The discount between Naspers’ share price and the value of its underlying assets has widened further and now looks quite extreme. Being a large holding in both the Allan Gray and Orbis portfolios, Ruan Stander from Allan Gray and Stefan Magnusson from Orbis examine this interesting and critical dynamic.

Founded in 1915 in South Africa to publish newspapers, Naspers is one of the largest technology investors in the world today. It derives essentially all of its intrinsic value from a collection of internet assets outside South Africa comprising not just its investment in Tencent, but also those in online classifieds, food delivery and online payments businesses.

The company has delivered exceptional returns for long-term shareholders. We estimate that a Naspers shareholder in 1980 earned 21% per year in real US dollar terms to today. This may not sound particularly impressive given the recent strong performance of many technology stocks, but to put it into context, only one US-listed share returned more than 20% per annum in real terms over the same period. The corresponding return for the US stock market has been 9.1% per annum and, interestingly, the 100 most profitable US-listed companies in 1980 that remain listed today, delivered a return of just 5.5% per annum. Compounding at that rate for just over 40 years would have turned US$1 into US$9 compared with US$2 350 from an equivalent investment in Naspers. This last comparison is particularly striking and illustrates that many companies struggle to adapt and thrive as they grow and age.

So how has Naspers been able to buck the trend?

At first glance, it’s hard to see what its past successes in businesses such as newspapers, magazines, pay TV, and online classifieds have in common. On closer inspection, their economic characteristics are remarkably similar: The cost and quality of these products and services improve significantly as they add more customers. As a result, these businesses tend to lose money for several years before becoming unusually, and sustainably, profitable for the providers that serve the most customers. Notably, Naspers’ newer businesses have disrupted its older ones, reflecting a culture that is willing to adapt. However, a willingness to adapt does not guarantee success. Naspers has therefore chosen to partner with entrepreneurs who have a record of strong execution.

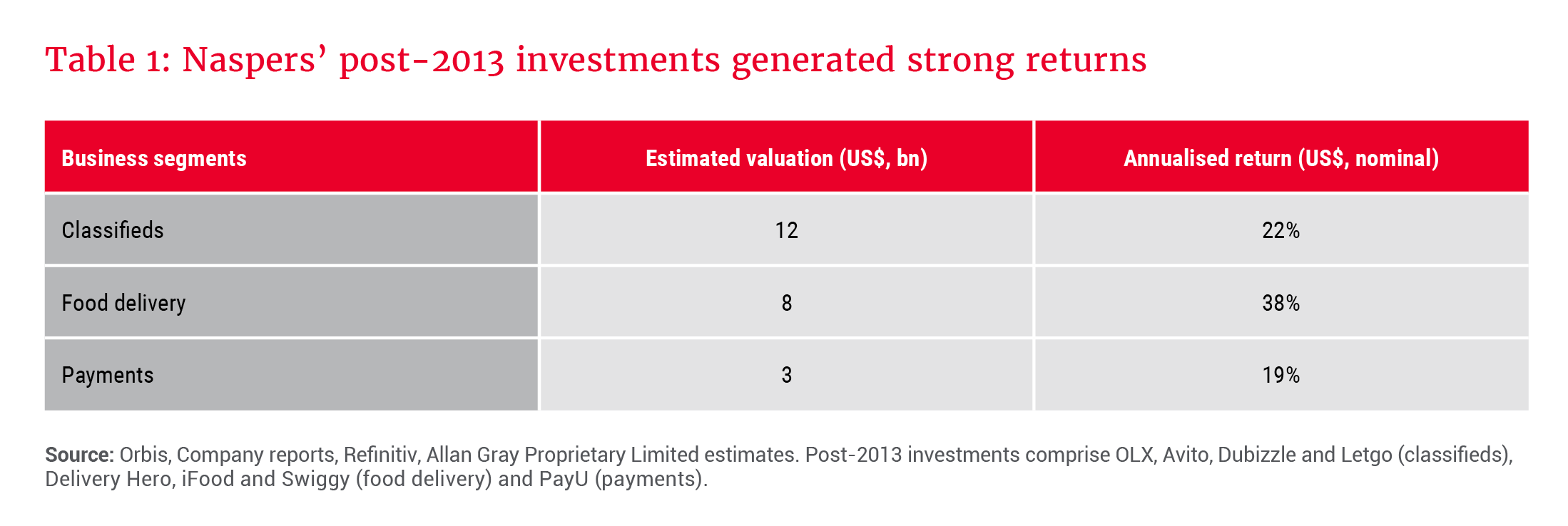

A similar question can be asked – and is being asked by investors today – of Naspers’ own management team. Does it have the same acumen as previous generations? We think the answer is a resounding yes, based on our view that seven of its eight most recent significant buy and sell decisions were good ones. Overall, and as shown in Table 1, we estimate that management’s decisions since 2013 to invest in the classifieds, food delivery and payments segments have each returned around 20-40% per annum.

Delivery Hero, a listed company that represents the majority of Naspers’ food delivery portfolio, serves as a good proxy for its investments in this segment. Since its listing in 2017, its share price has grown at around 50% per annum, as the company’s fundamentals have grown organically at a similar rate.

