Over multiple decades, the traditional value approach of buying cheap stocks has worked remarkably well. Over the last decade, it hasn’t, leading an increasingly large chorus to proclaim that value investing is dead. Is there truth to these words? Brett Moshal and Michael Heap from our offshore partner, Orbis, discuss this below. You can also watch this 3-minute video for additional insights.

While we aren’t textbook value investors, the debate about value investing is not academic for us, as the value philosophy and our fundamental, long-term, and contrarian philosophy are intellectual cousins. Value investing has taken knocks before and recovered – can it do so once again?

To cut to the chase, our answer is an emphatic yes. It will work in future for the same reason that it has worked so well over the long-term past: At its core, its efficacy is driven by thousands of years of basic human nature, specifically the survival instinct that causes humans to respond to greed and fear. These primal drives lead investors to run with winners and from losers. In markets, investors habitually expect the winners to forever thrive and the losers to forever struggle, and they price the companies accordingly. History has shown that investors tend to overshoot. Growth fades and struggles subside. Whether through the power of incentives, the levelling gravity of capitalism, or even luck, great and bad companies alike often prove their adjectives wrong.

That pattern hasn’t worked over the past 12 years, in part because in 2007, the cheap stocks weren’t very cheap. But the doubts currently circulating have little to do with valuations 12 years ago. Instead, investors are becoming convinced that expensive shares will carry on beating cheap shares indefinitely.

