In a world where instant gratification is king, it can be hard not to get distracted by the lure of short-term gains. But taking a long-term view of your investments and staying the course can give you the edge to achieve better investment returns over time. Thandi Skade explores the opportunity cost of failing to stick to your long-term investment plan and how you can avoid paying behavioural penalties.

It is often said that investing is a game of patience. Like in chess, the best moves are often the ones that require discipline and playing the long game. In some ways, staying the course can be seen as a checkmate move: You “win” by remaining committed to your long-term investment strategy, effectively blocking the common behavioural pitfalls that can lead to inferior investment performance.

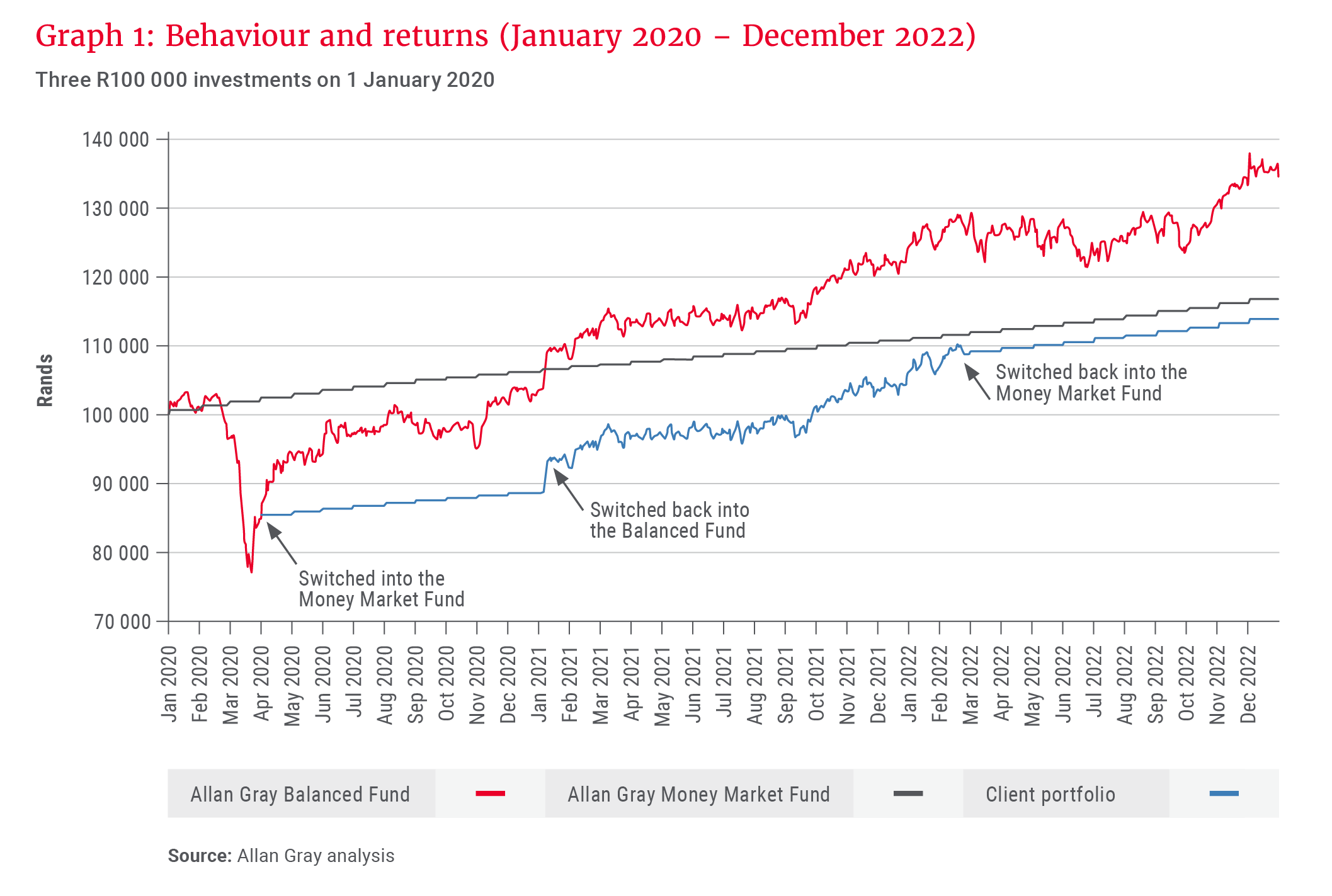

One of the mistakes many investors make is switching between funds or making withdrawals in an emotional response to short-term market movements. This can erode returns over time, as illustrated in Graph 1, which shows behaviour and resultant returns in three hypothetical investment scenarios. In all the scenarios, we measured the performance of a R100 000 investment initiated in January 2020 over the period to December 2022.

