Finance Minister Enoch Godongwana delivered his maiden Budget speech on Wednesday, 23 February. He noted that although the easing of COVID-19-related restrictions supported a return to economic growth in 2021, the country is still under financial pressure and dealing with the effects of the pandemic, rising inflation, increased fuel prices and a series of interest rate increases. The Minister acknowledged that now is therefore not the time to increase taxes, which would put the economic recovery at risk. The theme of this year’s Budget is “keeping money in the pockets of South Africans”.

Gross tax revenue for 2021/2022 is expected to be R181.9 billion higher than projections in the 2021 Budget and R61.7 billion higher than projected in the 2021 Medium-Term Budget Policy Statement. Corporate income tax collections from mining account for most of this surplus, with personal income tax collections and VAT also performing above expectations. For the past two years, the focus has been on broadening the tax base, improving administration, and lowering tax rates. Government intends to continue with this approach while avoiding tax rate increases as far as possible. Implementation of structural reforms will contribute to economic recovery and improved tax collection.

Due to the revenue improvement, government proposes R5.2 billion in tax relief to help support the economic recovery and to provide some respite to South Africans.

There is also a continued focus on rebuilding the South African Revenue Service (SARS). Over the past year, SARS has recruited additional staff and invested significantly in modernising its systems and infrastructure, which has resulted in improved revenue collection and tax compliance. A dedicated new unit focused on high-wealth individuals is also in progress.

Below we highlight some of the 2022 Budget tax proposals that may impact investors. These changes come into effect on 1 March 2022, unless otherwise indicated.

What were the highlights?

The key take-outs from this year’s Budget are summarised below:

- Inflationary relief through a 4.5% adjustment in the personal income tax brackets and annual tax rebates.

- As announced in last year’s Budget, the corporate income tax rate will reduce by 1%, from 28% to 27%, effective for years of assessment ending on or after 31 March 2023.

- No increase in the general fuel levy or the Road Accident Fund (RAF) levy.

- The monthly benefits for employers under the employment tax incentive will be increased by 50% to R1 500.

- Excise duties on alcohol and tobacco will increase by between 4.5% and 6.5%.

- The health promotion levy on beverages will be increased by 0.1 cent to 2.31 cents per gram of sugar from 1 April 2022.

- The plastic bag levy will increase by 3 cents to 28 cents per bag from 1 April 2022.

The following applies for the period from 1 March 2022 to 28 February 2023, unless otherwise stated:

Individuals and special trusts

Personal income tax brackets will be adjusted in line with the expected inflation rate of 4.5% for the 2022/2023 tax year. This relief will mainly impact individuals in the middle-income group.

This means that taxpayers earning above R226 000 will fall into the 26% tax bracket. The highest marginal tax rate for individual taxpayers remains unchanged at 45%. The personal income tax rates for the 2022/2023 tax year are listed below.

Tax thresholds

The tax-free thresholds for personal income taxes will also increase in line with the 4.5% expected inflation rate for the 2022/2023 financial year to the following:

- R91 250 for taxpayers younger than 65

- R141 250 for taxpayers age 65 to 74

- R157 900 for taxpayers age 75 and over

Rebates

The primary, secondary and tertiary rebates (deductible from tax payable) will increase to the following:

- R16 425 per year for all individuals

- R9 000 for taxpayers age 65 and over

- R2 997 for taxpayers age 75 and over

Medical tax credits

Monthly tax credits for medical scheme contributions will increase to the following:

- R347 per month per beneficiary for the first two beneficiaries

- R234 per month for each additional beneficiary

Companies

The corporate income tax rate will reduce from 28% to 27% for years of assessment ending on or after 31 March 2023.

Capital gains tax (CGT)

The capital gains tax inclusion rate for individuals and special trusts remains at 40%, and for other taxpayers at 80%.

The annual exclusion for a capital gain or loss granted to individuals and special trusts remains at R40 000. The exclusion granted to individuals remains at R300 000 in the year of death.

Trusts

The income tax rates for trusts (other than special trusts) remains unchanged at 45%.

Interest exemptions

The local interest exemptions remain unchanged:

- The exemption on interest earned for individuals younger than 65 years remains R23 800 per annum.

- The exemption for individuals 65 years and older remains R34 500 per annum.

Foreign interest remains fully taxable.

Dividends tax

Dividends tax remains at 20% on dividends paid by resident and non-resident companies for shares listed on the JSE.

Foreign dividends received by individuals from foreign companies (shareholding of less than 10% in the foreign company) are taxable at a maximum effective rate of 20%.

Interest withholding tax for non-residents

Interest withholding tax remains at 15% on interest from a South African source payable to non-residents. Interest is exempt if payable by any sphere of the South African government, a bank or if the debt is listed on a recognised exchange.

Tax-free savings account

The annual cap on contributions to tax-free savings accounts remains at R36 000 from 1 March 2022, with the lifetime limit also remaining at R500 000.

