The recent pandemic threw the South African banking sector a curveball, causing prices to tumble and creating new opportunities for patient, long-term investors. Siphesihle Zwane discusses the green shoots emerging at Nedbank and explains why they may reward investors who have enough conviction to stay the course.

Banks have a highly geared business model, taking in clients’ deposits and lending them out with little equity relative to the size of the lending. Periods of economic stress bring the quality of lending to the fore, and present opportunities to apply our long-term-orientated, valuation-focused process to invest in banks at a discount to our assessment of fair value.

Nedbank is the largest funder in the local commercial property market, funding the purchase and development of malls, offices and warehouses. The pandemic triggered lockdown restrictions on trading and a shift towards a greater number of employees working from home. These developments have deeply impacted Nedbank’s clients, creating the perception of heightened risk compared to the rest of the banking industry.

As valuation-focused investors, we look for companies where market expectations mirror recent trends despite evidence of green shoots.

While the risks to Nedbank’s balance sheet have increased over the last two years, we believe the business should be able to handle them, in most scenarios, with improving results from its retail bank providing additional upside.

Assessing commercial property balance sheet risks

When assessing balance sheet risks of commercial property lending, we consider the risk of non-payment, the quality of the assets backing the lending, and what larger-than-normal credit losses would mean for the overall business. In the case of Nedbank, the following risks remain well covered:

- Liquidity constraints: While the sharp restrictions in 2020 could have created a liquidity crunch, swift reaction from the South African Reserve Bank (SARB) in the form of lowering the benchmark interest rate by 300 basis points and loosening capital and liquidity requirements gave banks and businesses the ability to better handle lower cash flows. At peak restrictions, collections from tenants fell to 67% in April 2020, with listed property funds’ pre-interest earnings able to cover 2x the interest due.

- Asset losses: The portfolio’s loan-to-value ratio is 53%, which means the assets can lose more than half of their value before the bank makes a loss on collateral at a portfolio level.

- Capital requirements: Post-global financial crisis (GFC) regulations have meant banks hold more capital. This capital acts as a cushion against balance sheet shocks. At current levels, credit impairments as a percentage of lending would have to be more than 1.8x the COVID-19 peak and almost 2x the GFC highs for the business to wipe out all capital in excess of the SARB’s minimum requirements.