Staying invested allows you to reap the rewards of compound interest …

The first scenario represents the investor who stayed invested in the Allan Gray Balanced Fund over the entire period. The second scenario represents an investment in the Allan Gray Money Market Fund over the duration of the period, and the third represents the investor who attempted to time the market and made multiple switches between the funds in reaction to market volatility, which was driven by the start of the pandemic in March 2020 and Russia’s invasion of Ukraine in late February last year. The difference in outcomes is notable.

Although measured over a relatively short period of time compared to the average investment horizon, Graph 1 reinforces the point that you will likely earn higher returns by remaining consistently invested over time, whether it is in a low- or medium-risk investment. Staying invested allows you to reap the rewards of compound interest – gaining additional returns on the returns already earned from your investments over time. By selling off investments or switching between funds, we limit the compounding effect and growth potential of our investments.

Key to enjoying long-term investing success is ensuring that we keep our emotions in check and remain invested.

While you could argue that we have engineered scenario three to illustrate our point, this type of behaviour and outcome is very common. In fact, behavioural economists have a term for it: The “behaviour gap” refers to the difference between the long-term returns delivered by a fund and the return an individual investor earns; a gap widened by poor behaviour, particularly trying to time the perfect entrance to and exit from the market (which often leads to buying high and selling low).

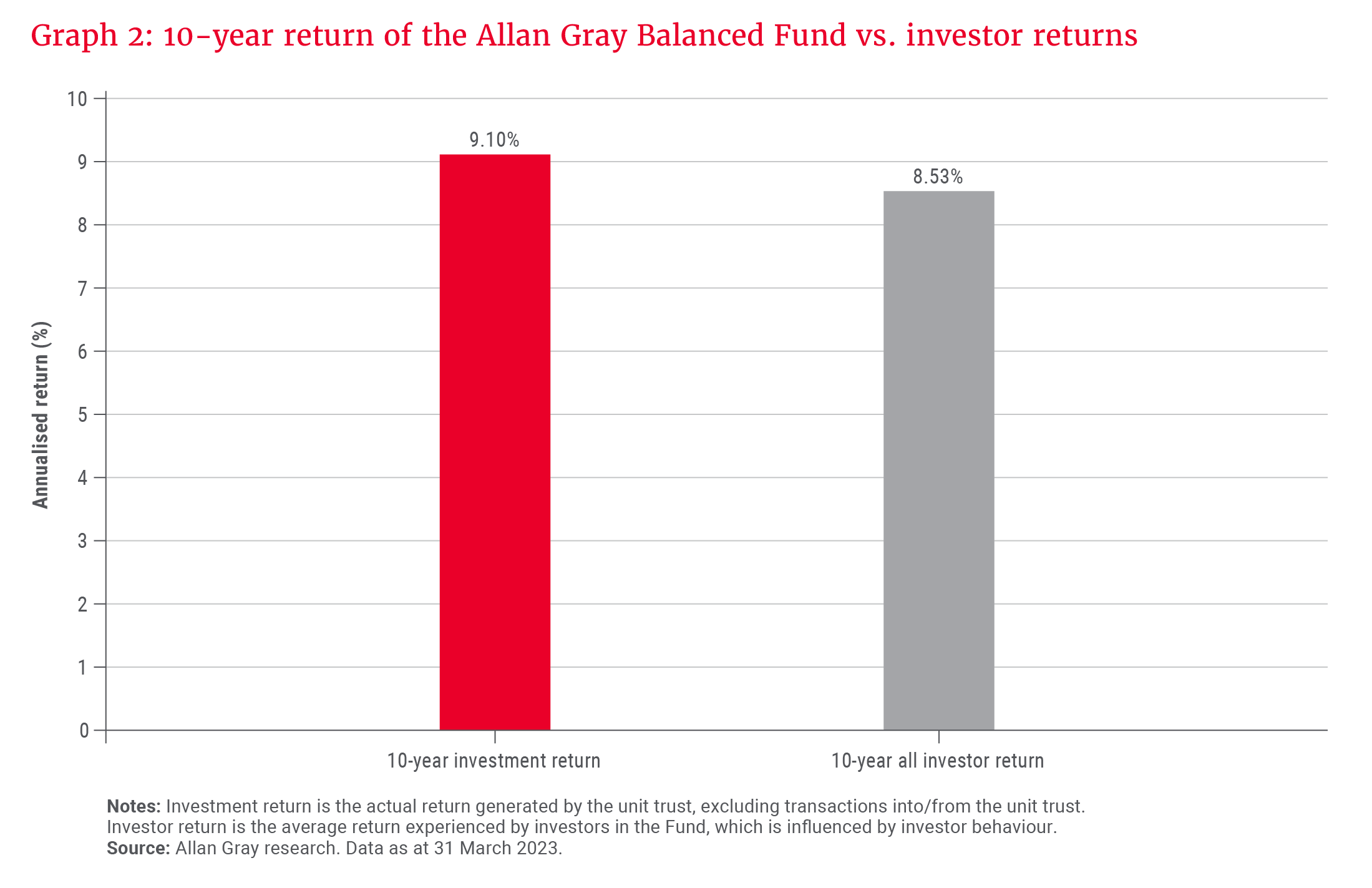

Graph 2 shows the 10-year return of the Allan Gray Balanced Fund – which is the return an investor would earn over the period by staying invested – compared to our clients’ investment returns. It highlights that, on average, our clients locked in a 0.57% investor behaviour penalty over the period. That may not seem like a big difference, but over time, these small differences compound and can have a significant impact, as Radhesen Naidoo discusses in his piece. Key to enjoying long-term investing success is ensuring that we keep our emotions in check and remain invested.

