Commentary as at 31 March 2026.

As markets grapple with volatility, uncertainty and rapid technological advancements, Stanley Lu from our offshore partner, Orbis, emphasises the importance of owning high-quality businesses grounded in discipline, trust and reliability. He explains how Taiwan Semiconductor Manufacturing Company, one of the Orbis SICAV Emerging Markets Equity Fund’s highest-conviction holdings, embodies Orbis’ long-term investment philosophy.

The future is inherently unpredictable and bouts of volatility are par for the course for investors. In the long run, however, we are firmly of the belief that the principal determinants of equity returns are the quality of the underlying businesses, the skill of the management teams that steer them and the price paid. Rather than predicting how events in the short run will play out, we instead stay focused on the long-term fundamentals of the businesses we choose for your portfolio.

In doing so, our aim is to invest in companies with durable business models that are conservatively run by aligned management teams, and with a proven history of navigating through uncertainties. We do so precisely because we know that periods of short-term volatility can, and will, occur.

In particular, we often look for companies that share similar core values to our own. At the top of that list is “Earn the trust and confidence of our clients”. Taiwan Semiconductor Manufacturing Company (TSMC), one of our largest holdings, is a prime example.

TSMC is the world’s largest dedicated semiconductor foundry, manufacturing semiconductor chips that power an ever-expanding range of compute devices and providing technology support for over 500 customers. As one of the only companies capable of commercially producing leading-edge semiconductors, TSMC has a dominant market share of approximately 70%. That position is the result of choices made decades ago, and the company’s substantial moat has only widened since.

Many are familiar with Morris Chang’s legendary founding of TSMC in 1987, following a distinguished 25-year career at Texas Instruments. As one of the semiconductor industry trailblazers, Chang pioneered the pure-play foundry model – manufacturing chips designed by others rather than competing with them. What is less widely appreciated, however, is Chang’s enduring influence on the company’s culture. From the outset, Chang embedded a clear and demanding philosophy: to be superior to competitors in satisfying customers’ needs in every aspect, with the singular exception of low prices. This was not merely aspirational; it was explicitly articulated in TSMC’s corporate strategy in the early days and has remained central to how the company operates.

Peter Drucker, the inventor of modern business management, astutely observed: “The purpose of business is to create and keep a customer”. The foundry model created the customers, and TSMC’s culture keeps them. That culture is perhaps best appreciated by those who have lived it. From the largest fabless companies down to the smallest startups, TSMC’s magic is to treat them as if they were the most important partner in the room. On time. With full support. No deflection, no runaround – problems are owned at every level of the organisation. The tools and equipment that TSMC uses are, in principle, available to others. Yet such customer-centric obsession is something that cannot be easily copied. Any competitor serious about displacing TSMC would have to start not with a better fab, but with a better culture. That, more than any process node or piece of technology, is Morris Chang’s most enduring legacy.

Over time, this customer-centric culture has created trust of an unusually durable kind. Chip designers build their entire product roadmaps around a manufacturing partner whose reliability and timeliness determine whether those designs ever reach the market. Typical roadmaps for leading-edge chips begin at least four years before high volume production and designing such products can cost over US$500 million. With such long cycles and high upfront costs, switching partners is both costly and risky – greatly increasing the value of a relationship built on reliability and trust. TSMC’s refusal to compete with its own customers, combined with an architecture designed to safeguard their intellectual property, has made it the partner of choice across the industry. Nvidia CEO Jensen Huang has acknowledged that Nvidia’s success would not be possible without TSMC.

TSMC’s trusted partnership has also placed it at the forefront of many of the major technological advancements of the past four decades. From the PC era in the 1990s, the birth of the smartphone in the late 2000s, to most recently, the artificial intelligence (AI) megatrend, TSMC’s technology has been behind them all. While the world scrambles to adapt to AI and tech giants spend vast sums in order to stay competitive in the capex arms race, TSMC’s position in the ecosystem is unique. Rather than facing obsolescence, TSMC is enabling innovation and increasingly capturing value from it. TSMC’s AI business is projected to grow more than fivefold over the next several years, with AI expected to account for more than 40% of total revenue by 2029.

What makes TSMC’s culture especially distinctive is its discipline around pricing. Despite having earned a dominant position, at a moment when foundry alternatives are scarce, TSMC has consistently chosen not to exploit, or even openly discuss, its pricing power. Instead, it has adjusted pricing broadly in line with cost inflation, delivering margin improvements primarily through operational efficiency. By offering price predictability and effective capacity to customers, while bearing the capital intensity, TSMC acts as a true enabler of innovation, reinforcing a win-win philosophy. That restraint – the conscious choice of not seeking to extract a disproportionate share of the value it creates – is striking, given that the chip designers who rely on TSMC earn some of the highest profit margins in the world.

Despite TSMC’s price discipline, the company’s ability to earn higher profits across industry cycles allows it to expand capacity and advance technology while competitors retrench – further widening the gap. Larger scale brings deeper customer relationships, higher demand visibility and the financial capacity to reinvest more aggressively than any peer. The flywheel, once set in motion by Morris Chang nearly four decades ago, turns faster with every cycle.

While many would agree that TSMC is a wonderful business, its shares have often traded at a discount to global peers, likely due to its physical location amid geopolitical tension cycles. While the risk of relations between China, Taiwan and the US meaningfully worsening is real, it is not unique to TSMC. Were the supply of chips to be disrupted, the consequences would be felt worldwide, especially by those users of technology and AI. In recent years, TSMC has also taken solid steps to diversify its footprint by building plants at scale in the US, Japan and Germany. As investors, our job is not to avoid this risk altogether, but to ensure that we are adequately compensated for it.