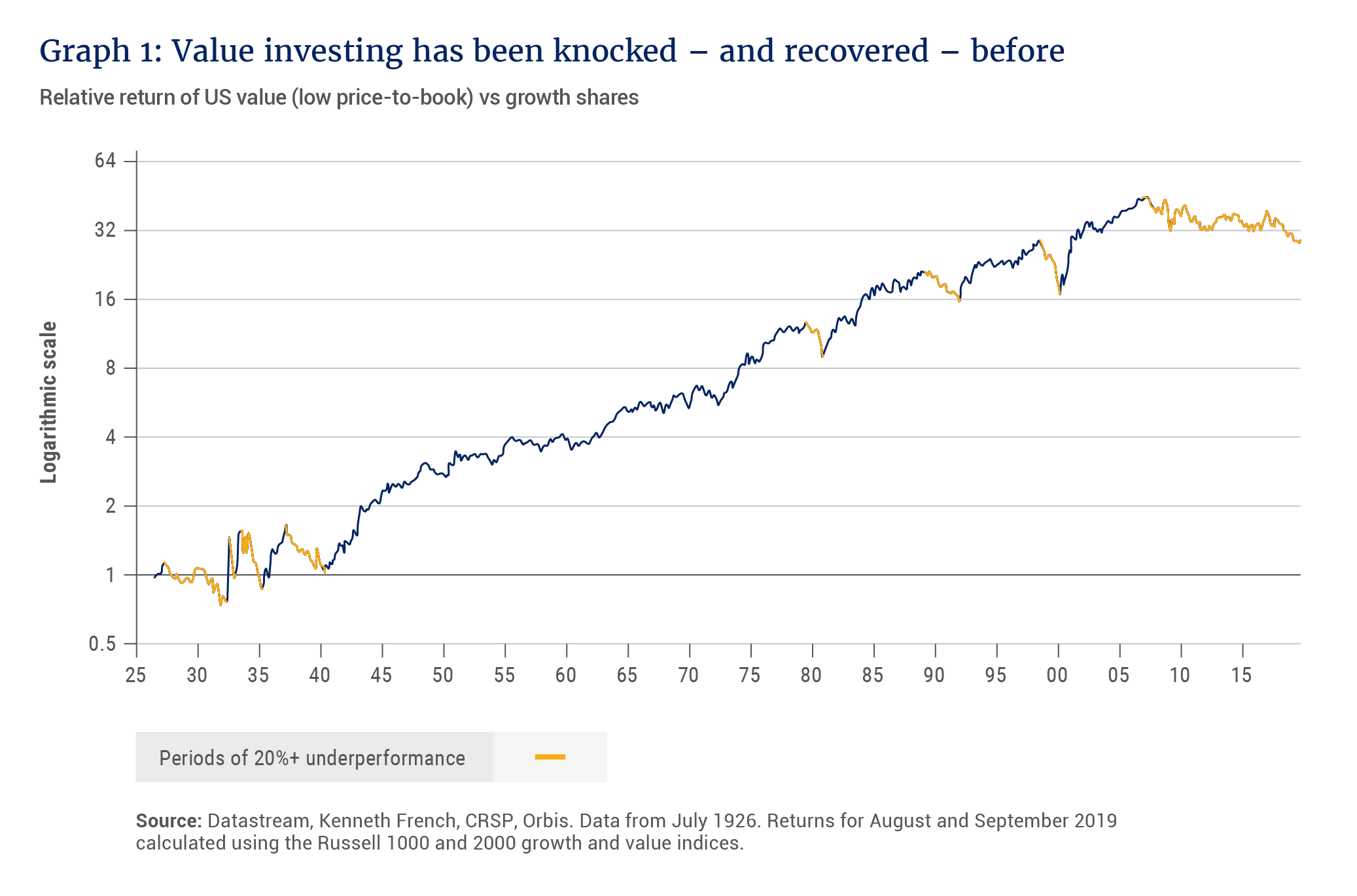

This is a necessary step. For value opportunities to emerge, investors first have to overestimate the differences between companies. Widening expectations are as essential to value investing as exhaling is to breathing. That does not make periods of widening expectations any more comfortable, however. As Graph 1 shows, in the 80 years from 1926 to 2006, value shares experienced seven periods of 20%+ underperformance vs expensive shares. The good news? Every one of those periods was followed by significantly better-than-average outperformance for value.

Is it different this time?

Yet this long historical perspective hasn’t stopped investors from claiming that this time is different, whether because of technological change, falling interest rates, changing valuation metrics, or even the very awareness of value investing. This questioning, of course, is a condition of value investing’s success, not a proof of its failure.

We don’t believe this time is different, and we believe value investing and the underlying psychology that drives it remain valid. More importantly, we remain as convinced as ever that our fundamental, long-term, and contrarian approach is sound, and as co-investors in the Orbis funds, it is how we’re investing our own money.

The technological developments of the 21st century are impressive, but they have not been better for economic productivity than the major technological advances of the 20th century – a period when value shares outperformed. Social media and e-commerce are significant innovations, but so, too, were the telephone, radio, car, television and electricity. And while low interest rates have recently been correlated with poor returns for value shares, those shares handily outperformed from the early 1980s to 2006, even as 10-year US yields fell from double digits to below 5% per annum.

we believe value investing and the underlying psychology that drives it remain valid