The overall property market

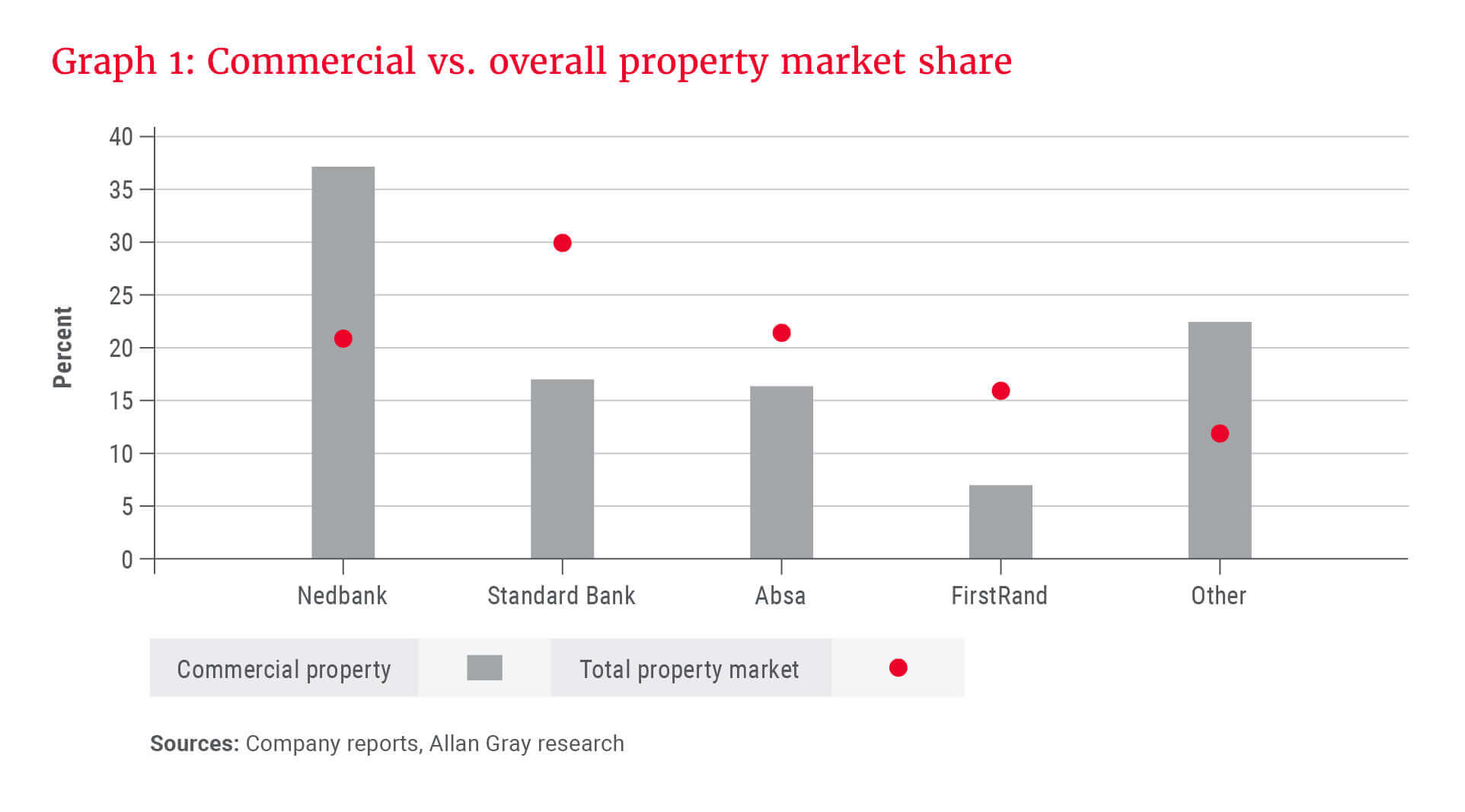

The overall property financing market is large, with Nedbank carrying a greater share of the commercial space, and a lower share of the overall market including home loans, as seen in Graph 1. It is not obvious that commercial property is riskier than residential property, with the latter experiencing higher economic sensitivity.

Currently, Nedbank’s average home loan balance is 79% of property values, compared to 53% in commercial financing. The typical new home loan is currently made at more than 90% loan-to-value, meaning that clients contribute less than R10 for every R100 of the home’s value.

