Over the past year, we have seen local investments streaming towards bonds and cash – the top-performing asset classes for most of 2019. Are investors chasing performance, or can they expect to get real returns from perceived safer investments over the long term? Beatri Faul investigates.

Recency bias is the tendency to overvalue the most recent information available to us. It can impact our decision-making and cloud our judgement. This common behavioural bias crops up in various aspects of our lives and can have negative consequences. Disregarding long-term trends can be detrimental, particularly when it comes to investing.

A difficult time for local equities

Investing in today’s environment is difficult. We are forced to make decisions in the face of uncertainty, including political unrest, slow economic growth, threats of downgrades and massive fiscal debt. Meanwhile, equities, which are expected to give the best real returns over the long term, have disappointed, with the FTSE/JSE All Share Index (ALSI) delivering real returns of 1.1% annualised over the past five years (to end December 2019).

In contrast, cash and bonds have delivered strong real returns of over 2.3% annualised over the same period. Globally, the level of uncertainty isn’t much better, with Brexit, trade wars, slowing economic growth and sustained quantitative easing skewing the natural flow of capital in these economies.

Now more than ever, given all the uncertainty, keeping a long-term mindset is key

All this negative sentiment and uncertainty has driven investors to shun the local equity market. Is this warranted – or is it a perfect case of recency bias?