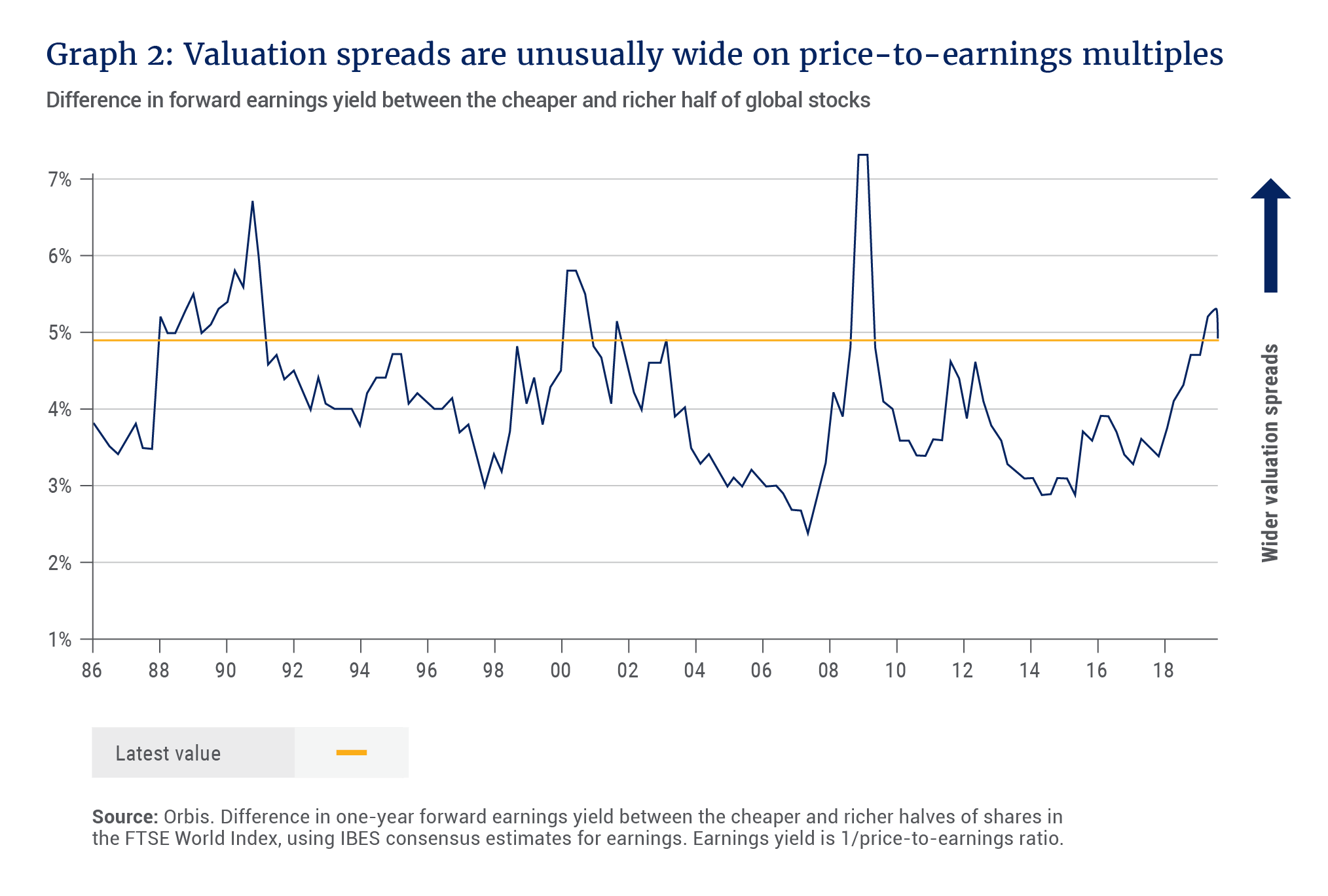

Finally, if awareness of value investing closed all the discounts in the market, you would expect to see muted differences between the valuations of cheap and expensive companies. Yet valuation spreads today are unusually wide. That’s true whether you look at the classic price-to-book multiple, or at other measures such as price-to-earnings (see Graph 2). Over the past 30+ years, the valuation gap below has only been wider around the Japan bubble in 1990, the tech bubble in 2000, and at the trough of the global financial crisis. On each of those occasions, the “value investing is dead” refrain was heard far and wide.

Although valuation spreads are wide, not all of our favourite ideas are trading at depressed multiples. We’re flexible, and we’re happy to own shares trading at higher “headline” price multiples, so long as the business trades at a sufficiently attractive discount to our estimate of its true worth.

In the US and emerging markets, for instance, many of our favourite ideas are stocks that we believe offer idiosyncratic and underappreciated growth potential at a reasonable price. In the US, these include XPO Logistics, Facebook, Anthem, Alphabet, and S&P Global, and in emerging markets, NetEase, Autohome, and Taiwan Semiconductor Manufacturing Company.

In Europe and Japan, however, it’s a different story – many of the most compelling ideas we’ve found there trade at very low valuations. In aggregate, the Orbis Global Equity Strategy’s holdings in developed Europe trade at just 1.0 times book value, and in Japan, just 0.8 times. This is despite fundamentals that are on a par with or slightly better than local averages.

Two examples provide a good illustration of these attractive opportunities: BMW in Europe and trading companies in Japan are quintessential value stocks.

