As part of our investment process, we monitor developments under the environmental, social and governance (ESG) pillars to understand how they may affect the long-term sustainability of companies. Within the social pillar, the alcohol industry offers a topical case study to demonstrate our approach. Stephan Bernard takes a closer look at the latest trends in alcohol consumption.

In developed markets such as the United States, alcohol consumption has moderated since its COVID-19 pandemic-era peak. This has prompted concerns about a possible structural decline, mostly attributed to changing behaviour among under-30s, who are characterised as a more sober and health-conscious generation. At face value, survey data appears to support this narrative, showing lower drinking prevalence in this group.

However, there are several factors to consider.

- Over the long term, much of the decline in self-reported participation among young people in the US reflects a sustained reduction in underage drinking. Once individuals reach legal drinking age, prevalence rates tend to revert. In other words, young people are starting later, rather than opting out entirely.

- Survey data alone is unreliable. People generally underreport their vices, even if they do not consume excessively. The objective data is less dramatic. Despite recent softness, absolute US per capita alcohol consumption remains within its long-term range. With several major events ahead, including the FIFA World Cup and the 250th anniversary of US independence, 2026 could prove stronger than expected.

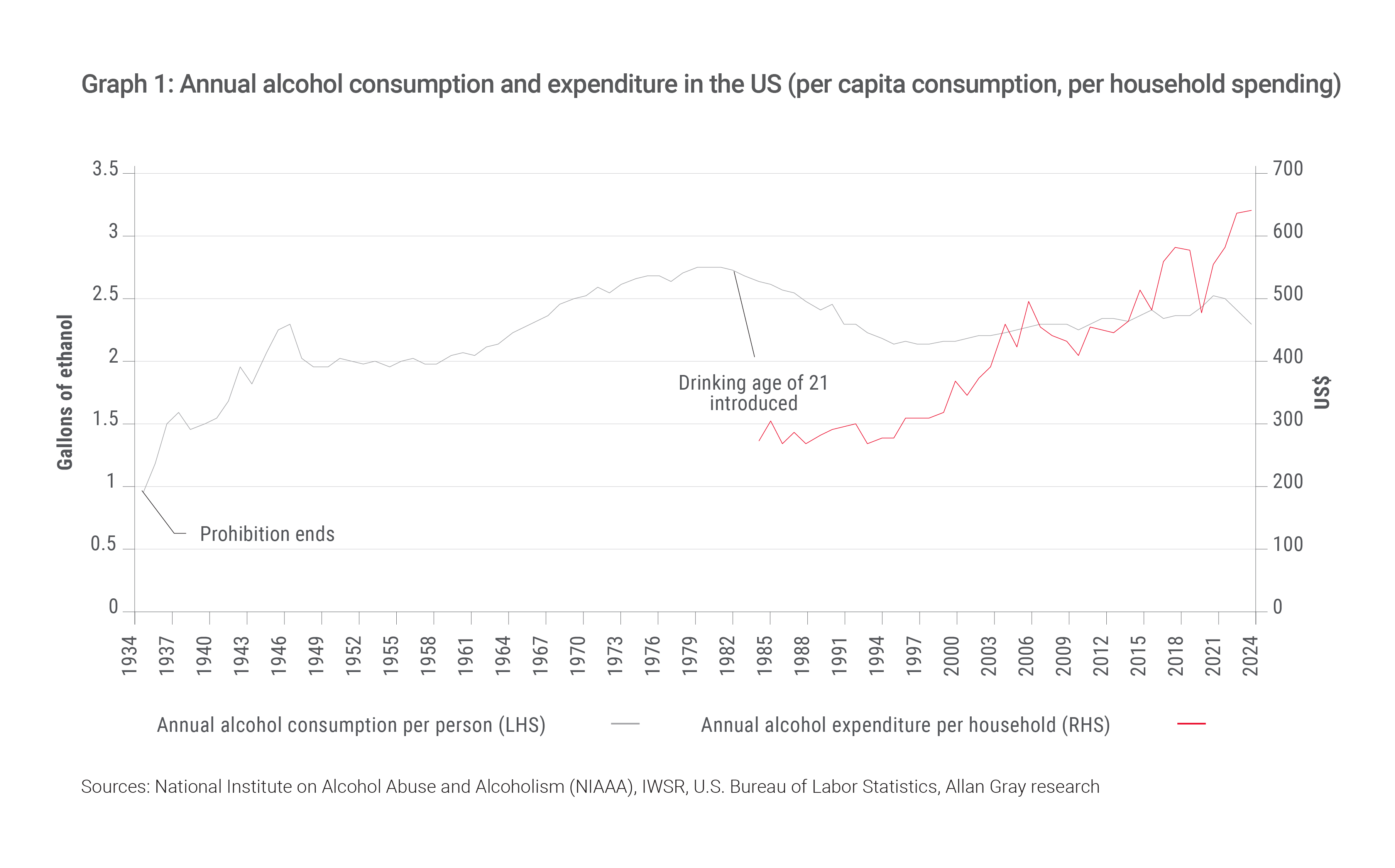

- While people may drink less, they are not spending less: Inflation-adjusted household spending on alcohol in the US has remained broadly flat over the past 20 years, as shown in Graph 1. What is lost in volume can be recouped from consumers moving up the pricing ladder (a trend called “premiumisation”). Older age groups continue to increase their spending, while lower expenditure among younger consumers may owe more to affordability constraints than to shifting preferences.

- Demographics matter. In markets where populations are still growing, the impact of lower per capita consumption on total demand is less severe than survey data might suggest.

We are also mindful of the impact that “new” influences and economic strain may have on consumption going forward.

Emerging markets remain a growth story

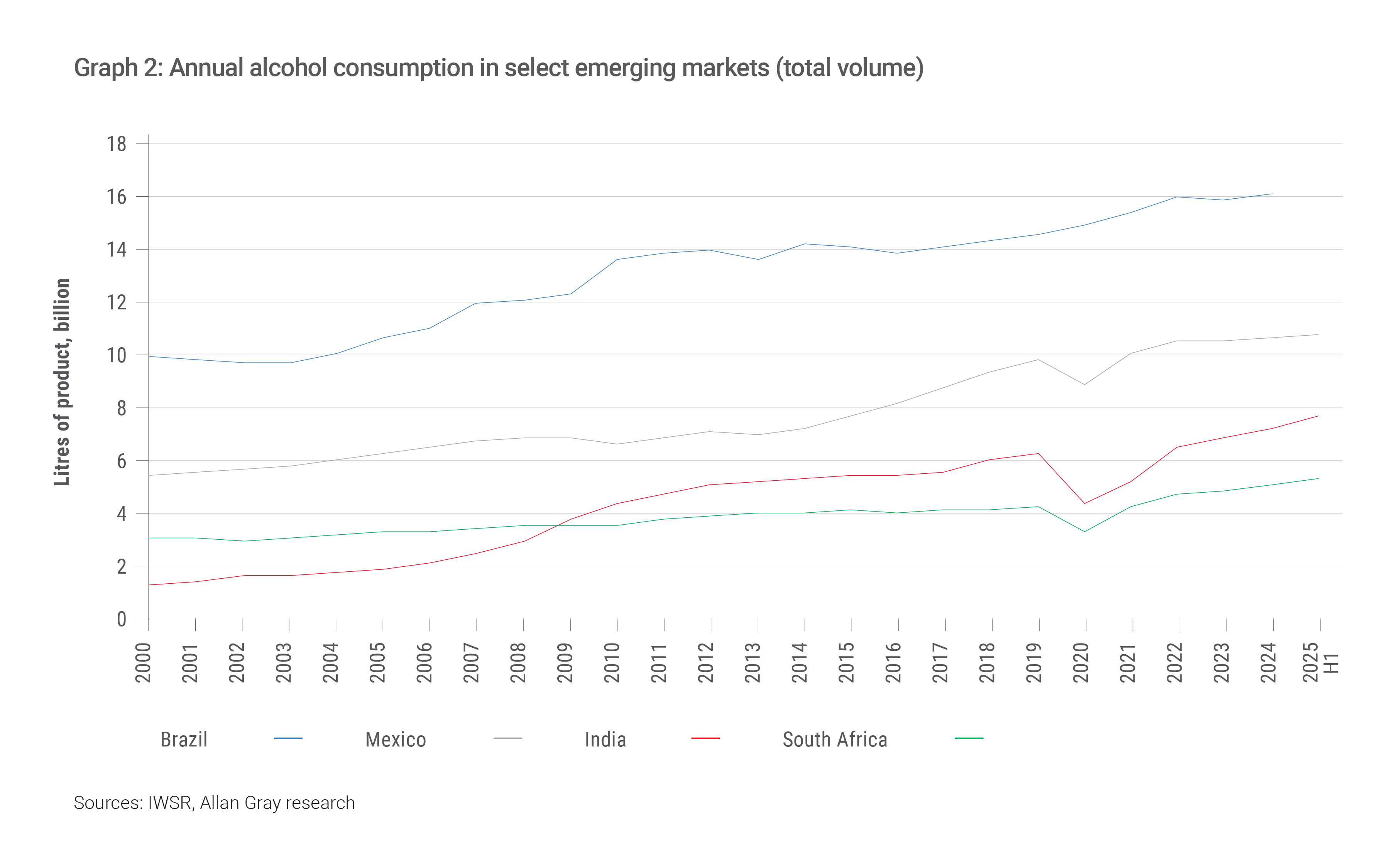

While developed markets dominate the public debate, emerging markets paint a different picture. Across most emerging economies, alcohol consumption has continued to grow in line with rising incomes and urbanisation. As demonstrated in Graph 2, countries such as India, Brazil and Mexico are seeing volume growth as new consumers enter the market.

