How much is enough to save for a comfortable retirement? Wanita Isaacs unpacks the concepts of ‘enough’ and ‘comfortable’ in the context of this distant, unpredictable goal.

Rules of thumb for a comfortable versus sustainable retirement income

Behavioural scientists explain that we base most of our actions on mental shortcuts, learned through our own past experience or through commonly held beliefs: we use ‘rules of thumb’.

A well-researched rule of thumb is that a retirement income equal to 75% of your final salary just before you retire will allow you to live comfortably in retirement. This figure accounts for the adjustments many people make as they age, for example, lower housing and higher medical costs.

We have written previously about a rule of thumb for ensuring a sustainable income during retirement. Based on the findings of US author and financial adviser William Bengen, and our own research, we found that if you structure your portfolio appropriately and draw a rand-based (rather than percentage-based) income that amounts to 4% of your savings at retirement, and only increase your rand amount in line with inflation each year, there is a high likelihood that your income could last for at least 30 years (see Michael Summerton’s piece in Quarterly Commentary 2, 2014).

Not all widely held beliefs are good rules of thumb

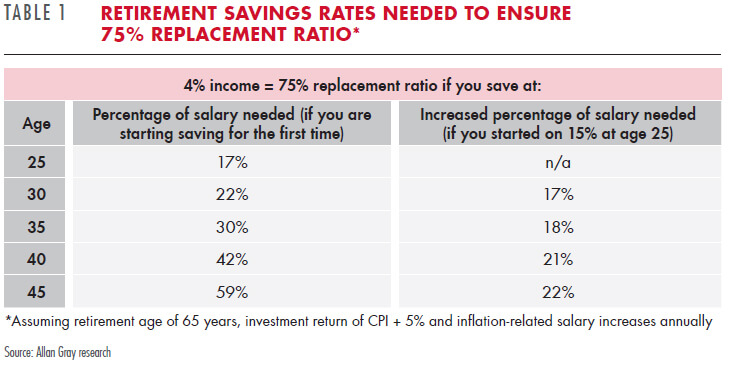

The government incentivises us to save for retirement in approved retirement funds, rewarding us with tax breaks. An example of an unintended rule of thumb is using the tax-break maximum as a guide for how much is an appropriate amount to save. For years many people have used the previous maximum tax-break of 15% as a savings benchmark, which is too low to reach the recommended 75% income replacement.

This might explain why many of our living annuitants, and their financial advisers, report that 4% of their investment is not enough to fund their lifestyles. Our client research indicates that the majority of retirees already take a conservative approach to their spending, which suggests that they simply have not saved enough.

How much do you need to save for 4% to be a comfortable retirement income?

Assuming that you will be comfortable living off 75% of your pre-retirement salary, the first column in Table 1 shows the percentage of current salary that individuals at different ages would need to invest when starting to save for retirement for the first time. The table shows that even for a 25-year old, investing 15% of taxable income is not enough to ensure a sustainable and comfortable retirement. A safer rule of thumb is to invest at least 17%.

For those of us who started saving for retirement early and have been resting in the false security of investing the previous ‘maximum’ of 15% of our salaries, the second column shows the level to which we would need to increase our percentage of salary in order to catch up.

The new maximum tax-break of 27.5%, which came into force on 1 March 2016, is a much better benchmark, but it is still important to look at your personal needs to assess how much you should save.

Rules of thumb do not account for personal circumstances

The numbers in Table 1 are simply averages and it is important that you take your personal circumstances into account. This percentage of salary rule of thumb assumes a consistent, inflationary salary increase each year. This won’t work for you if your personal inflation rate is higher than the published inflation rate (which reflects the general rise in the cost of goods and services). Your personal inflation rate rises each time you improve your lifestyle, for example moving to a bigger, more expensive house.

A spike in salary affords you those lifestyle improvements, but may set you back in your provision for retirement if you don’t shift your retirement savings goalposts appropriately and allocate some of the extra cash to the future. Continuing to invest at the same percentage of your new salary won’t be enough. This is because everything you invested before your salary increase accounted for your previous lifestyle; you will need to make up for the shortfall if you want your retirement income to fund your current lifestyle at that time.

“MOST OF US HAVE CONFLICTING PRIORITIES WHEN IT COMES TO AFFORDING OUR CURRENT LIFESTYLE AND SAVING FOR OUR FUTURE”

Three levers to pull to increase your retirement savings pot

Most of us have conflicting priorities when it comes to affording our current lifestyle and saving for our future. If you can’t currently afford to increase your retirement savings, there are three levers to pull:

1. Prioritise your retirement savings when you get additional income. Consider either splitting each individual income boost, or alternate between improving your current lifestyle and increasing your retirement savings.

2. Delay retirement to give your investment more time to grow, both through your contributions and return on your investment.

3. Decrease your income needs in retirement by re-thinking your lifestyle priorities.

Also, remember that there are various ways you can supplement your retirement savings. It makes sense to use the tax break the government provides in approved retirement funds, such as your employer’s retirement fund or an RA, but thinking this is the only way you can save for your retirement is another unintended, and potentially disadvantageous, rule of thumb.

You may want to consider saving in other products, such as a tax-free investment account or a basic unit trust, which give you more flexibility in terms of investment choice and access to your investment. And any paid-off assets you own, such as your house, contribute towards your retirement by decreasing your financial needs, or increasing your income in retirement.

A comfortable retirement takes careful planning

While we inherently look for mental shortcuts to make sense of the complexity of life, problems arise when we follow rules of thumb blindly. It often feels easy to take a mental shortcut when it comes to your income at retirement, but it may be better to get advice from a good, independent financial adviser. At the very least, thoroughly research and plan your next steps making sure that the shortcuts you choose to take are prudent.