European value: BMW

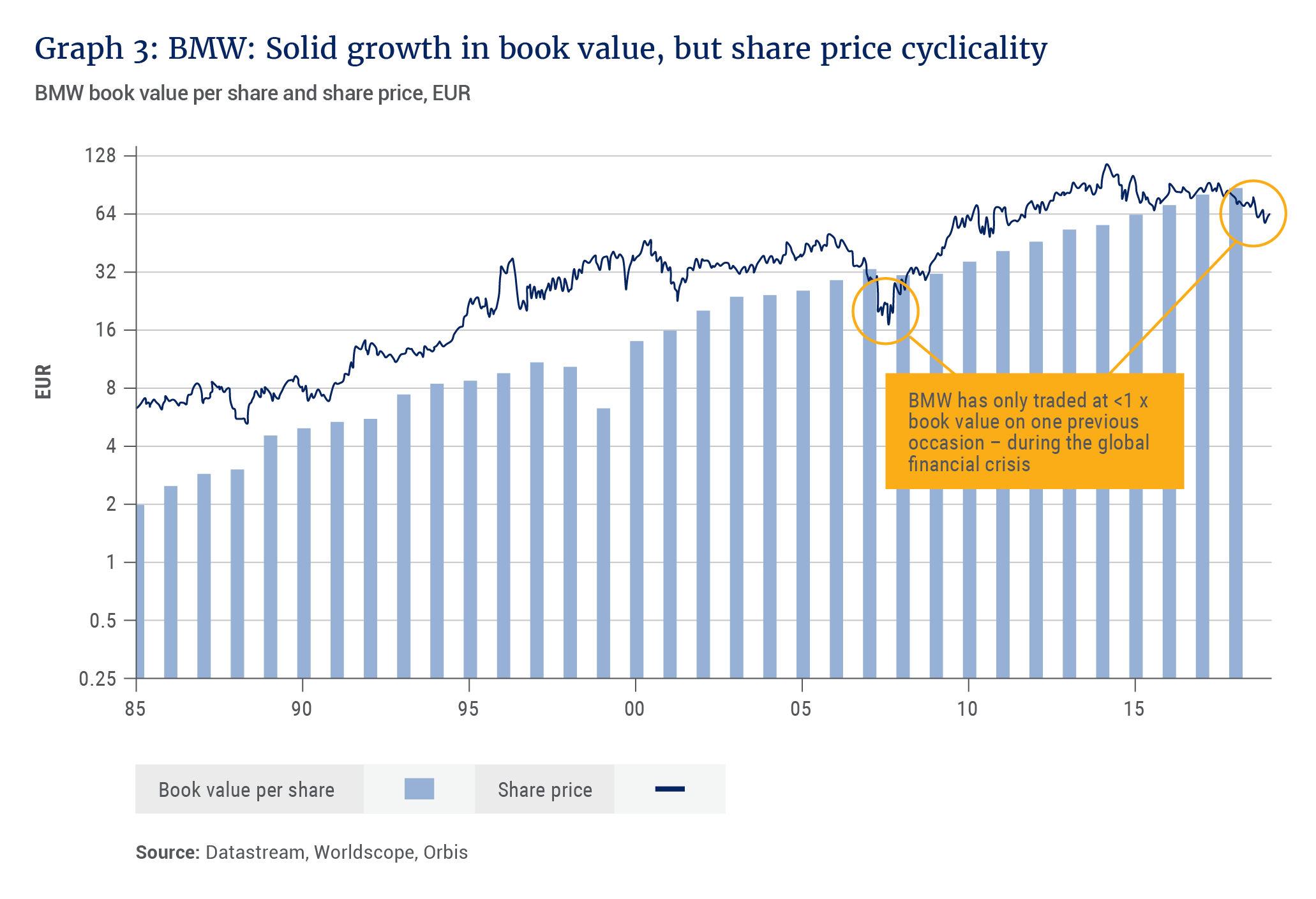

Last quarter we discussed Honda Motor, which is trading near an all-time low (even worse than during the financial crisis) valuation due to concerns about the global auto industry. Trading at 0.8 times book value and just six times depressed 2018 earnings, BMW is in the same boat.

The automotive sector does face some challenges. The sales cycle globally has been getting worse, particularly in China, and the industry faces an uncertain future as governments, particularly in Europe, push hard to promote electric vehicles. However, over the long term, we believe these risks are unlikely to be anywhere near as severe as implied by BMW’s share price.

While the cycle in China has been painful, in cyclical companies it often pays to invest when the outlook is uncertain, so long as the valuation more than accounts for the risk. If you wait until the outlook is clearly improving, that improvement is obvious to everyone else too, and will be reflected in a higher stock price.