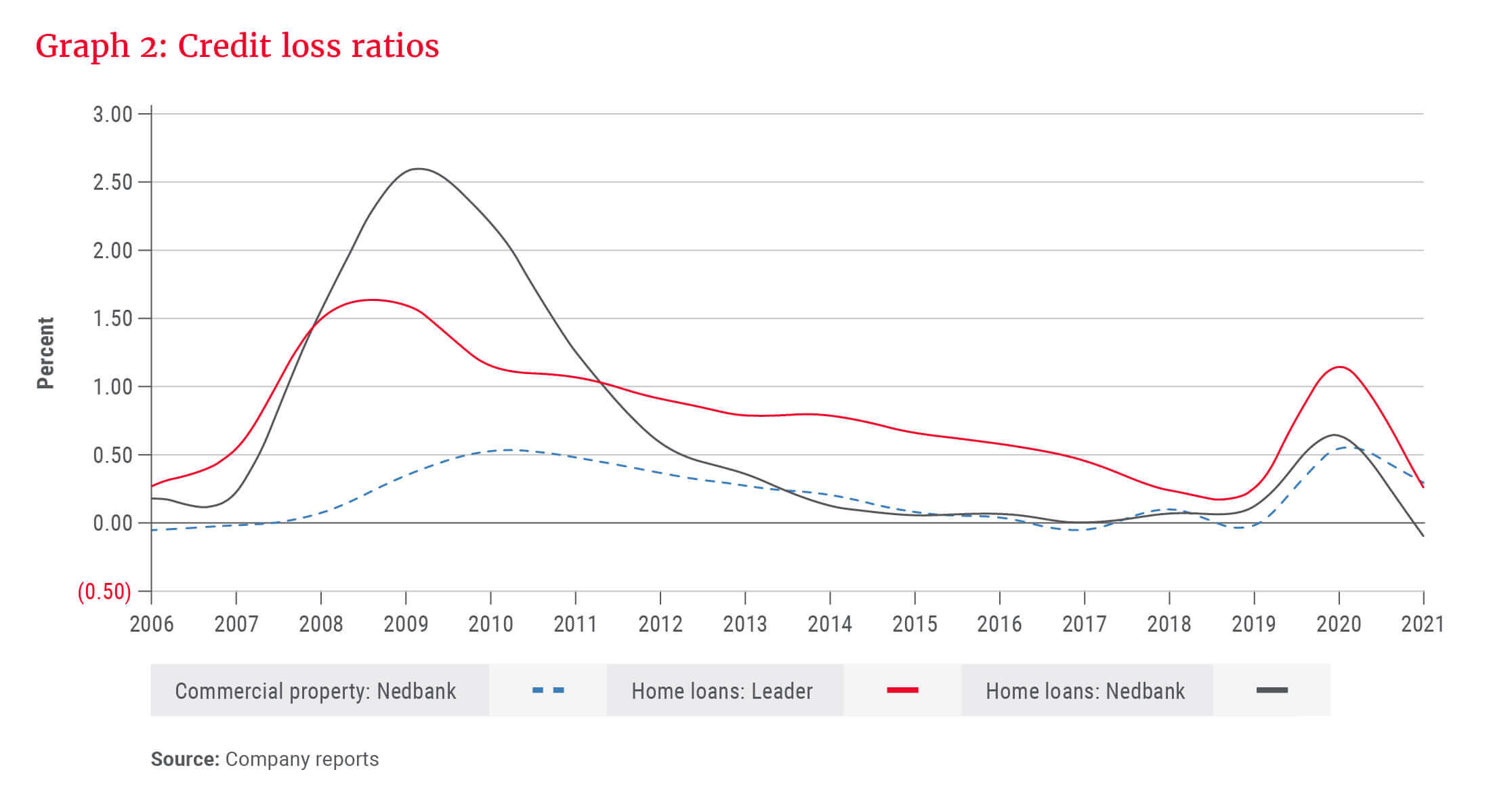

Annual expected losses from lending (defaults) are deducted from earnings in the form of credit impairments. Graph 2 shows the cost of defaults, expressed as a percentage of the overall lending book. The high degree of asset protection has meant that the cost of risk in Nedbank’s commercial lending has been less than 0.6% of the book over the last 15 years, with home loans having a more extreme experience over both the GFC and COVID-19 lockdown periods. Commercial property tends to lag the economy given the contractual nature of leases, giving both landlords and lenders more time to prepare for possible losses.

