There has been little else to talk about as COVID-19 dominates world headlines. Globally, everyone is trying to evaluate the real impact the pandemic will have on their livelihoods and communities, and businesses are grappling with the true economic cost of the lockdowns. Uncertainty, a concept which we tend to avoid as we seek out comfort, is now front of mind. As asset managers, estimating the intrinsic value of a company requires us to accept that we are always weighing up probabilities about the future: Uncertainty will always be a part of investing and our contrarian approach. Nonetheless, we agree that today the range of outcomes has clearly widened. Radhesen Naidoo explains how our offshore partner Orbis is navigating this environment.

Performance update

Before talking about Orbis’ recent actions and views on the underlying businesses in the portfolios, it is important to address and provide context about our performance experienced in the first quarter of 2020. Going into the start of 2020, the Orbis funds were broadly overweight emerging markets and underweight the US, compared to their benchmarks. At a stock level, the funds were overweight more cyclical/volatile areas in the market and value stocks, and underweight growth stocks and safer/low volatility names. Towards the end of previous economic cycles or bull markets, safer shares tended to become more attractively priced as investors got too optimistic about cyclical areas. On this occasion, the “safe” shares led the market up. Faced with a difficult choice, we preferred to own cyclical stocks with earnings risk at low prices, rather than "safe" stocks, which we felt had valuation risk (and were not free of earnings risk). This positioning had been a headwind through much of 2018 and 2019, as (1) stocks with safe, predictable earnings had become more expensive, in our view, while those with more volatile/cyclical earnings appeared to have been unduly punished, (2) growth shares outperformed value and (3) US shares and large caps both led the market up.

These headwinds abated briefly (late 3Q19 to early 1Q20), and performance started to turn, but the headwinds have since reasserted strongly, as concerns about the COVID-19 pandemic have led to a further flight to safety in 2020. Stable stocks, which were already expensive, in our view, have held up better than the wider market thus far. To be specific, the fundamental impact on a business selling consumer goods needed during the lockdown has been positive, so it makes sense they have held up better. However, will these businesses continue in the same vein going forward? It seems unlikely, as people won’t require more toilet paper, food and other essentials today, than before the virus, indefinitely.

Conversely, stocks in the most cyclical parts of the market have been punished the most as their earnings are more sensitive to the immediate impacts. Energy stocks, in particular, have faced additional pressure, as oil prices have collapsed, driving a large portion of the underperformance experienced in the Orbis Global Balanced and Optimal SA funds. The Orbis Global Equity Fund has underperformed to a lesser degree, as the energy exposure is lower, and the higher exposure to emerging market shares, such as NetEase, has been beneficial, as these shares have held up given the consistent demand for services like online gaming.

In our view, valuation spreads globally are at fresh extremes following the recent market moves – an environment which piques our interest as valuation-driven investors. The dislocations noted above appear to have widened, such as volatility versus stability and value versus growth. We are therefore more excited by the relative value opportunity in our funds, than at the start of the year – when the outlook looked promising already. Given the fall in markets, we also believe that the outlook for absolute returns has improved.

Evaluating opportunities

During this period, the Orbis investment team has been reviewing the balance sheet strength and liquidity of the companies they own to assess the potential capital impairment risk from a prolonged economic slowdown. Analysts are also busy evaluating new opportunities that have arisen amid the extreme volatility, starting with our pipeline — companies that we know well, but which, until recently, have not been available at the right prices. Broadly, this can be categorised as buying the proverbial “babies being thrown out with the bathwater”. This has resulted in reducing exposure to shares which have held up better or outperformed (such as NetEase), and increasing our positions into businesses which have more stable fundamentals at lower prices (Comcast, British American Tobacco), and in existing cyclical businesses that we believe are more resilient to weather the downturn than people think (for example, BMW). Importantly, all these decisions are driven by the relationship between price and fundamentals – NetEase continues to be a top 10 holding and attractive to own relative to the broader market, but we’ve trimmed the position because discounts for other shares have widened so much more. Overall, this means that the funds today remain significantly cheaper than the benchmarks, but with improved fundamentals.

We also have stress-tested our largest holdings and, encouragingly, the majority have a low sensitivity to the impact of COVID-19. For example, the shares which are most sensitive include the auto companies (BMW and Honda), but they have strong balance sheets, and enough cash to fund themselves for the next 12 months, assuming they make zero sales. This makes their operations significantly more resilient than peers. XPO Logistics has been incredibly volatile, but the nature of the underlying business is less cyclical than the market believes and it is able to generate sufficient cash to comfortably cover debt servicing. In contrast, companies such as NetEase and Naspers could emerge stronger given their positions in their online businesses.