Globally, the push for battery electric vehicles (BEVs) is a headwind to automakers’ profits, as governments in many markets set requirements for BEVs as a share of an automaker’s sales. Customer demand, however, is not yet high enough to allow manufacturers to sell BEVs at prices that generate sustainable profits. As a result, the automakers generally lose money on each one they have to sell.

While this is challenging over the short term, we don’t think it is an accurate picture of the industry’s future. When a capital-intensive industry faces low returns, prices generally rise until the industry makes a sufficient return to cover its reinvestment needs. Over the medium term, we therefore think it’s more likely that consumers, rather than manufacturers, will pay the cost of reducing emissions via higher prices. Premium brands like BMW appear particularly well placed to pass on this pricing, given a wealthier customer base.

Across industries, companies with prestigious brands earn higher margins and returns on equity, because customers are willing and able to pay up for their products. Think of a tie rack at a clothes store – a Hermès tie will always be able to command a higher price than one from a no-name brand.

The same is true of cars, and this competitive advantage shows up in BMW’s financials. Over the long term, it has earned a roughly 15% return on equity and grown book value by 11% per annum while paying out a third of earnings as dividends – better results than the wider industry.

Yet due to industry pessimism, BMW today trades at just 0.8 times book value and six times depressed 2018 earnings, compared to 2.4 times and 21 times for the wider European market (see Graph 3). In any other sector, a luxury brand with a century-long pedigree and peer-leading financial returns would likely trade at a premium to the market. We believe a rerating to just 1.1 times book value, coupled with modest growth and a well-covered 5.5% dividend yield, could drive very attractive returns for BMW shares over our investment horizon.

Japanese value: Mitsubishi, Sumitomo and Mitsui

Part of our concentration in Japanese value shares is in Honda, which we discussed last quarter. But the biggest exposure is to a different kind of company – Japan’s trading companies, including Mitsubishi, Sumitomo and Mitsui & Co.