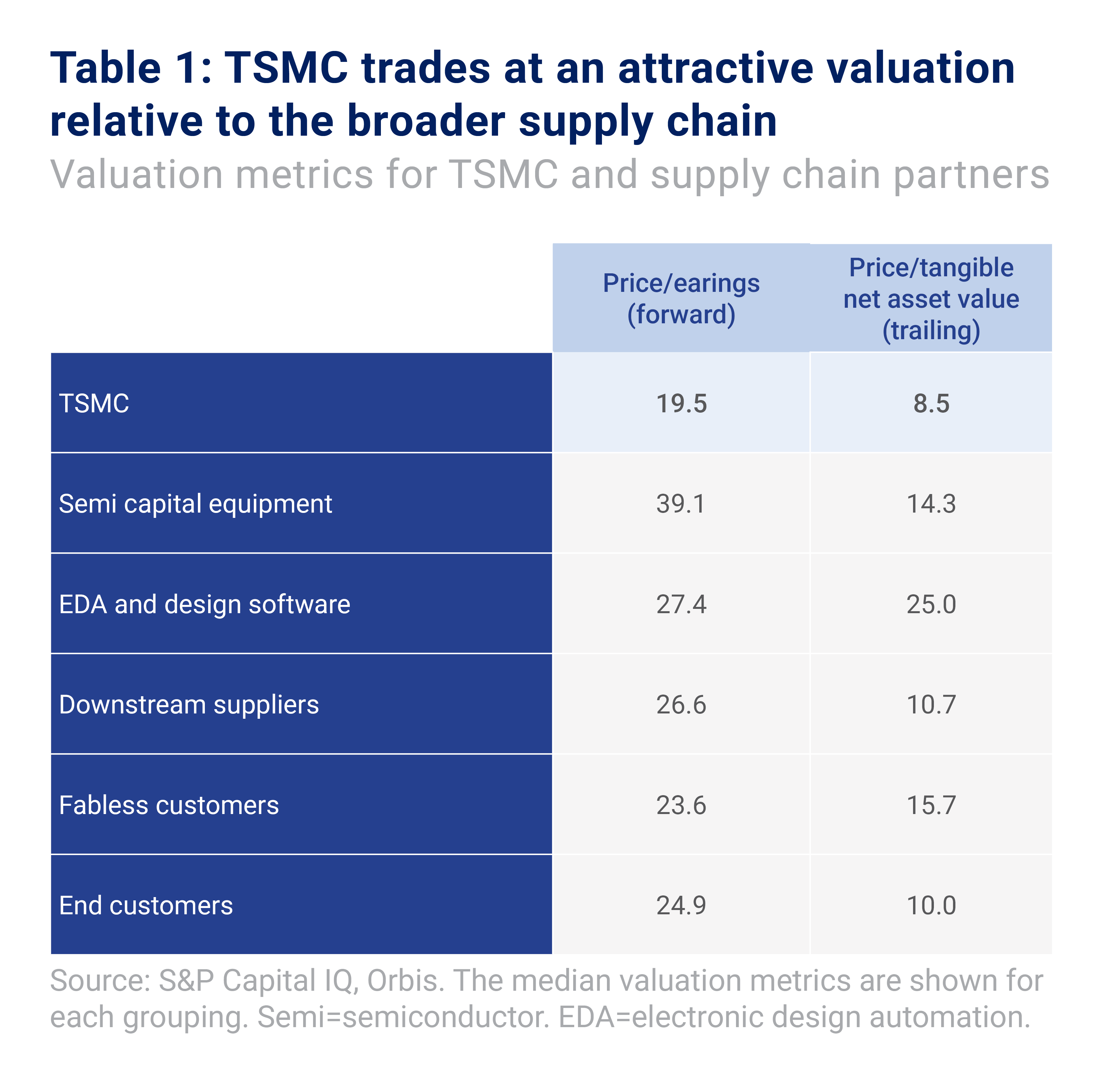

Today, shares in TSMC change hands at less than 20 times this year’s estimated earnings – a valuation that, in our view, is undemanding in light of the company’s unique qualities outlined above. TSMC also trades at a discount to the mega-cap tech companies that depend on its chips, as well as to many supply chain peers whose products, while critical, are also heavily reliant on TSMC’s partnership, as shown in Table 1. In our view, concerns around geopolitics and cyclicality have often overshadowed the enduring quality of TSMC’s underlying business, which creates the compelling investment opportunities we see from time to time.

We have owned TSMC for the best part of a decade. Over that period, the semiconductor cycle has turned several times. There have been phases when demand slowed, when geopolitical headlines dominated investor attention or when sentiment towards emerging markets weakened. These episodes have often weighed on the share price. But we view those moments as part of the compounding process rather than reasons to question the company’s long-term business prospects. TSMC has continued to do what excellent businesses do: reinvest in technology, deepen relationships with customers and grow earnings over time. The short-term volatility of the share price has rarely told us much about the long-term trajectory of the business and does not necessarily reflect changes in intrinsic value.

We opened this commentary with a simple belief: that the principal determinants of long-term returns are the quality of the underlying business, the people who run it and the price paid. TSMC is, in our view, the clearest expression of that belief in your portfolio. It is a company built on trust – trust earned over decades, one customer at a time, and defended not through pricing power but through the daily discipline of being the most reliable partner. In a world that remains unpredictable, that is the kind of business we want to own – and precisely why we remain, with conviction, long-term shareholders.