Reasons to believe

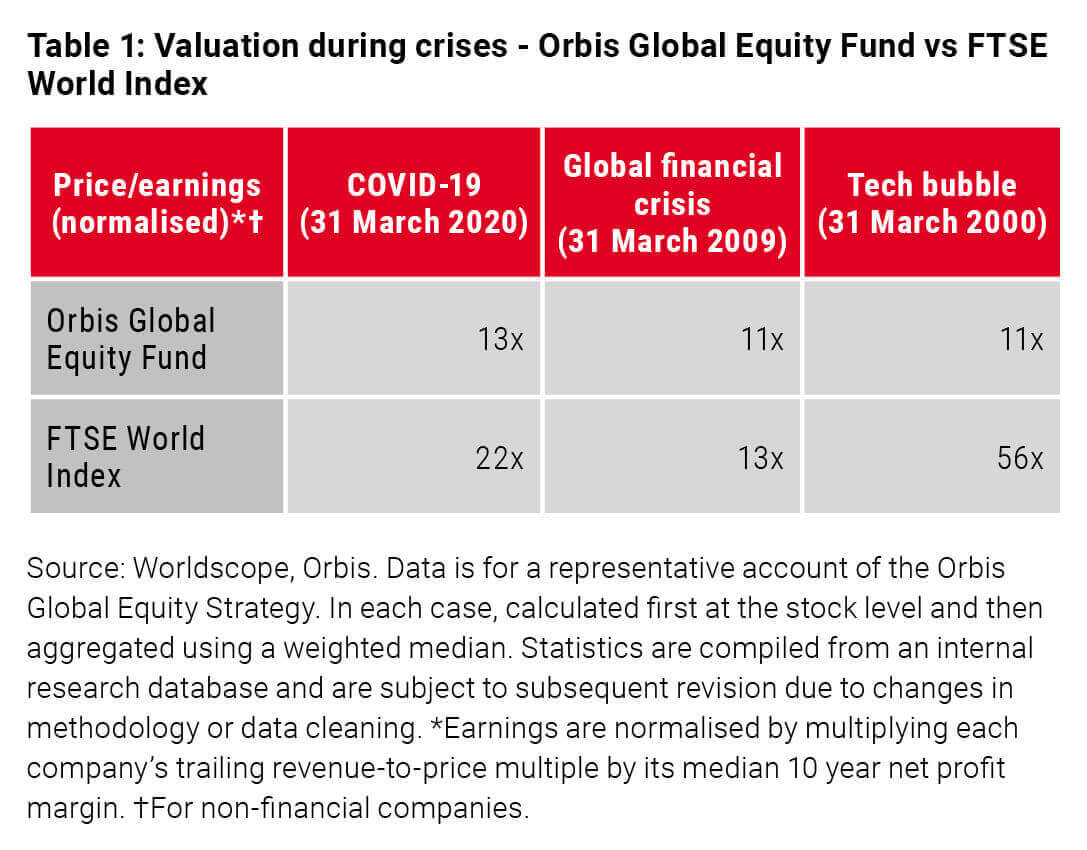

Clients today are understandably going to ask us why they should remain invested when markets have tumbled, remain incredibly volatile, and our performance has not improved. In short, the extreme pessimism of other investors creates rare opportunities for those who can remain disciplined. To provide further context, Table 1 compares the valuation of the Orbis Global Equity Fund to the FTSE World Index at previous extreme periods.

We are paying a similar valuation for the shares we own in the Orbis Global Equity Fund today as we did in previous crises, and the absolute return potential looks comparable. However, what is different is the alpha opportunity – after the global financial crisis (GFC), the entire market was cheaper and, perhaps unsurprisingly, the opportunity to outperform was limited. Leading into the GFC, value shares experienced the best period of performance compared to growth. Today, the overall market is more expensive, driven by the exact opposite, as growth shares have crushed value over the past decade. While not as extreme as in 2000, the opportunity to outperform from here is very attractive, in our view.

Many investors have pronounced ”the death of value investing” over the past few years but we take comfort in knowing that all investment factors operate in cycles. While it may have taken a decade to approach this point, one could venture that it doesn’t take a decade to unwind – just like how markets build up and suddenly crash. Ignoring the factors, we would remind our clients that we own a collection of businesses that already trade at a fraction of what we believe they are worth: No matter what happens, it’s always the price you pay today that is the key determinant of future returns.

We appreciate that this has been a challenging time for our clients, but we are increasingly excited by the value that we believe is embedded in our funds at today’s prices. While the uncertainty may persist for some time, this creates opportunity, and typically clients who have remained invested through these periods have shared in the rewards.