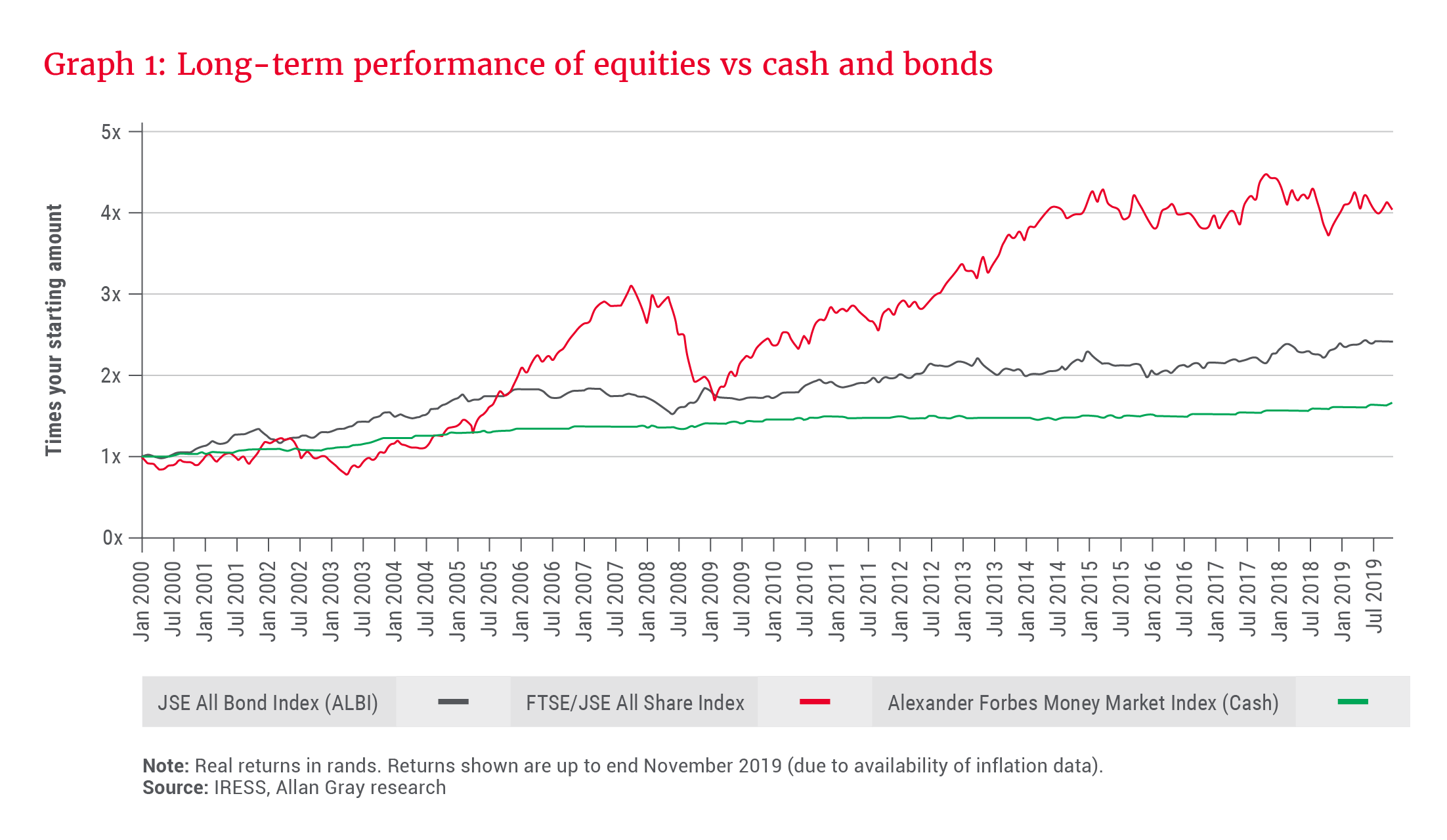

Graph 1 shows the extent to which equities have outperformed cash and bonds in real terms over 20 years. If you started to invest in January 2000 and invested in cash, you would have 1.6x your money today; if you invested in bonds, 2.4x your money, and if you invested in equities, 4x your money. Having said that, the ride to achieving returns through equities has not been comfortable, as reflected by the bumpiness of the red line.

