Leonard Krüger and Nick Ndiritu look at how we have tailored our investment philosophy and process to invest in Frontier Africa markets. They discuss lessons learnt and how these have been applied to our South African portfolios.

From our experience investing in Africa’s frontier markets over the past decade, the most critical driver of long-term investment returns is finding great businesses with a competitive edge and trading at a discount to our estimate of intrinsic value. If this sounds familiar, it’s because it is the same approach we use to invest in South African markets, and it is the same approach used by our offshore partner, Orbis.

What is clear across geographies is that GDP growth and market returns are not correlated. Uncertainty and negative sentiment, often driven by poor macroeconomic factors, tend to drive asset prices down, presenting an attractive buying opportunity for long-term investors. In a severely under-researched part of the world like Africa (outside of South Africa), having a strong, independent research process helps to unearth bargains. Having the patience and courage to take a contrarian approach can yield attractive long-term returns.

While our investment philosophy has remained the same, we have adapted certain aspects of our investment process to fit the nuances and challenges of operating in frontier markets, including incorporating country risk assessment.

How we approach investments in Africa’s debt markets

One example is our approach to investments in debt markets, where we developed a framework to assess currency and credit risks across different countries. This internal credit rating framework focuses on the risk of loss and considers factors such as: What is the fiscal balance, how reliant are they on commodities, what type of commodities, the ability to service debt obligation, etc.

Our analysts write detailed credit analysis reports on individual countries and corporates and the investment team subsequently votes on a risk rating, which determines the exposure limits.

We benefit from a cross-pollination of ideas by leveraging insights from the broader investment team; if we have researched a company from an equity perspective these findings will inform our decisions when appropriate.

Lessons learnt

While having a robust process helps, we aren’t always going to get things right, and we have learnt many lessons along the way. These have been beneficial for our forays further into Africa and have provided a new perspective on local investments too.

1. African markets are not all the same

There is a misconception that markets in Africa, north of South Africa, are all the same, which is of course not the case. We have learnt to appreciate nuances of different markets.

In Nigeria, for example, it is important to establish relationships and understand business incentives and operations.

In Kenya, we have been struck by the entrepreneurial spirit of the people, where the success of Safaricom’s M-Pesa is a prime example of the far-reaching impact that successful fintech businesses can have.

We have learnt hard lessons in Zimbabwe, where irrational and destructive legislation has persisted for longer than was imaginable. Reported business profits, under the previous US dollar monetary regime, were very different to what was actually happening on the ground, and we have had to adjust valuations accordingly.

In Egypt we have seen the country pivot from the Arab spring in 2011 to a military coup in 2013 – yet have found businesses able to withstand the tremendous political turmoil and thrive, for example, Eastern Tobacco.

