There is a perception that we do not regard listed property as an attractive investment for our clients. This is not the case. It is, however, true that our clients have had below-average exposure to listed property. Mark Dunley-Owen explains the rationale behind this long-held view and why the time may be right to shift gears.

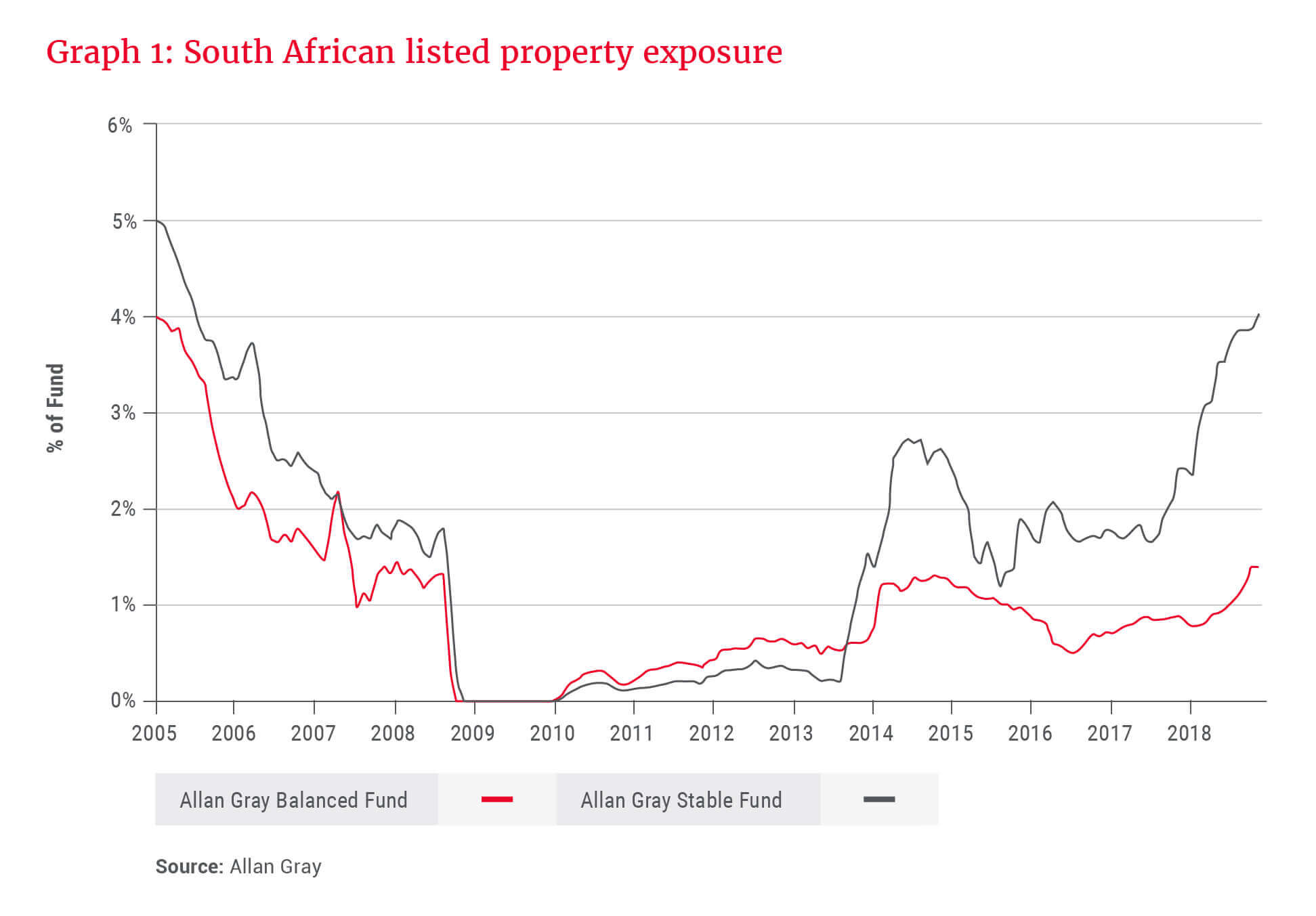

The mandates of the Allan Gray Balanced Fund and Stable Fund allow us to invest our clients’ money across asset classes such as equities, bonds and property. The asset allocation changes depending on where the portfolio managers are finding value at any given point in time. Graph 1 shows the percentages of the funds’ holdings that have been invested in South African property since 2005. The percentages are low, in both absolute terms and relative to peers. This is not because we are biased against investing in property, but rather this reflects our investment philosophy and focus on long-term intrinsic value.

