In investing, risk and opportunity are two sides of the same coin. Graeme Forster from our offshore partner, Orbis, unpacks current distortions in the market, including the “duration dislocation”, and provides insight into how Orbis is weighing up the risks versus the opportunities in the Orbis Global Equity Fund.

As painful as the first six months of 2022 have been for global stock markets, it’s worth keeping the decline in perspective. Since 2009, global equities are up about four times during a time when the yield on safe cash has collapsed to near zero. The difference between the two – the compensation that investors receive for buying risky assets – has been unusually wide, thanks in no small part to unprecedented support from central bank actions. Those actions have led the financial world to a strange and precarious place.

Today, we see three giant sources of risk and opportunity in global stock markets. First, and most importantly for us, valuation dislocations are extremely stretched and should unwind. Second, economic conditions may look extremely different from those of the last decade. Third, many industries may face a future that is extremely different from their recent past. And crucially, these three forces feed on each other.

Our job is to search around the world for the most attractively valued individual companies we can find. That leads us fairly naturally to be on the cheap side of valuation dislocations. Today, we are finding that many of the shares that look most attractively priced to us are also on the right side of the other two forces. The energy sector offers some of the clearest examples and serves as an excellent illustration of how we see markets today.

We will start by touching on the distortions in economic conditions and valuations, then we will walk through the current opportunity in energy to show how the three forces come together.

Duration dislocation

Since 2009, central banks have suppressed interest rates and bond yields, distorting the signals that interest rates usually provide. Normally, cash today should be more valuable than the promise of cash later, and normally one would expect compensation for the “time risk” of locking up money for a long time.

The past decade has not been normal. In this strange world, investors have been happy to pay up for the promise of potential profits in the distant future, sometimes even valuing faraway cash flows at a premium to more immediate cash flows. We call this the “duration dislocation”, and it seems to defy both conventional financial theory and common sense.

In time, we should expect to end up in a world where capital efficiency is restored … but it looks set to be a bumpy ride.

Within equities, it has – until the last few months – been fantastic for the valuations of speculative growth companies which lose money now but promise untold riches later, and it has been painful for the valuations of boring old economy companies that make plenty of cash now. The duration dislocation explains much of the valuation gap between value and growth shares, which has only begun to unwind after reaching levels rarely seen in history, as well as wide valuation gaps between US and ex-US shares and between the technology and energy sectors.

While the duration dislocation is unusual, it is not unprecedented. Similar conditions in the 1960s and the 1990s led to highly dislocated markets – the “Nifty Fifty” bubble in the early 1970s and the dotcom bubble in 2000. These valuation distortions did not just affect the performance of stock prices – they also had a profound impact on how capital was allocated in the real economy.

The same thing is happening now, and the energy sector offers a timely illustration.

Underinvesting in an energy crunch

As a society, we have gone through a remarkable transformation over the past two centuries. It wasn’t long ago that we relied almost entirely on human and animal muscle for farming, construction and manufacturing. The energy in the economy came largely from people and animals literally pushing things around. Modern machinery is far more efficient and powerful – as is the fuel that powers it.

Harnessing fossil fuels has been an enormous windfall for growth and productivity, as Vaclav Smil’s latest book, How The World Really Works, explains. Smil quantifies the “surplus” energy available to people today compared to pre-industrial levels. In the developed world, each person enjoys surplus energy equivalent to 60 adults working for you non-stop day and night, allowing for vast improvements in living conditions. In richer countries, like the US, surplus energy is more like 240 workers per person. But one of humanity’s greatest challenges is how unequally our energy windfall has been distributed – over one billion people in the world remain in energy poverty, consuming less than the average American fridge.