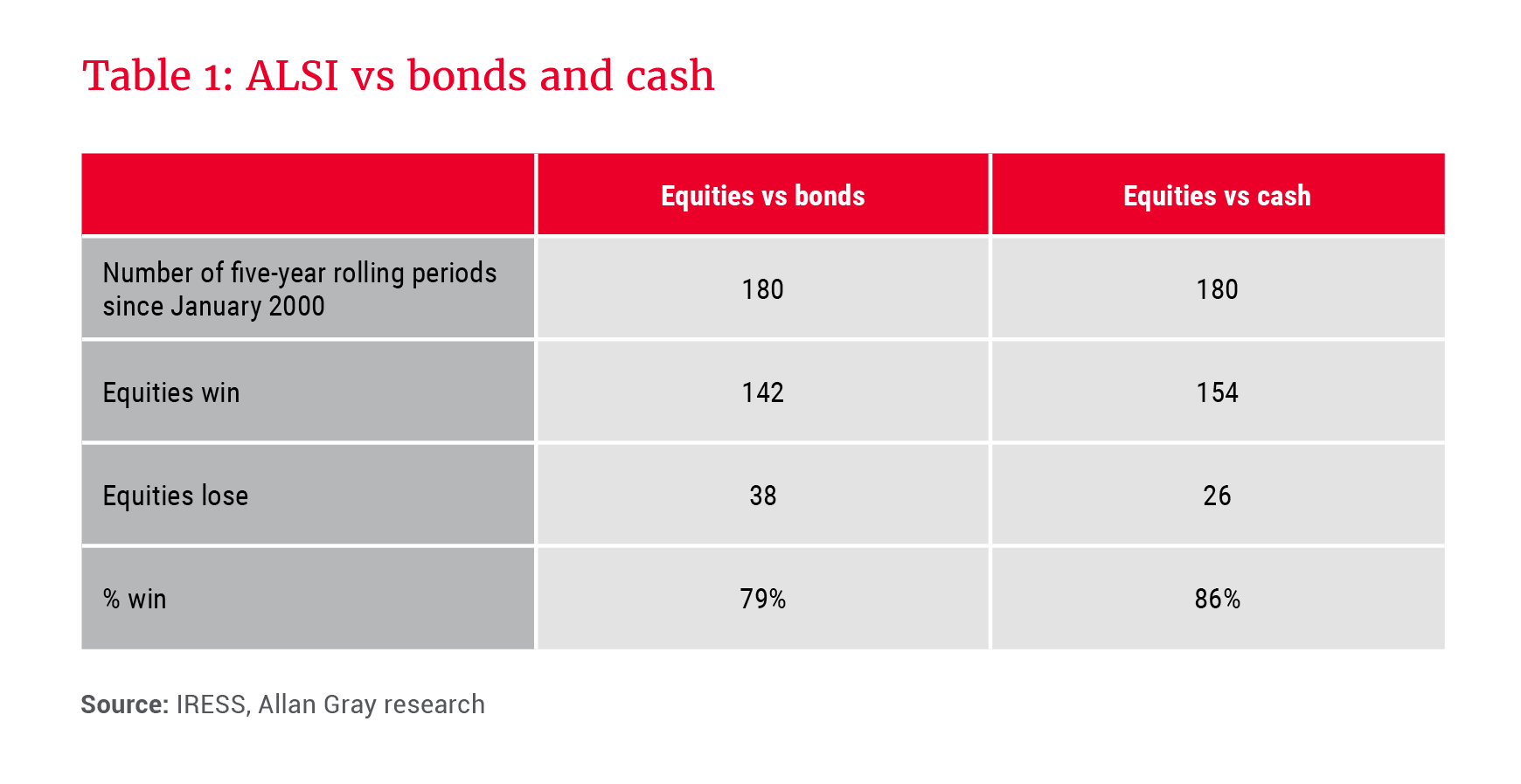

Put differently, of the 180 monthly rolling five-year periods since January 2000, the ALSI managed to beat bonds 79% of the time, and cash 86% of the time – an overwhelmingly positive result, as shown in Table 1. But bear in mind that 21% and 14% of the time respectively, equities underperformed bonds and cash over a five-year period. And in those times, much like today, it may have felt like a mistake to hold equities in your portfolio.

Are South African equities a poor choice?

Many clients today are struggling to reconcile the dim economic outlook for the country with positive returns on local equities in the future. How can a company that operates in such a difficult environment do well? Why should you take the risk?

Firstly, a strong, growing economy does not necessarily mean that you are guaranteed strong performance from all companies on the stock market. This is because a strong economy likely introduces competition, which brings down the prices these companies can charge, and subsequently profits. In a slower growing economy there is less competition, and while there is also less money to spend, goods and services are still needed, therefore there is still opportunity for some companies to thrive.

Secondly, price and value are the most important determinants when it comes to investment returns. Because the South African stock market has been driven down by negative sentiment over the past few years, you are able to pay reasonable prices for attractive opportunities today. This increases your chances of achieving good performance in the future.

Of course, not all stocks are created equal, and some may be trading at low valuations for good reason. But it is our job to do the hard research and pick those shares that we find to trade below their intrinsic value.

Lastly, equities offer diversification benefits, because around 60% of the earnings on the JSE are generated offshore. Equities are therefore more likely to protect the value of your investments in extremely negative South African scenarios.

It’s not to say bonds and cash should be entirely avoided: They are an important part of a well-diversified portfolio, as Londa Nxumalo discusses. However, changing your strategy out of fear and switching to cash and bonds completely may not be the best long-term strategy. This is because these asset classes are not entirely without risk, especially given the current climate and impact of potential rating downgrades.

long-term past performance reflects that equities give you the best outcome

What risks are you exposed to through cash and bonds?

One common mistake investors make is not considering the real value and/or purchasing power of their capital. Local cash and bonds offer no exchange rate diversification, so if the rand depreciates, in most cases, so does your relative wealth.

Another risk to the real value of your capital is inflation. When buying a vanilla bond, you commit to receiving a certain yield. If inflation increases sharply, this yield may not be enough to keep up and could leave you with negative real returns. Similarly, the return on cash is determined by the prevailing interest rates, which may not keep up with inflation.

Some other more obvious risks include the devaluation of your investment. Increased interest rates would be good for your cash investments, but bad for your bonds. An increase in interest rates will cause the price of your bond to fall. At this point, you won’t be able to sell the bond for as much as you bought it for, and you may experience a capital loss.

today, we are more excited about the opportunities on the stock market than five years ago

Are investors currently following the herd?

The best way to protect your capital is to construct a well-diversified portfolio that can earn real returns regardless of market conditions. But looking at money movements in the investment industry (flows), it seems that investors are making decisions based on recent performance.

In 2018 and 2019, income funds took a bigger portion of investors’ money than they have over the past 20 years, attracting 37% and 137% of total industry flows respectively. Graph 2 shows what percentage of flows went into various unit trust categories, as classified by the Association for Savings and Investment South Africa (ASISA), from 2000 to 2019. Flows to the Multi-Asset Income (red) category in 2019 were at the expense of the Multi-Asset High Equity (green) and Multi-Asset Low Equity (blue) categories.

Generally, the latter two categories enjoy a bigger portion of flows as they provide investors with a good balance between growth asset exposure (like equities) and more stable asset exposure (like cash and bonds). However, the disappointing real return on equities over the past five years has led investors to increasingly shy away from equity exposure in their portfolios, opting for bonds and cash instead.