The retail franchise

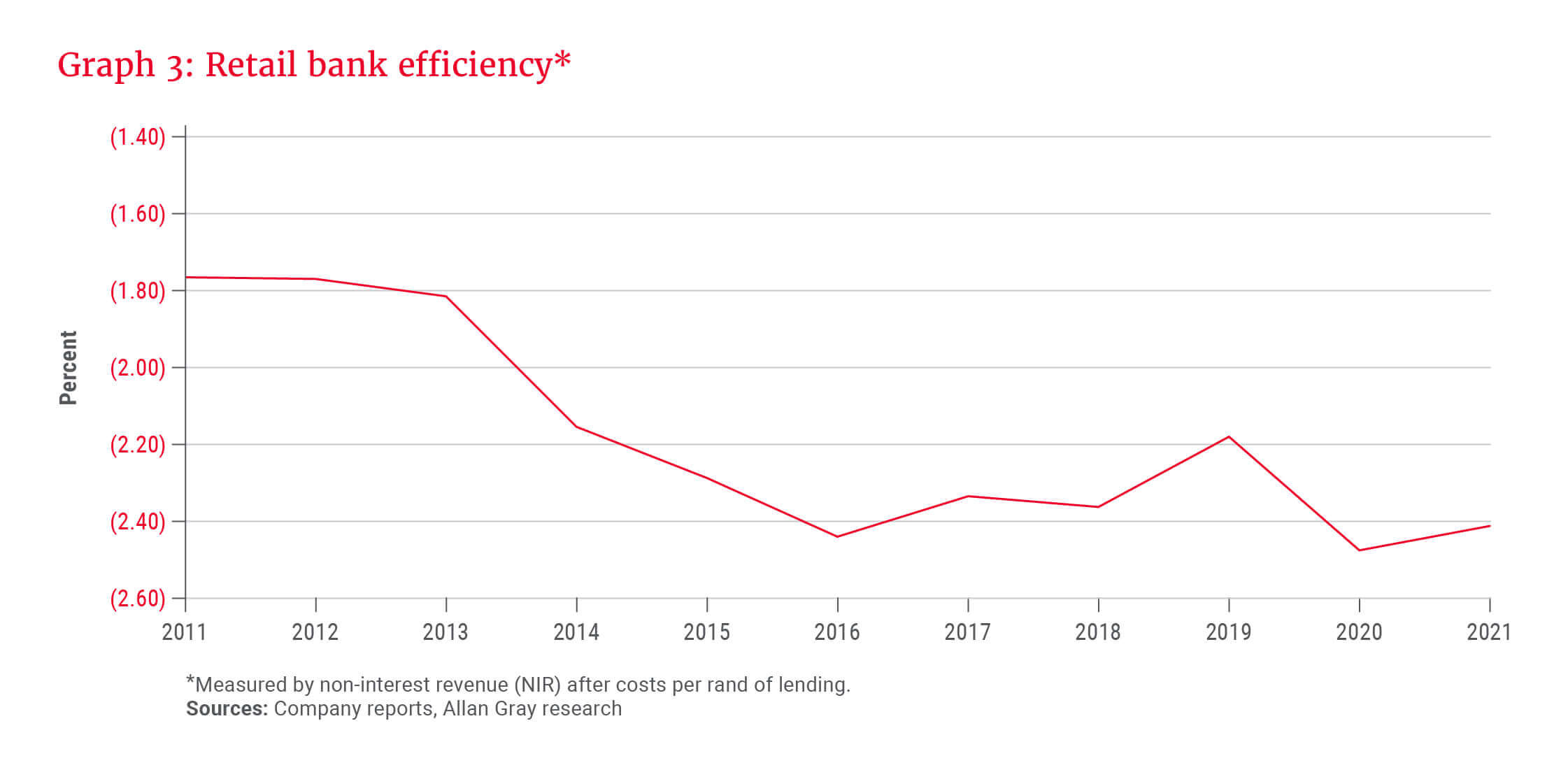

While the quality of the lending is important, the best banks have competitive retail franchises that maximise the efficiency of lending, especially in a macro-constrained lending environment. Graph 3 shows Nedbank’s efficiency of lending, measured by non-interest revenue (NIR) after costs per rand of lending. This had been on a sharp negative to 2016, but was improving until the start of COVID-19, as the business focused on efficiency. The bank managed to remove more costs than any associated revenue impact through investing in improved IT systems, with annualised IT project costs of R1.7bn compared to R3bn saved. This is in the context where the average fee rate per transaction in the South African banking industry is declining as online fees are often a fraction of what was charged in-branch, forcing cost-cutting to maintain transactional earnings.

Since 2015, Nedbank has reduced office space by 116 000 m2, and overall branch space by 45 000 m2 by closing a quarter of its branches. This has been achieved while maintaining the industry level of 85% of the target market having access to a branch within 30 km of where they live. Space reductions have been enabled by an increase in the digitally active client base from less than half in 2018 to 64%, which halved teller activity and the related cost base. Increasing digital connectivity allows the bank to provide wider services per client, which offsets some of the per-service fee pressure.

Doing well in an increasingly competitive retail banking environment requires efficient, easy-to-use technology. We think the market underestimates the benefit of the business’s steady investments in this area, but on the other hand, clients seem to appreciate this, as evidenced by improving customer satisfaction survey results and increased market share over the last two years.

The price you pay matters

As valuation-focused investors, we look for companies where market expectations mirror recent trends despite evidence of green shoots. While there are always tail risks associated with investing in banks, we think Nedbank-specific risks are being overpriced and that the increasing efficiency of Nedbank’s retail business will likely be a driver of value.

… the increasing efficiency of Nedbank’s retail business will likely be a driver of value.