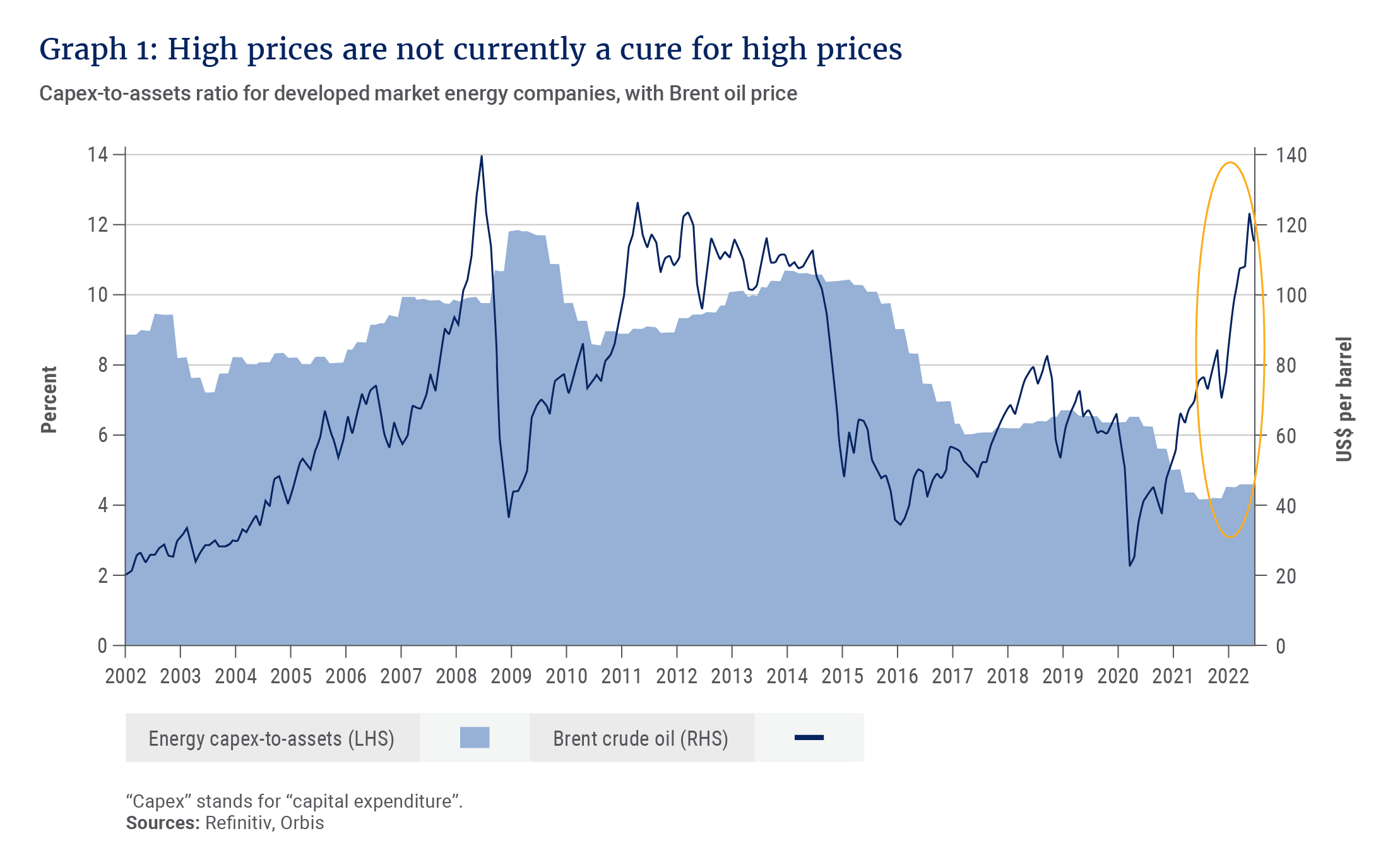

Given the importance of energy in our modern economy, we should expect to see steady capital investment over time to drive further gains in productivity and quality of life. It’s striking, therefore, that capital investment in primary energy has dropped significantly in recent years.