You don’t have to go at it alone

While some investors can construct their own financial plans and portfolios and are able to stay the course over the long term, many find these activities and behaviours challenging and could benefit from partnering with a good independent financial adviser (IFA). An IFA can put together a plan based on your long-term goals and should review your investment portfolio annually to ensure that it continues to appropriately meet your needs.

Investors cite the cost of financial advice as the biggest deterrent to seeking professional guidance. However, what is often overlooked are the subtle and less tangible ways in which financial advisers create value for their clients over time. While it is hard to quantify the cost of not receiving advice, it can perhaps be measured by the penalties incurred through poor investor behaviour – which an IFA can help you avoid (see below).

Independent financial advisers (IFAs) can help investors avoid the pitfalls of investing on their own. While some investors may not need an IFA to help them achieve this, it pays to be aware of how to avoid these common mistakes:

Attempting to time the market

During times of volatility, many investors struggle to tune out the noise, opting to switch out of higher-risk assets into lower-risk assets, like money market and interest-bearing funds. Switching between investments at the wrong time can lock in losses and prevent you from enjoying any future turnaround. An IFA can serve as a “voice of reason”, helping you to be rational rather than emotional and encouraging you to stay the course.

Not accounting for inflation

Money loses value over time. If your investments aren’t delivering inflation-beating returns, you will lose purchasing power in the long term. An IFA can make sure your money is invested in the right assets.

Not preserving retirement savings when changing jobs

Failing to preserve retirement savings exposes you to the risk of falling short during your retirement years. An IFA can guide you through the available options to preserve and grow your investment.

Failing to diversify

An IFA will make sure that your investment portfolio is adequately diversified to balance your risk and return requirements, and that you make adjustments at important life stages and milestones.

A good example of this is evidenced in the contribution and debit order behaviour of our advised and non-advised client base. An analysis of the database over a 10-year period revealed that our advised clients tend to make more regular contributions towards their investment accounts and remain invested for longer than non-advised investors across all our investment products.

This pattern was repeated among clients who pause and restart contributions to their investments: The data shows that advised clients reinstating debit order instructions make contributions for seven months longer than non-advised clients before their first debit order contribution freezes.

Over and above financial planning expertise and behavioural coaching, an IFA also provides estate-planning and comprehensive tax advisory services to help you structure your investment portfolio in the most tax-efficient manner.

So where do you begin if you are keen to partner with an IFA on your investment journey?

Trust is fundamental in choosing a financial adviser and maintaining a prosperous relationship with them over the long term. A good place to start is by asking people you trust, and whose judgement you value, for recommendations. You can also make use of our Find an independent financial adviser service, or have an adviser’s certification verified by the Financial Sector Conduct Authority (FSCA).

Asking the right questions, such as those suggested below, is a great way to gain insights that can help you determine the best fit.

Are you licensed?

Financial advisers in South Africa must be licensed as an authorised financial services provider by the Financial Sector Conduct Authority (FSCA).

Are you independent?

Not all advisers are equal. Some advisers are restricted to specific or limited product providers. The broader the range of product providers your adviser works with, the more options you will have to achieve all your financial goals.

What credentials do you hold?

As with any professional partnership, it is important to complete due diligence on a prospective adviser. Interrogate the letter of introduction that you will need to sign before you receive financial advice. Check that it contains the name and registration number of the adviser, whether they have professional indemnity insurance, and the categories of business on which the adviser is qualified to give advice.

How can you help me grow my wealth?

It is important to ask questions about both the nature of the adviser’s advice and their investment process to make sure these align with your needs and expectations.

How are your fees structured?

Transparency about how the adviser calculates their fee is critical. It is important to know upfront for what you will be expected to pay.

Consistency and patience are key

Winning a game of chess requires more than just making the right moves – you have to go into the game with a well-thought-out strategy, and stick to it. The same is true for investing. Being a successful long-term investor begins with determining what you want to achieve, then putting a plan in place to help you get there, and having the patience and conviction to stick to the plan.

At times along your investment journey, and particularly in the face of short-term underperformance or market volatility, you may need to sacrifice gains in the short term in exchange for more rewarding returns over the long term. This can be a lot easier said than done, though, so if you need an accountability partner, a financial adviser will be there to lend a hand.