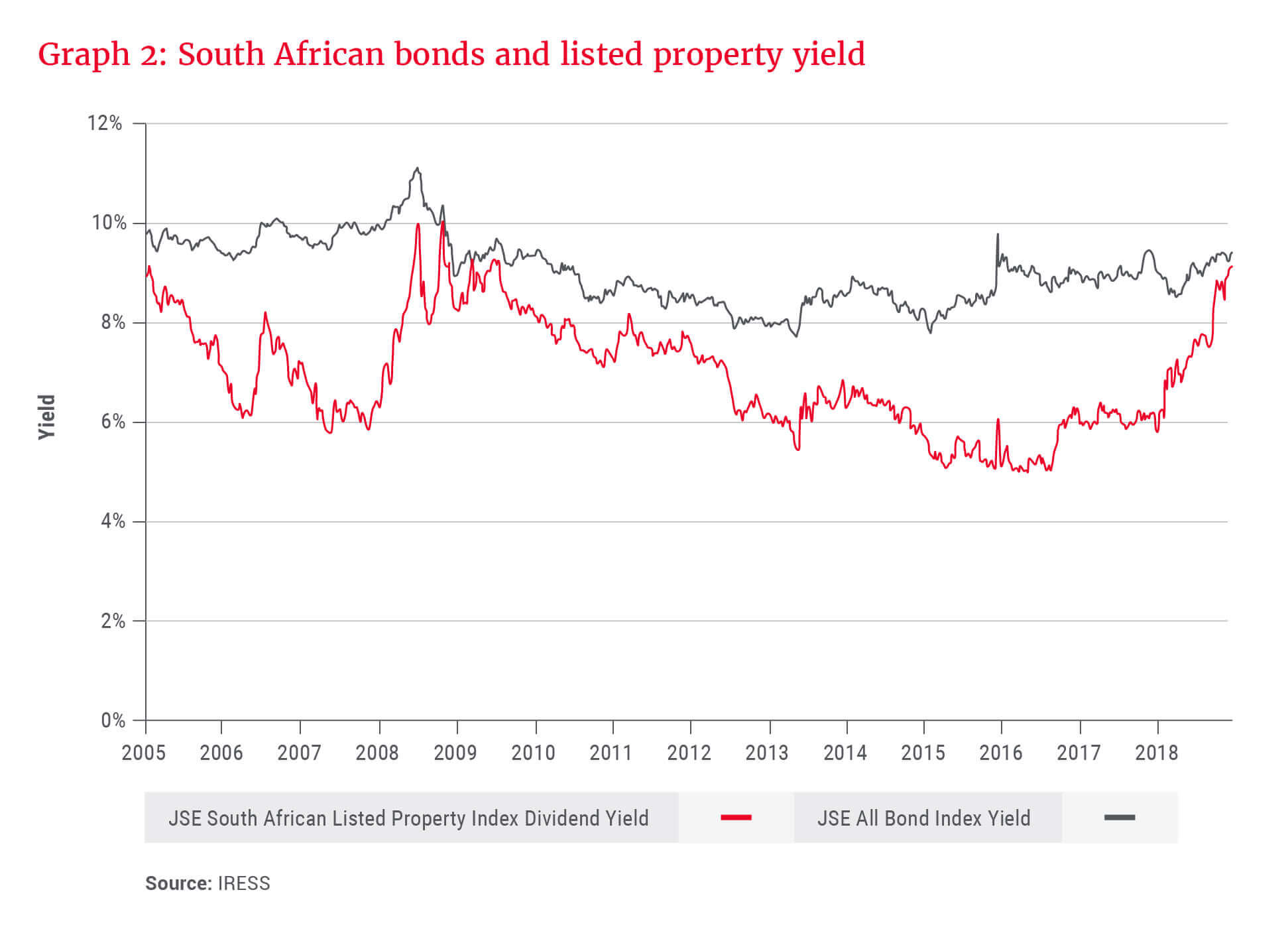

Graph 2 shows the dividend yield from listed property, represented by the JSE South African Listed Property Index (SAPY), and the yield from bonds, represented by the JSE All Bond Index (ALBI). Following the global financial crisis in 2009, South African property and bonds offered a similar yield, suggesting that listed property was attractive. It subsequently returned more than 100% and was the best-performing asset class between 2009 and 2016.