The recent dip in capital spending has been bigger than in prior cycles, so it will likely take longer to recover.

There’s nothing new about capital cycles. High energy prices ultimately cure high prices by attracting new investment and greater supply, which brings prices back down. This typically takes five to 10 years to play out in full. In the current environment, however, a longer and less efficient capital cycle heightens the possibility that we will see long-lasting volatility and scarcity of energy. The recent dip in capital spending has been bigger than in prior cycles, so it will likely take longer to recover. See Graph 1.

The current underinvestment is partly due to the duration dislocation. When investors value faraway cash as highly as cash today, they pour capital into startups that burn money to grow quickly, and they drain capital from old economy businesses that make money but grow slowly.

The falling investment in energy has also been driven by increasingly urgent climate concerns. For the first time in history, we are faced with the challenge of optimising our energy system not just for cost, but also for carbon. As stewards of our clients’ capital, our challenge is to understand how much of this energy transition is priced into current valuations, while also acting as responsible shareholders. As we look across businesses exposed both negatively and positively to longer-term energy prices, we don’t think the risk of prolonged energy scarcity is sufficiently appreciated.

Consider Shell, a roughly 2% position in the Orbis Global Equity Fund. Most people see Shell as a fossil fuel company, but we see it more as a diversified energy business that is well positioned to aid the transition by delivering various forms of energy to customers in an efficient and increasingly clean way.

In South Africa, Shell’s planned offshore seismic survey is a particular focus, and Orbis and Allan Gray analysts engaged with the company regarding this in December. Shell laid out the industry’s long experience with offshore surveys, the assessments they have conducted, and the planned mitigation measures that give them the confidence that they can conduct the survey responsibly while minimising risks to wildlife. We encouraged the company to publish a summary of their environmental impact assessment and to share the scientific evidence on which their views are based. The planned survey is currently suspended, and aspects of the project are now being debated in courts.

Globally, Shell has committed to net-zero emissions by 2050 along with interim targets for 2035 – targets that include not only its own emissions but also the impact of the energy products it sells to customers.

A key part of this is through Shell’s exposure to natural gas – a fuel that we see as key to facilitate the transition – but also through renewables, infrastructure and retail operations (refuelling stations). Shell’s trading arm, which plays a critical role in matching supply and demand for energy around the world, is unique in scale and likely to be increasingly valuable in a volatile and scarce energy environment.

While the duration dislocation is unusual, it is not unprecedented. Similar conditions in the 1960s and the 1990s led to ... the “Nifty Fifty” bubble in the early 1970s and the dotcom bubble in 2000.

One would expect Shell – as well as other critical energy infrastructure holdings such as Sunrun (solar), Vestas Wind Systems (wind), Constellation Energy (nuclear) and Kinder Morgan (pipelines) – to trade at a premium given the concerns around energy security that are beginning to emerge in all corners of the global economy. Rather than offering the promise of cash flows in the distant future, Shell is returning hard cash to investors today in the form of dividends and share buybacks, as well as increasing capital expenditures to more sustainable levels. On top of that, it offers longer-term inflation protection and resilience against energy shocks. But like many cash-producing businesses, Shell is still very conservatively priced, offering a mid-teens free cash flow yield.

Shell is just one example, but there are other companies in the Orbis Global Equity Fund that we believe will benefit from the unwinding of what, in our view, is a historic valuation dislocation. Today’s misallocation of capital has echoes of those in the 1960s and 1990s, but to us looks even more extreme. The current dislocation, coupled with the critical need to reduce carbon emissions, will likely drive higher and more volatile energy prices in the coming decade, improving fundamentals for businesses like Shell. It is also likely that the resulting inflationary environment will force central banks away from manipulating bond yields, providing an additional tailwind as cash today once again becomes more highly valued.

In time, we should expect to end up in a world where capital efficiency is restored, bringing things back into balance, but it looks set to be a bumpy ride.