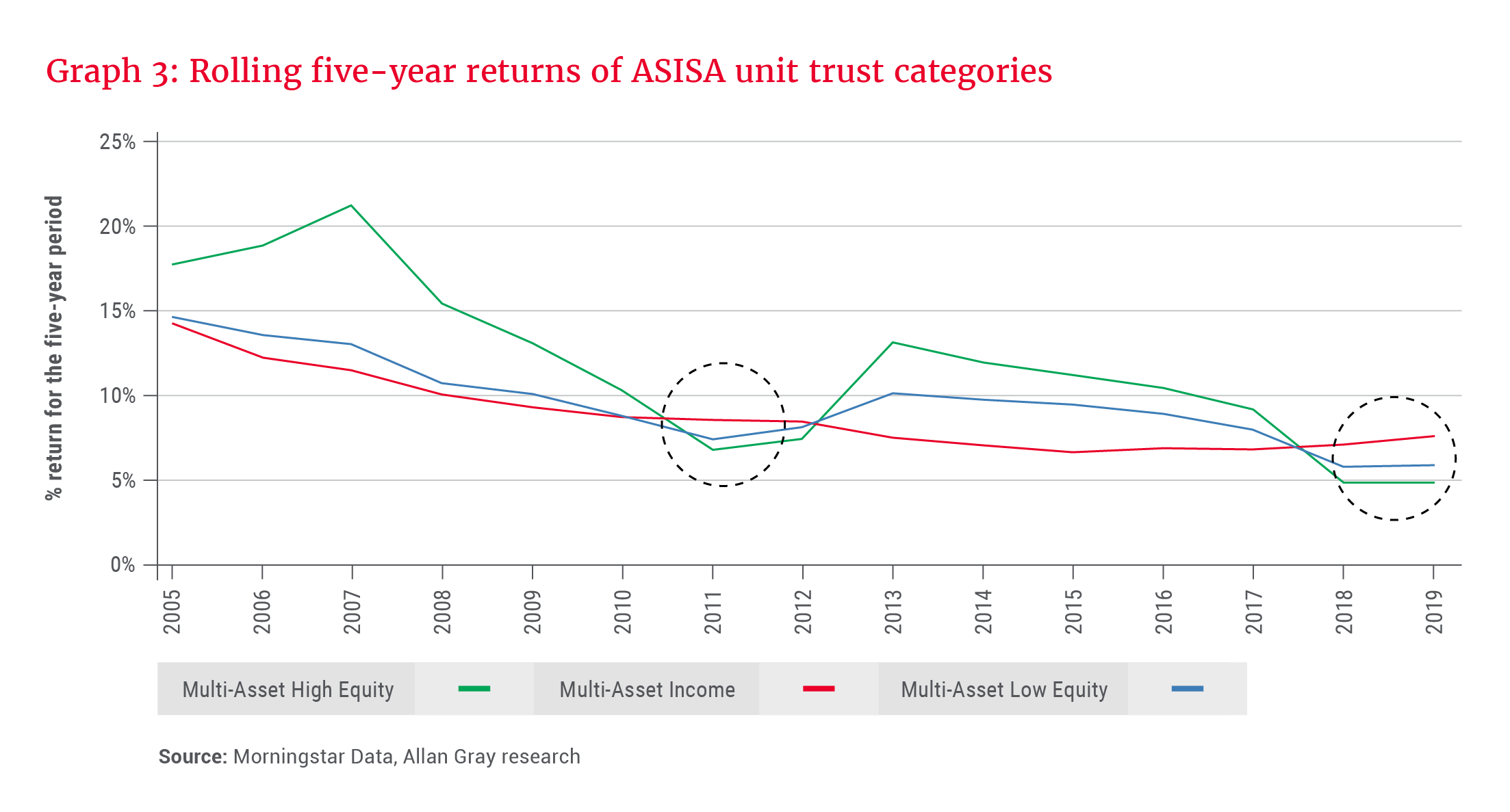

Looking at Graph 3, apart from 2018 and 2019, the other time that the Income category had a higher five-year rolling return than High-Equity and Low-Equity was in 2011 and 2012. That coincides with the third highest relative share of flows to the category over the entire period. This trend is similar today.