In hindsight, our funds’ low allocation to property over this period was a mistake. However, our decisions were based on concerns which we believed reduced the intrinsic value of listed property, including:

- The risk inherent in the distributions

- Misalignment of management and long-term shareholders

- Misallocation of capital

The risk inherent in the distributions

Many investors assume that property offers reliably growing income distributions and limited risk of capital loss. The former makes it attractive compared to the static distributions from bonds; the latter makes it attractive relative to more volatile equities. We disagree with both of these assumptions.

It is a mistake to equate property with bond distributions. A bond is a senior ranking debt investment that pays predetermined coupons, while listed property is an equity investment that pays distributions out of company profits. Property distributions are less certain and more volatile than bond distributions, and may fall if company profits do similar.

It is also a mistake to assume that any equity investment, including listed property, has a low risk of capital loss. This may be true in some instances, particularly in the case of a relatively simple business backed by physical assets such as property. However, capital loss is influenced by other factors, such as starting price and financial engineering. In an environment of rising property prices and acquisitive growth, listed property is essentially a subordinated claim on highly priced assets funded by a lot of debt; capital loss is probable for such investments.

Misalignment of management and long-term shareholders

Aligning management incentives towards the creation of long-term value encourages decisions to be made in the best interests of shareholders. There are characteristics of listed property that suggest this is not always the case.

Due to the flawed assumptions discussed earlier, many investors invest in listed property to earn income. This encourages management to make decisions that target short-term distribution expectations at the expense of long-term value, for example, refusing to sell low-quality assets because they are high-yielding. This goes against our investment philosophy, and the long-term time horizon of our clients.

The focus on distributions may also encourage management to pay out more cash than the business generates. We view free cash flow as the cash generated by a business, less capital investment that is needed to maintain the ability to generate comparable future cash flow. In the quest to grow distributions, some listed property companies pay out more in dividends than their free cash flow, funding the deficit by issuing shares, taking on more debt or underinvesting in their assets. This strategy works when share prices are high and debt is readily available, but is unlikely to generate value through the cycle.

Misallocation of capital

The majority of recent investments made by South African property companies have been outside of South Africa.

Taking educated bets on an unknown future is part of management’s job. However, experience suggests that most countries are more competitive and less profitable than South Africa, and few people are as skilled at creating value in other markets as they are in their backyard.

While some recent offshore property investments have paid off handsomely, others appear to be justified by currency diversification, size and artificially low funding rates, rather than a rational process that allocates capital to the highest return opportunities. Such deals may benefit management’s compensation and prestige, but are unlikely to generate long-term shareholder value.

Our investment philosophy focuses on fundamentals

Few investors shared our concerns while the property market was performing well. Nonetheless, our belief that intrinsic value was lower than that implied by market prices made it appropriate to limit our clients’ exposure. Our conviction deepened as property fundamentals deteriorated, in particular the increasing supply of property and worsening public service delivery.

A landlord sells space, the price of which is determined by demand and supply. South Africa has experienced a property construction boom for much of the last two decades, most notably in retail shopping centres and office nodes such as Sandton. At the same time, South Africa’s economic growth has declined due to structural deficiencies, and demand for space has been less than expected. We expected this combination of rising supply and weak demand to result in lower rentals to keep space occupied.

Property companies invest large amounts of money in immovable assets with long lives. This makes them particularly susceptible to the poor public service delivery that has become prevalent in South Africa. Inept municipalities limit the approvals and services needed for further investment, thereby restricting growth. Rising non-discretionary rates and utility costs crowd out the ability of tenants to afford higher rentals.

These and similar factors suggested it was unlikely that property companies would grow their distributions in line with history or market expectations. In contrast, the yield on property had declined to 4% lower than the yield on bonds by early 2016 (as shown in Graph 2). This was a notable divergence from history, indicating that property was unusually expensive (low yields mean high prices) despite the worsening environment. We reduced our clients’ property holdings further.