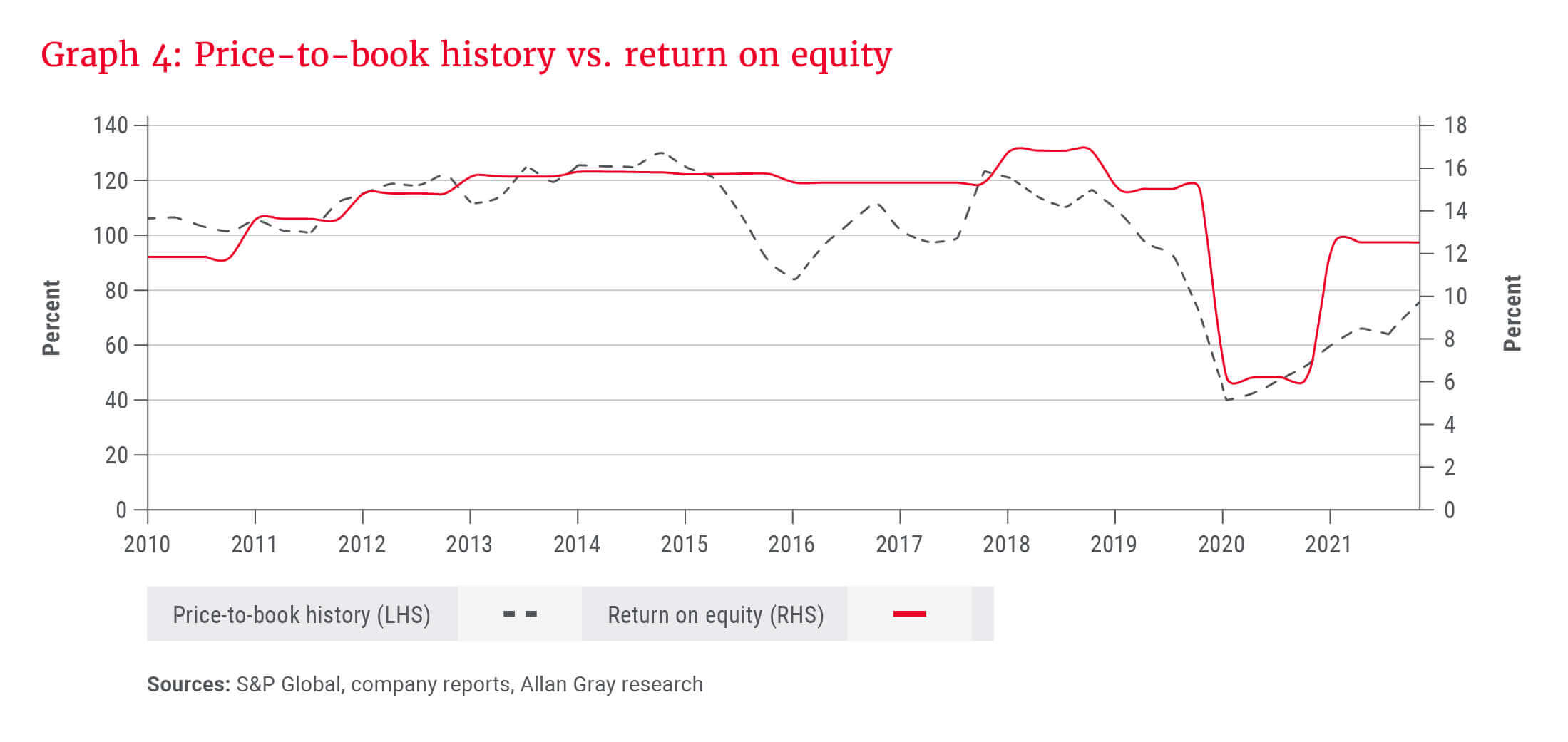

As a simple rule of thumb, the multiple of book value that investors are willing to pay for a bank is determined by its return on equity (ROE). Graph 4 shows how this relationship has held over time, with the price-to-book ratio shown as a percentage of the long-term average multiple. We think there is upside to current ROEs, which should drive a higher valuation multiple, with Nedbank currently trading at a discount to both its peers and its own history.