Naspers has … chosen to partner with entrepreneurs who have a record of strong execution

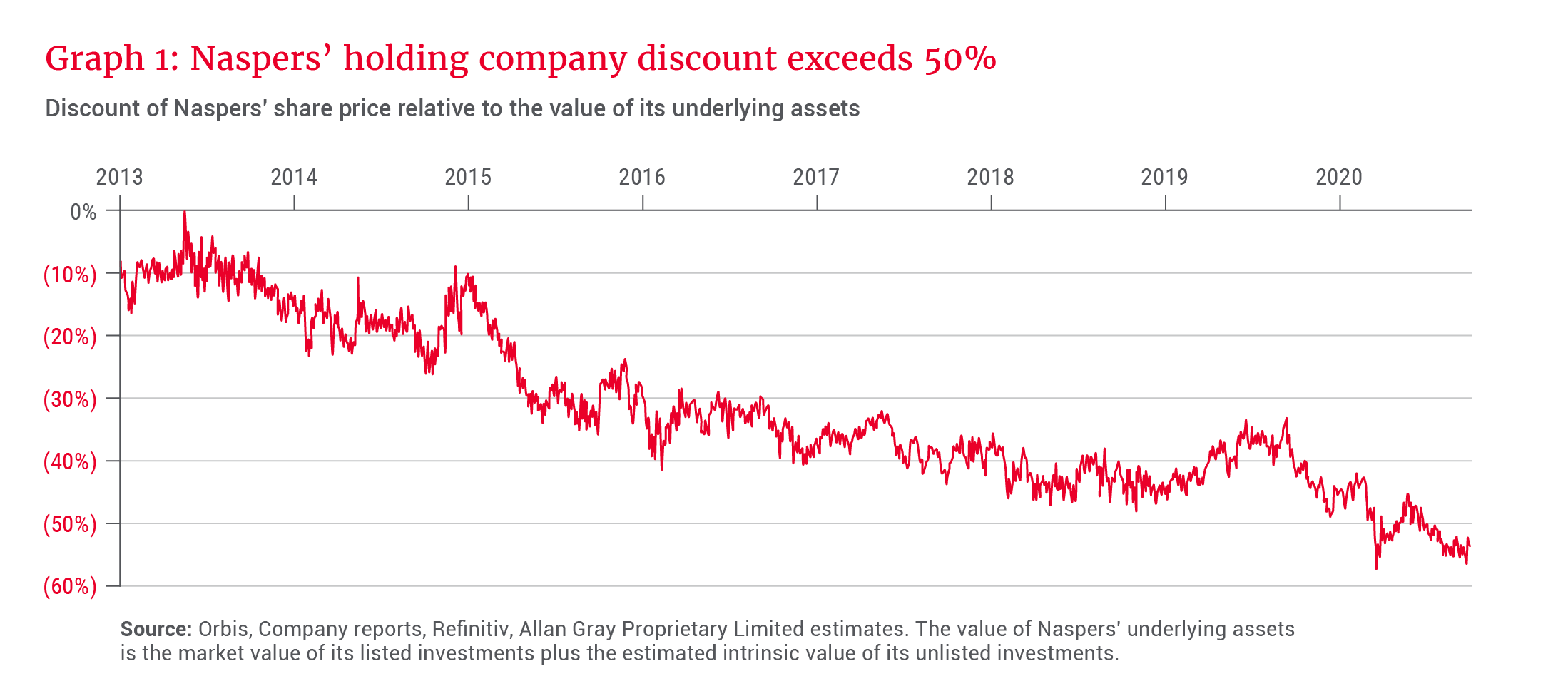

The market’s positive view of Naspers’ investments like Delivery Hero has not been reflected in its own share price. Instead, shares in Naspers have traded at an ever-widening discount to its underlying assets, as shown in Graph 1.

Why this apparent disconnect? One explanation is that South African investors are more sceptical of new ventures that are currently loss-making – similar to magazines, pay TV and classifieds in their early years. Another is that, as Naspers increases in size as a proportion of the South African stock market, investment mandate limits force local institutional shareholders to reduce their holdings. Alternatively, many investors may simply prefer direct access to the underlying portfolio of investments. While we recognise that each of these factors is unlikely to change any time soon, we do not see why the current discount should persist over the longer term.

Naspers’ leaders are acutely aware of the holding company discount and, as substantial shareholders in the company, have a strong incentive to reduce it. Last year, Naspers separately listed all of its internet assets outside of South Africa – via a new entity, Prosus, that has a primary listing on Euronext Amsterdam. Management recently commented that it is exploring a number of other ideas to unlock value for shareholders.

Regardless of one’s views of these plans, if Naspers continues to invest wisely, it should attract investors who recognise the scarcity value of such a good long-term investment record.

Balancing risk and return

Both Naspers and Prosus have two share classes, giving voting power to a small number of shareholders. This governance concern has not destroyed value for ordinary shareholders in the past, but could inhibit their ability to effect change if future management teams are less competent.

Another risk is that its existing investments generate poor returns from here, either due to deteriorating fundamentals or lofty starting valuations, but our bottom-up work leads us to conclude that they remain reasonably valued in aggregate.

the recent widening of the holding company discount has made the investment case for Naspers more attractive

Recent events also show how Chinese technology firms, including Tencent, face geopolitical risks that are hard to handicap. Still, with the combination of Naspers’ assets outside Tencent and its proportionate share of Tencent’s own investment portfolio (where stakes in listed companies make up the majority of the value) representing nearly 80% of its current market price, the implied value of Tencent’s operations is just six times its free cash flow.

In our view, the recent widening of the holding company discount has made the investment case for Naspers more attractive from a risk and return perspective. While it is realistic to expect some discount, if it were to narrow from 53% to 25% in the next four years, shares in Naspers would outperform its underlying investments by more than 12% per annum in that time.

We continue to hold a large position in Naspers, despite its significant outperformance of the South African stock market, but will continually adjust the position size as our assessment of the risk and return takes into account new evidence and changes in the valuation.