India stands out. Alcohol consumption remains a fraction of that seen in developed markets, but growth has been rapid, particularly among affluent young adults. Recent data shows strong demand across beer, spirits and ready-to-drink products. This reflects a familiar pattern observed historically: Alcohol consumption tends to rise as economies grow before eventually stabilising at higher income levels.

China is an exception. Consumption has fallen sharply since the mid-2010s, driven not by health considerations or evolving consumer preferences but by far-reaching government austerity measures that curtailed alcohol use in official and business settings. Despite lower volumes, the alcohol industry in China has been partially insulated through premiumisation, with consumers drinking less but choosing higher-quality products.

New influences: medicines, cannabis and alternatives

Our research also monitors emerging factors that could influence future consumption. One widely discussed topic is the impact of GLP-1 weight-loss drugs. Opinions are mixed, with some expecting a dramatic reduction in alcohol demand, while evidence currently suggests a more modest effect. Transaction-level data indicates little change in alcohol spending (-1%) among US households with at least one GLP-1 user. However, the impact could become more meaningful over time if prescriptions expand to treat alcoholism and obesity, and as oral formulations increase access and uptake. It is still too early to draw definitive conclusions.

To the extent that people consume alcohol to “take the edge off”, cannabis is mooted as a potential substitute, particularly appealing to younger adults. Legalisation has expanded access in several regions. The evidence is mixed: some consumers substitute alcohol with cannabis, others use both, and long-term impacts remain uncertain. Experience in countries with long-standing cannabis availability, such as the Netherlands, suggests that alcohol demand should remain intact.

No- and low-alcohol beverages have grown in popularity on the back of the moderation trend, attracting new consumers and broadening drinking occasions. No-alcohol beer has gained meaningful market share in parts of Europe and is growing quickly elsewhere. This reflects changing norms around moderation and inclusion, allowing consumers to participate in social gatherings without alcohol.

For alcohol producers, and brewers in particular, this represents a growth opportunity, as research suggests that no-alcohol beer is not only offsetting lost beer volumes but also attracting consumers who would otherwise choose soft drinks.

Health awareness and regulatory pressure

From a social perspective, health considerations are central. Alcohol is classified as a carcinogen, and health risks increase with consumption. Public awareness of these risks has grown, and regulators are increasingly reflecting this in policy.

Alcohol-related mortality rates remain elevated in several developed markets, reinforcing the likelihood of stricter regulation over time. Governments and health organisations are promoting more conservative drinking guidelines, stronger warning labels and tighter marketing restrictions. Against the stream, the 2025-2030 Dietary Guidelines for Americans shifts from explicit consumption limits towards broader moderation-based language.

Evidence suggests that prominent health warnings can reduce alcohol sales, although the magnitude varies by market and design. However, greater awareness does not automatically translate into lower consumption. Financial pressures are often a stronger driver of moderation than health concerns, and these pressures can be more cyclical. This highlights the importance of understanding alcohol use within the broader social and economic context.

Social behaviour is evolving

Alcohol consumption is closely tied to how people socialise. Younger generations spend more time online, live with their parents for longer, report higher levels of social isolation and have fewer in-person interactions than previous cohorts. These shifts reduce the number of traditional drinking occasions, particularly among teenagers and young adults.

At the same time, cultural narratives can exaggerate trends. Concepts such as being “sober-curious” receive significant media attention, but consumption data suggests that they remain behaviours concentrated in wealthier markets.

Alcohol in the portfolio

We do not believe the headwinds discussed above present insurmountable challenges for the alcohol industry. Within this context, we find Anheuser-Busch InBev (ABI) attractive on a valuation basis, including when ESG considerations are incorporated:

- Beer is winning share of throat away from spirits and wine. As the world’s largest and most profitable brewer, ABI will naturally benefit from this shift.

- Increasing affordability pressures should support beer relative to other alcoholic beverages going forward, as should the moderation theme, given beer’s lower alcohol content. ABI can also scale its no- and low-alcohol beer portfolio.

