach, combined with a longer-term outlook, allows us to buy great businesses at low valuations, especially in times of heightened risk and disruption. A look at BAT’s financials reveals little impact from this disruption, given the company’s measured approach to handling it – see Graph 4.

BAT has managed to invest in NGPs with limited impact on the cadence of reported results, likely improving the longevity of its business in the process. We invest as business owners, considering the sustainable cash flow that a business can generate over the long term. BAT’s share price has not reflected the fundamental results of the business in recent years, but at a growing 7% GBP dividend yield, shareholders should be well rewarded for their patience.