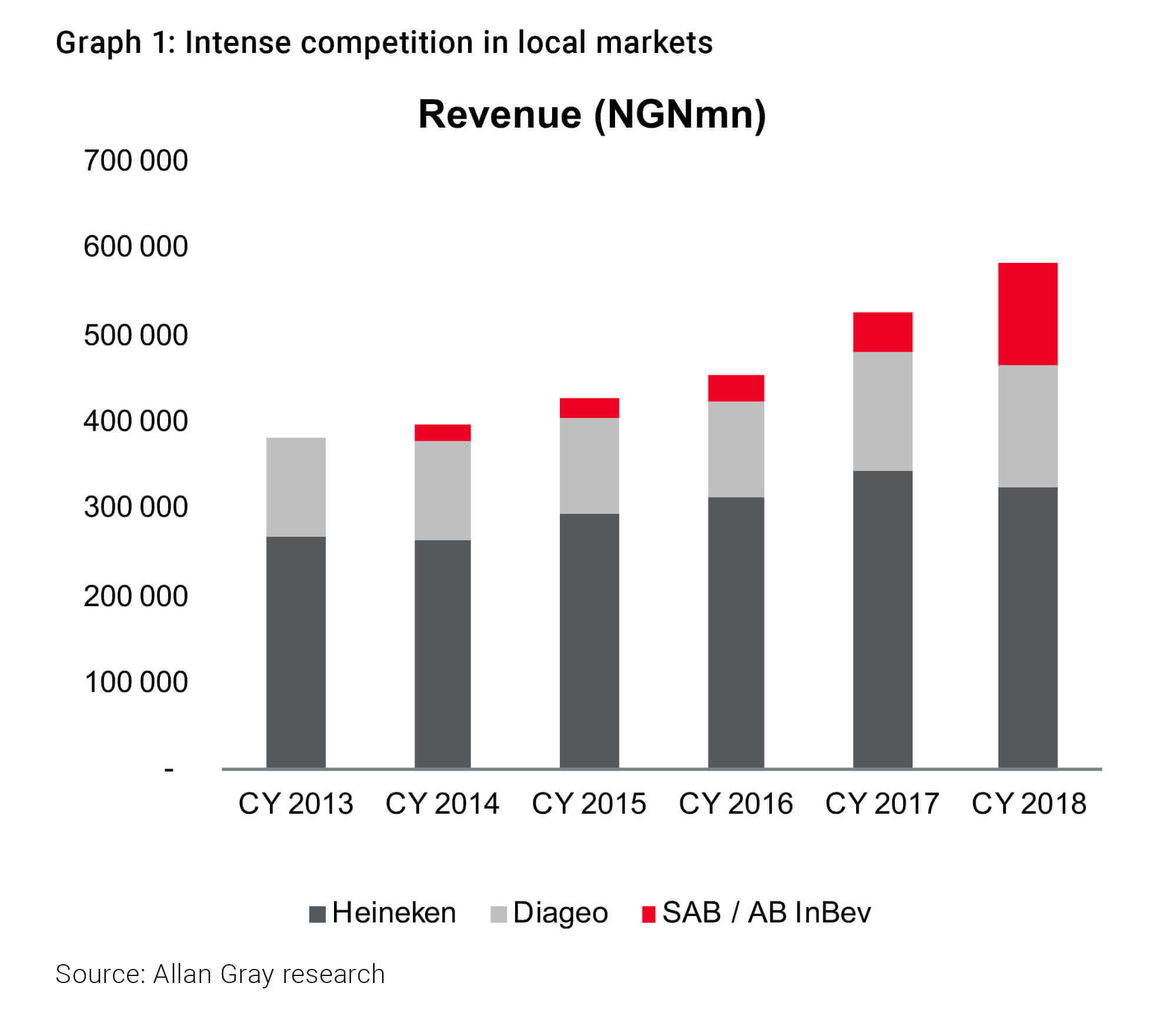

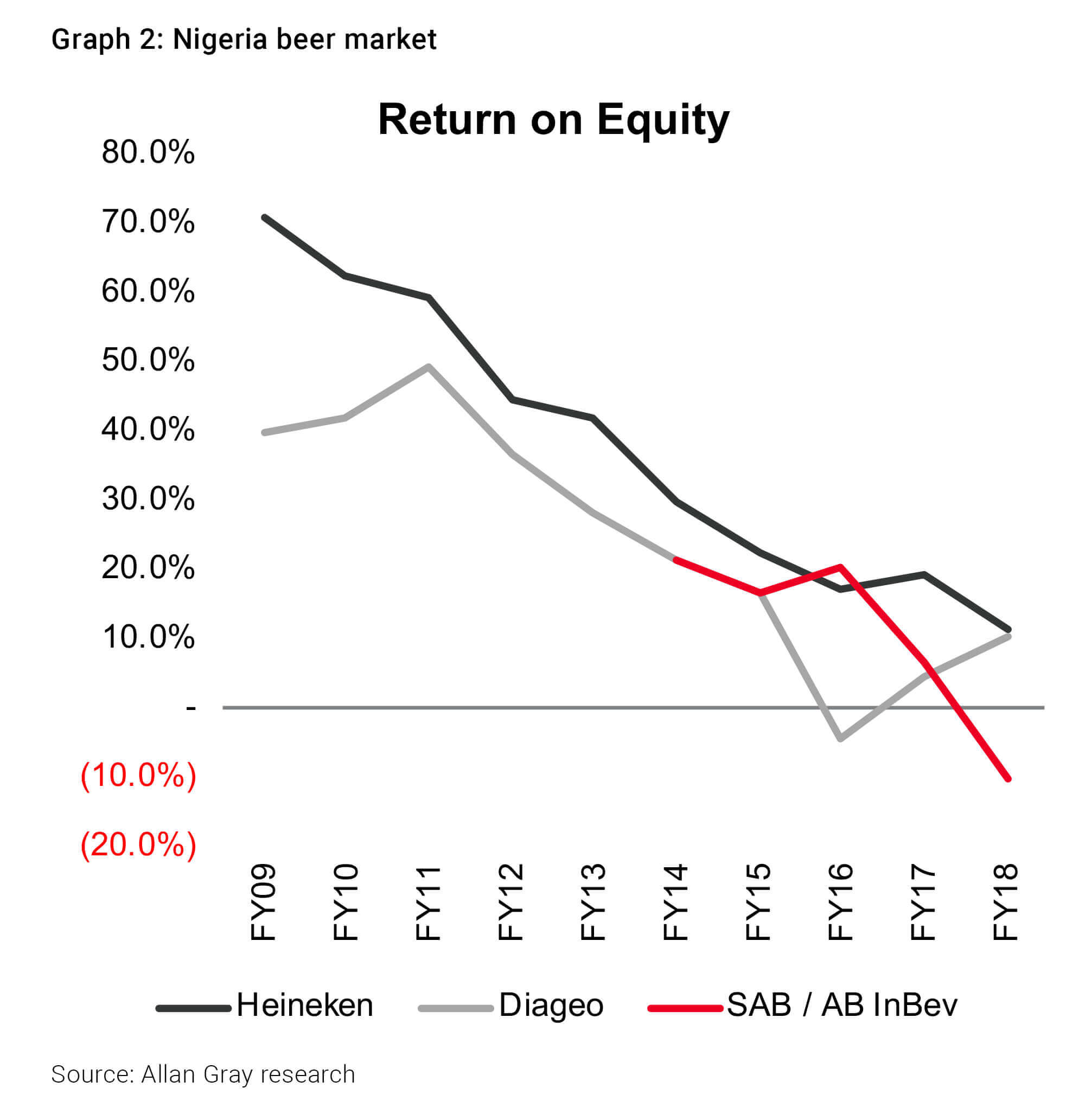

2. There is intense local and international competition

One common misperception is that African markets are virgin territory for many South African businesses. However, there are well-established competitors in these markets and South African businesses need to establish their competitive edge and be prepared to fight it out.

One example is SAB’s successful market entry into Nigeria’s beer market, but it has come at a cost of reduced profitability for the whole sector. As shown in Graphs 1 and 2, SAB has been incredibly successful in gaining market share in Nigeria’s beer market, but the profit pool has shrunk due to increased price competition. SAB has established a competitive position in Nigeria, but this investment hasn’t yet delivered profitable returns for shareholders.

3. Value the differences in business quality across countries appropriately

Some industries, like banks, are conceptually the same irrespective of their geography. At its most basic level, a bank takes in deposits from clients and lends those funds to other customers seeking credit, charging interest and fees in the process. South Africa has a much more sophisticated and diverse banking system than Nigeria, for example. Comparing FirstRand from South Africa with Guaranty Trust (GT) Bank in Nigeria is instructive. Both are high-quality businesses and leaders in their respective markets, involved in the same fundamental activity of taking deposits and making loans. The regulatory environment, market maturity, the role of government and competition differ markedly though. Despite a return on equity (ROE) higher at GT than FirstRand, the valuation metrics of GT deserve a deep discount to that of FirstRand.