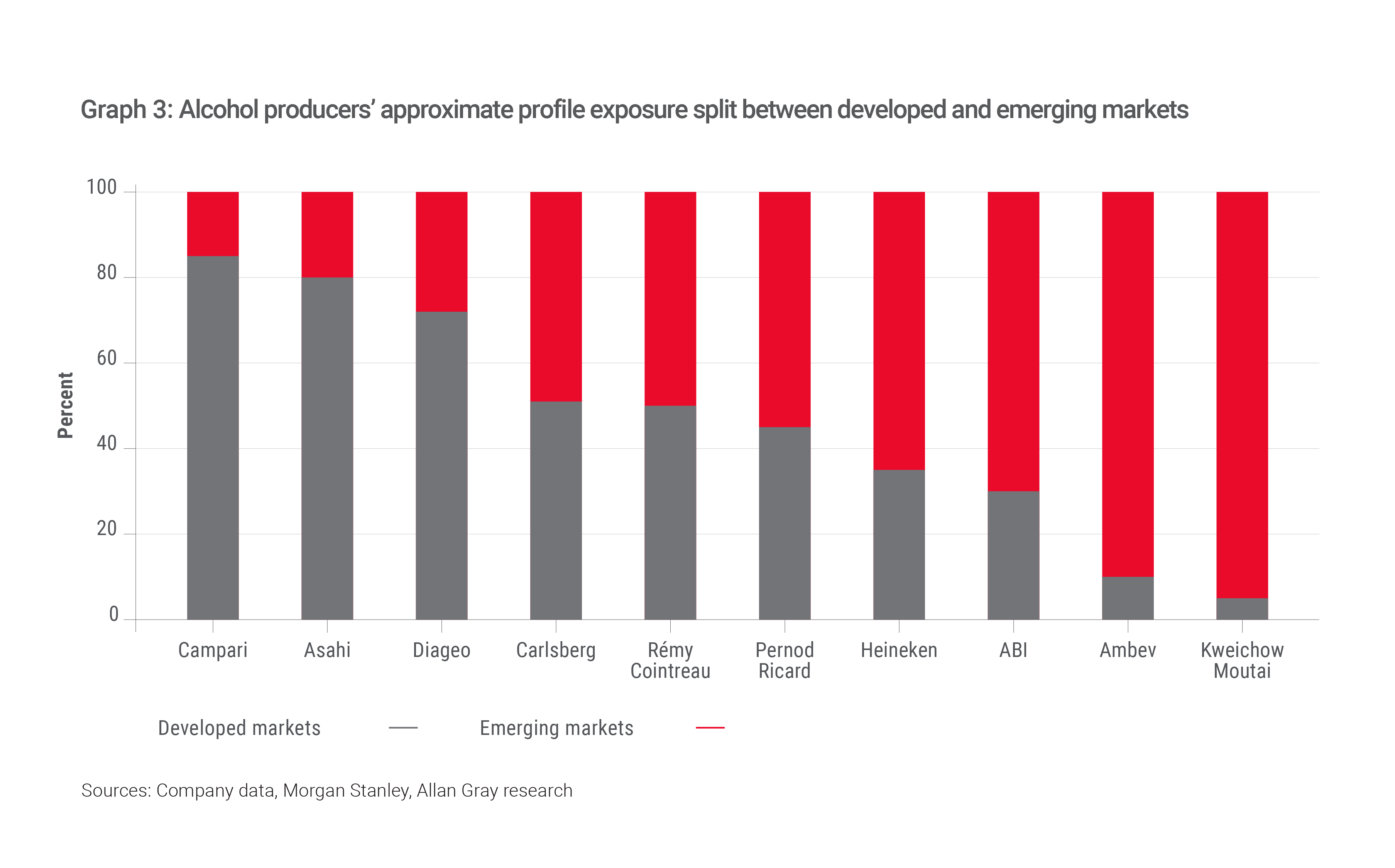

- ABI is more exposed to emerging markets than its competitors (see Graph 3) and stands to benefit from consumption growth in those markets.

- ABI is encouraging consumers to trade up to newer aspirational brands. As consumers have become increasingly fickle, this requires a strong innovation pipeline and superior brand-building competence to ensure the product portfolio hits the sweet spot of consumer demand. Fortunately, ABI leads peers in its ability to launch and scale new beverages. While premiumisation may have its limits, ABI stands to benefit from margin expansion on more supportive input prices and a weaker US dollar.

- At a portfolio level, ABI tends to behave differently in times of market upheaval; it is a natural hedge against South Africa and China’s general risks (both are small in its business mix), and its core product is unlikely to be disrupted by artificial intelligence.

For more details about our stewardship efforts, please see our latest Stewardship Report.