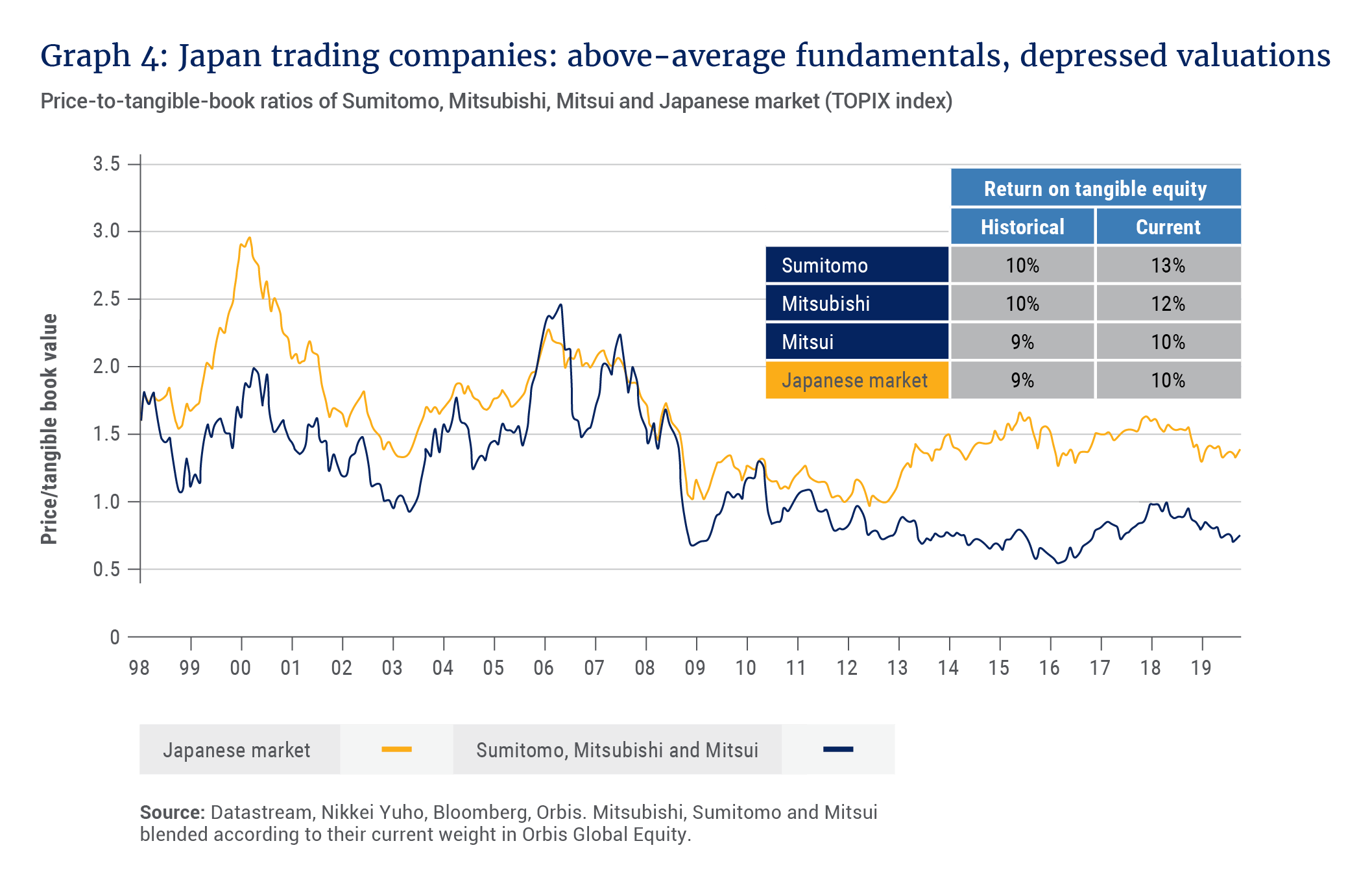

General trading companies are best thought of as industrial conglomerates. Their subsidiaries deal in businesses as diverse as natural gas, coking coal, nickel mining, oil pipes, power plants, food distributors, salmon fisheries, cable operators and convenience stores. In effect, the companies are so diversified that their fundamentals unsurprisingly tend to track those of the Japanese economy as a whole. For most of their history, the companies generated roughly average returns on equity, and were appropriately assigned roughly average valuations.

we believe time will prove that today’s reports of the death of value investing were… greatly exaggerated

In 2013, however, the market was concerned about the companies’ resource businesses, leading the stocks to trade at a discount to their book value despite generating higher returns on equity than the average Japanese company (see Graph 4). We bought positions in Mitsubishi and Sumitomo for the Orbis Global Equity Fund in 2013, adding Mitsui later. Our thesis was that their assets would generate reasonable, sustainable profits, and that improvement in capital allocation could drive a rerating and attractive returns for shareholders.

On the asset side, there have been hiccups. Amid the commodity crash from 2014 to 2016, the companies took write-downs, leading to Sumitomo’s first annual loss in 15 years, and Mitsubishi and Mitsui’s first losses in over 40 years. Since then, however, commodity prices have recovered, and the companies’ biggest commodity segments have returned to generating profits and cash flow.

Perhaps more importantly, the companies have also become better at allocating that cash flow. Having previously spent freely on investments, they are now divesting assets with low returns, investing more carefully in new projects, paying down debt, and making higher payouts to shareholders through dividends and buybacks. From almost any angle, the businesses are in better shape now than they were five years ago.

Yet that improvement has not been rewarded with appropriately higher valuations. Today, all three companies trade at a discount to their book value and just seven times earnings, with dividend yields above 4%, despite earning higher returns on equity than the broader Japanese market. To us, that looks like a substantial discount to the companies’ intrinsic value. From here, simply generating cash and growing book value would deliver reasonable returns, with any rerating providing additional upside for shareholders.

Focusing on intrinsic value

In today’s market environment, valuation spreads look unusually wide, and we have uncovered a number of attractive value shares, particularly in Europe and Japan. As ever, there is no guarantee that the market will come to share our view of these businesses. But importantly, we don’t own the stocks just because they’re cheap. We own them because we believe their low valuations are unwarranted. With opportunities like these on offer, we believe time will prove that today’s reports of the death of value investing were – once again – greatly exaggerated.