Lessons learnt applied to our South African portfolios: MTN case study

Our investment in MTN provides a useful case study. MTN was one of the largest holdings in Allan Gray funds up to 2011/12. The business enjoyed tremendous success and was growing fast on most metrics. Its success in Nigeria, in particular, stood out. By the 2014 financial year, Nigeria accounted for over a quarter of subscribers, more than a third of revenue, half of earnings before interest, tax, depreciation and amortisation (EBITDA) and almost 60% of operating free cash flows for the MTN group.

One of the things that concerned us greatly was the currency peg in Nigeria, which was fixed relative to the US dollar. The benefit MTN enjoyed over this time from a weaker rand against the US dollar (and by implication the naira in Nigeria) was not well understood by market participants, in our opinion; nor was the vulnerability of Nigeria’s ability to maintain the currency peg. We reduced our position as we didn’t believe it was sustainable. Ultimately, the naira depreciated from NGN160/US$ to NGN360/US$ between 2015 and 2017. MTN has underperformed the FTSE/JSE All Share Index (ALSI) materially since 2014.

Lessons applicable more broadly

We are applying the lessons learnt in Frontier Africa markets to our local investments. We have learnt that patience does pay off. Establishing the right price to take a position and having the stomach to wait for the right price to sell at, helps clients make money over the long term. The human element and importance of trusted relationships are essential in new markets and new investment types. Understanding businesses and the operating environment well, spending time with management, as well as their competitors, getting to know the nuances, trading and liquidity conditions: these are all key to successful investing.