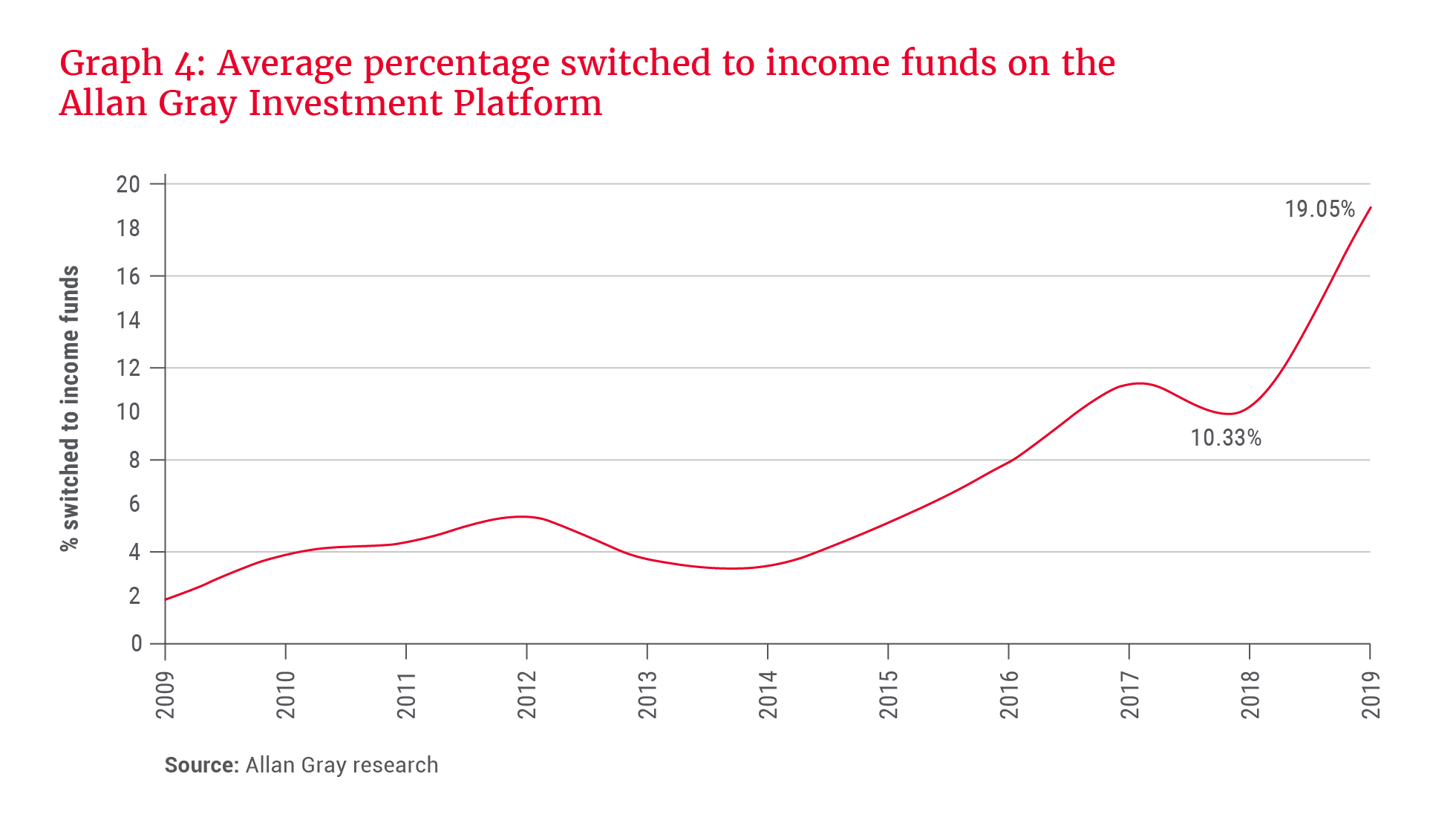

We have seen the same behaviour on the Allan Gray Investment Platform. The average percentage of gross inflows into the Multi-Asset Income category has increased almost four times over the past five years, while it has decreased for the Multi-Asset High and Low Equity categories. Furthermore, the average percentage switched to income funds almost doubled from 2018 to 2019, as shown in Graph 4. As a result, many clients on our platform have a bigger exposure to cash and bonds today than in previous years.

Adopt a long-term mindset

Many investors seem to be basing their decisions on the recent performance of cash and bonds, ignoring the longer-term data, which tells a different story.

Switching to cash and bonds may seem like a good idea now. However, long-term past performance reflects that equities give you the best outcome and, depending on your personal objectives and time frames, are an important part of your portfolio. Furthermore, by the time you have the courage to get back into the equity market, prices may have moved upwards, reducing future returns.

Remember, the most important determinant of future returns is the price you pay for an asset today. And today, we are more excited about the opportunities on the stock market than five years ago. Now more than ever, given all the uncertainty, keeping a long-term mindset is key.