Retirement lump sum taxation

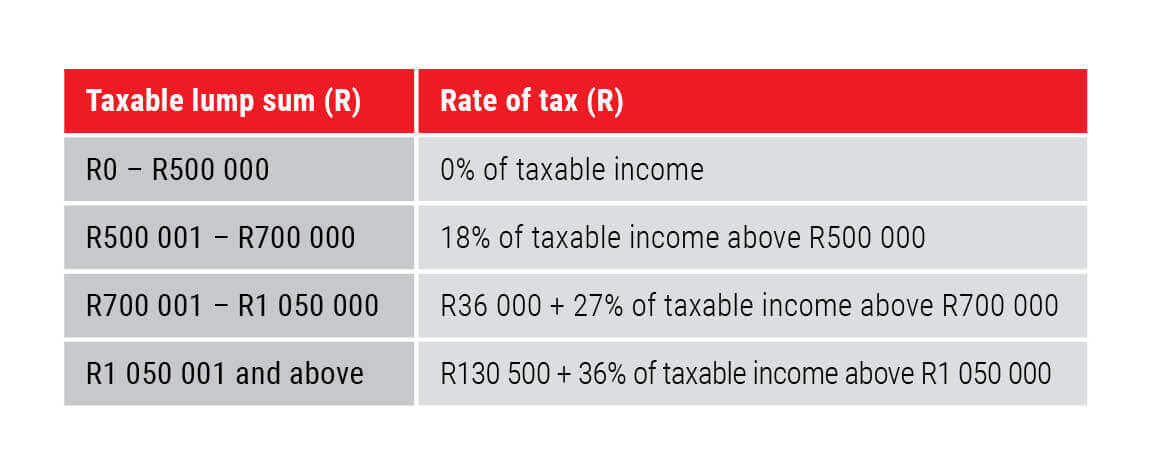

At retirement

The first R500 000 of a retirement lump sum remains tax-free. The table below illustrates how retirement lump sums will be taxed:

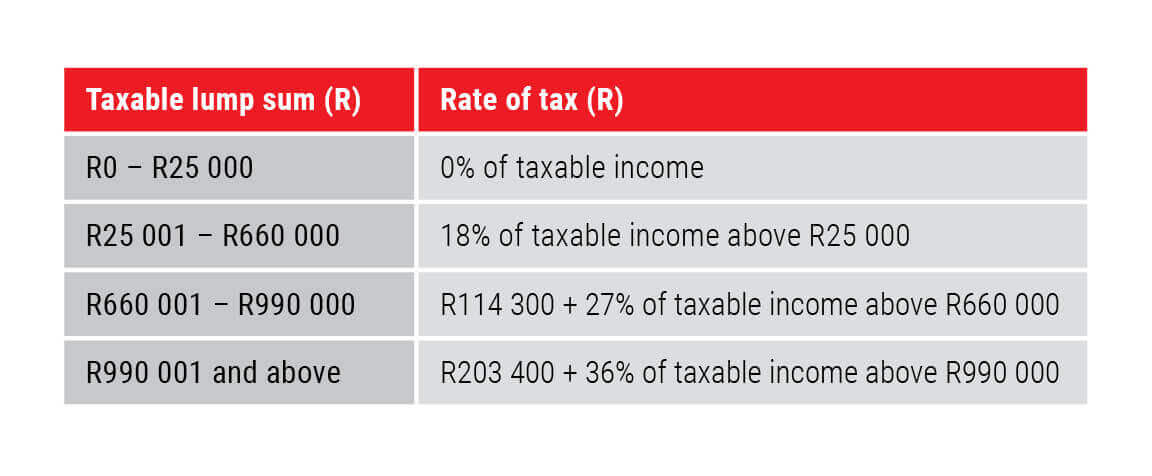

Pre-retirement

The first R25 000 of a pre-retirement lump sum withdrawal remains tax-free. The table below illustrates how withdrawal lump sums will be taxed:

Value-added tax (VAT)

VAT is charged on the supply of goods and services provided by registered vendors. It remains at 15%.

Estate duty

Estate duty is levied on property of residents and South African property of non-residents, less allowable deductions. The duty is levied on the dutiable value of an estate at a rate of 20% on the first R30 million and at a rate of 25% above R30 million.

A basic deduction of R3.5 million is allowed in the determination of an estate’s liability for estate duty.

Donations tax

Donations tax is payable at a flat rate on the value of property disposed of by donation. It is levied at a flat rate of 20% on the cumulative value of property donated since 1 March 2018 not exceeding R30 million, and at a rate of 25% on the cumulative value of property donated since 1 March 2018 exceeding R30 million.

The first R100 000 of property donated in each year by an individual is, however, exempt from donations tax. This amount remains unchanged from last year.

Additional tax proposals for the 2022 legislative cycle and beyond

Retirement fund provisions

Deemed exit tax on retirement fund interest on cessation of South African tax residency

Last year’s Budget announced proposed changes to impose a withdrawal tax and interest charge, with effect from 1 March 2022, when a member of a retirement fund ceases to be a South African tax resident. These changes were withdrawn from the 2021 legislative cycle, following concerns raised during public consultation on the 2021 Tax Bills. In order to address the complexities raised through the comment cycle, including the concern that the amendment would result in double-tax treaty override, government will start the process of renegotiating the affected tax treaties to ensure that South Africa retains taxing rights on payments from local retirement funds. Government intends to start these negotiations this year.

Retirement fund reform update (“two-pot system”)

Proposals are being worked on to allow members access to one-third of their retirement fund savings before retirement while the remaining two-thirds will need to be preserved for retirement. Public comments on the tax treatment of contributions to the two pots are being reviewed in preparation for public workshops, to be followed by legislative amendments.

Disclosure of wealth for provisional taxpayers and a review of the provisional tax system

Provisional taxpayers with assets above R50 million will be required to declare specified assets and liabilities at market value in their 2023 tax returns to assist with the detection of non-compliance and fraud. The additional information will assist in determining the levels and structure of wealth as recommended by the Davis Tax Committee.

Government proposes a review of the provisional tax system in line with international developments and intends to publish a discussion paper in this regard.