Patience can pay off

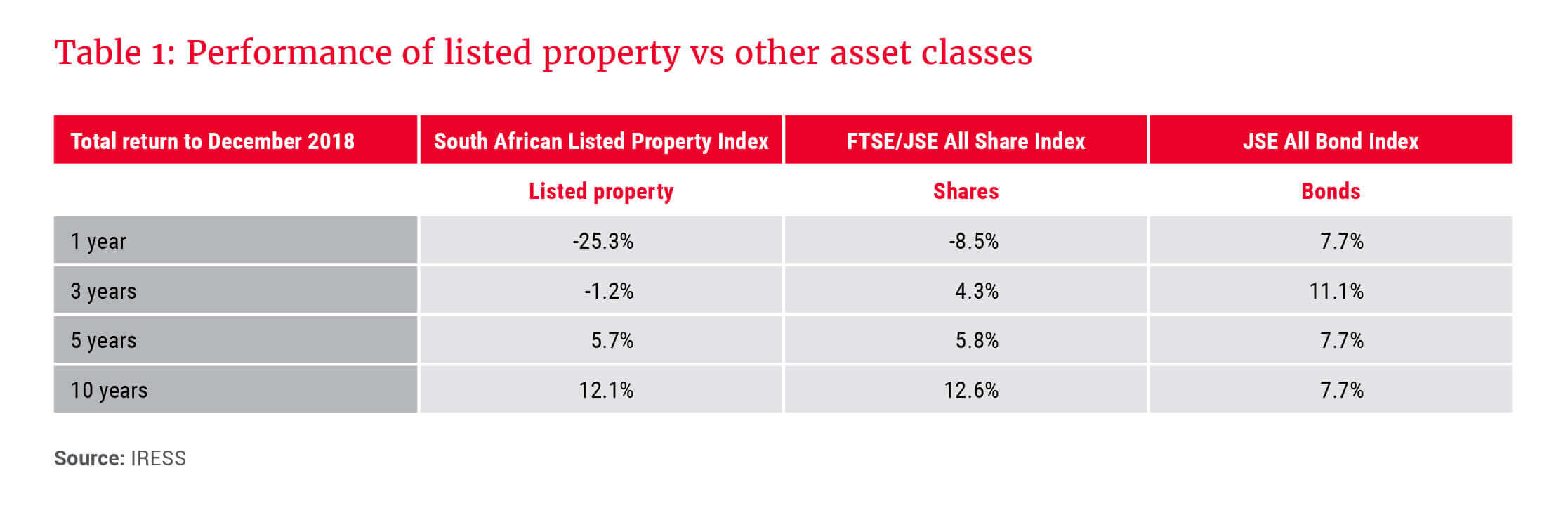

Recent performance suggests our patience was warranted. Listed property, represented by the SAPY, has fallen 28% since peaking in April 2016, generated negative returns over the last three years and was the worst performing asset class in 2018 (see Table 1).

Following the recent correction, the SAPY dividend yield is again on a par with bond yields, suggesting that property offers similar relative value as it did in 2009. Some of our concerns about the asset class are also being addressed. Thus, we have begun selectively investing in listed property companies that are priced below our assessment of intrinsic value, in particular those run by management that is aligned with shareholders, uses appropriate financial gearing, focuses on cash flow rather than accounting earnings, and prioritises long-term value over short-term metrics.

It is difficult to find property companies that tick all these boxes, but some come close:

- Attacq is best known for developing Waterfall City in Midrand. Building a new city requires the long-term value-creation mindset that is aligned with our philosophy. The share is priced at a substantial 40% discount to net asset value (NAV), and NAV should grow as Waterfall City matures into the prime node between Sandton and Tshwane. Our concerns include high debt and questionable free cash flow, but we believe these are being addressed.

- Octodec mainly owns residential and retail buildings in the Johannesburg and Tshwane CBDs. Their buildings are functional and affordable rather than pretty, in line with what their tenants need. Most of their properties are on short-term leases with rentals that reset to market levels regularly, unlike many other property companies. Their properties are valued sufficiently cheaply to make redevelopments attractive as and when demand grows. Management owns a substantial share of the business. The share is priced at a 35% discount to NAV with higher than 10% dividend yield.

- Equites Property Fund specialises in high-quality logistics buildings that are used to store and distribute goods. Gearing is low, accounting is transparent, and management has substantial shareholdings. Unfortunately, Equites’s quality is well-known and the share trades at a premium to NAV and relatively low dividend yield. This, plus questions we have over their recent expansion into the competitive UK logistics market, have limited our clients’ holdings.

We will continue to invest our clients’ money into these and similar companies when they are priced below our assessment of intrinsic value. We apply this philosophy across all asset classes, including property, in order to maximise our clients’ long-term wealth.