Employee benefits consultants play a critical role in shaping outcomes for retirement fund members. Siyasanga Mlozana explores how they influence contribution structure and design and guide the selection of appropriate investment defaults, as well as the everyday, non‑financial decisions members make throughout their working lives.

Making adequate contributions towards retirement remains the foundation of achieving successful retirement outcomes. But beyond how much members invest, research and experience show that the decisions they make over time – how early they start, how long they work, whether they preserve their investments and how they respond to financial pressure – can significantly enhance or materially destroy the impact of their contributions.

There are several non‑financial actions that improve long‑term retirement outcomes.

Employer fund design

Before considering behavioral or structural factors, it is important to restate a fundamental principle: Investing enough matters. Members need to make adequate contributions. To ensure adequate contributions, fund design is key. Employers and consultants need to consider default contribution and escalation rates, review contributions as members progress in their careers and allow for additional voluntary contributions through payroll, where possible.

Selecting an appropriate default strategy

Regulation 37 of the Pension Funds Act requires umbrella fund trustees to offer default investment portfolios designed to meet the needs of the majority of members. Consultants support the selection process by:

- Conducting due diligence on default investment strategies

- Advising employers on suitability, risk management and cost

- Ensuring governance structures remain robust and compliant

Once a suitable default investment strategy is in place, members benefit most by contributing consistently, at appropriate levels, to benefit fully from tax efficiency and compound growth over the long term. Frequent switching or reactive decision‑making can undermine outcomes rather than improve them.

The everyday decisions that shape long‑term outcomes

Once the foundation is in place, it is often non‑financial choices and actions that determine long-term outcomes.

1. Starting early

One of the strongest drivers of positive retirement outcomes is time in the market. Starting early initiates good investment habits and allows contributions to benefit from decades of compounding.

- Outcomes improve when retirement investments begin automatically from the start of employment

- Communication during onboarding encourages member engagement and helps members understand the long‑term value of early and ongoing contributions

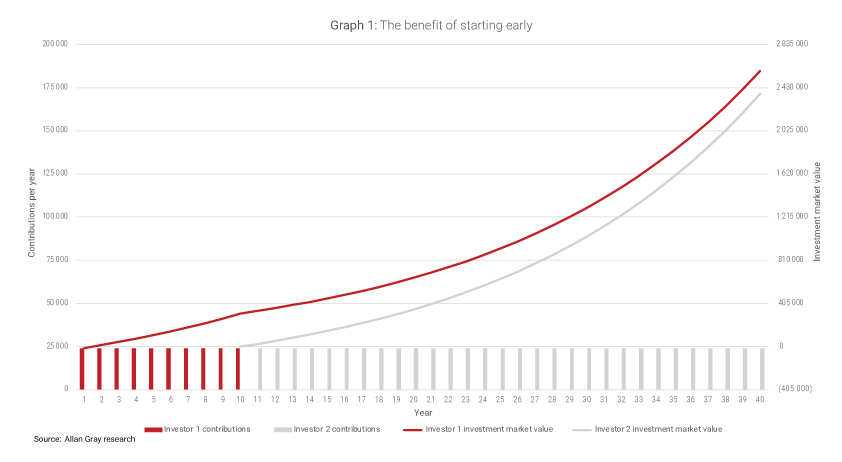

Graph 1 below paints a comparative scenario of two investors: Investor 1 starts investing for retirement when they start working; Investor 2 starts to invest a decade later. Investor 1 invests R24 000 every year (R2 000 per month) for 10 years, then stops. Investor 2 starts investing the same amount in the year that Investor 1 stops, continuing for 30 years. In both scenarios, the growth rate is 7.3%, with contributions escalating with 5% inflation.

The picture that emerges is that Investor 1 ends up in a better position (with 10% more at retirement) – even though they would have only contributed R240 000 in nominal terms versus Investor 2’s R720 000. This shows that starting early and staying invested significantly improves retirement outcomes.

2. Working for longer

According to Statistics South Africa, the life expectancy of South African men increased from 61.7 years in 2022 to 64.0 years in 2025, while for women it has increased by 2.2 years from 67.4 to 69.6 years in the same period. This means that retirement investments need to last longer than previously anticipated.

Working longer and deferring retirement, where circumstances allow, presents several benefits:

- Contributions continue for longer, resulting in more money being invested

- Contributions from earlier remain invested for additional years, benefiting from compound growth

- When members put off withdrawing an income, they allow more time for the first two benefits above to take effect, ensuring reliance on retirement income for fewer years

That said, any extension depends on a member’s employment contract, role requirements and operational considerations. Consultants can facilitate informed, constructive discussions between employers and employees, helping to ensure that expectations are aligned and fund rules are applied consistently.

3. Resisting early access

Since September 2024, the introduction of the two-pot retirement system has allowed members limited access to the savings component of their retirement fund before retirement. This access is intended to support members facing genuine financial distress. However, early withdrawals come at a cost: They reduce retirement capital and are difficult to replace. Once accessed, savings lose the benefit of future compounding.

Consultants play a critical role in helping members understand that early access should be a last resort and that retirement investments are fundamentally long‑term in nature. By encouraging members to explore alternative funding options first, consultants can help preserve capital and protect long‑term outcomes when short-term pressure arises.

4. Preserving investment when changing jobs

Changing jobs is one of the highest‑risk moments for retirement outcomes. Historically, it has been a key point at which a significant amount has leaked from the retirement system. Default preservation rules and the two‑pot framework aim to reduce this leakage. Umbrella fund members are typically defaulted into paid‑up membership when they leave employment, allowing their retirement contributions to remain invested and benefit from institutional pricing. Consultants can reinforce the value of preservation by helping members understand the tax implications and long-term impact of cashing out available funds* when changing jobs, compared to staying invested over time.

Small decisions, lasting consequences

Contribution levels set the foundation for retirement planning, but the above non‑financial actions can determine whether members ultimately retire well. Employee benefits consultants are uniquely positioned to influence these decisions. By guiding both employers and members through the moments that matter most, they help turn sound retirement design into stronger outcomes over the long term.