Tamryn Lamb looks at the important role balanced funds have played in your portfolio over time, the returns they have generated and the variability of these returns. Given the flexibility granted to invest a greater percentage offshore, she investigates how their role may evolve. Tamryn also discusses how Allan Gray and our offshore partner, Orbis, are set up to navigate this change, and how the Allan Gray Balanced Fund is positioned in this highly uncertain environment.

Balanced funds have been an important part of the South African savings landscape for many years. When we launched the Allan Gray Balanced Fund in 1999, multi-asset equity funds represented approximately 6% of the overall unit trust industry, but grew steadily over the next 10 years to reach around 25% in 2010, and just under 40% at the end of 2022. Multi-asset high-equity funds, or balanced funds, represent over half of this category and were a key part of this growth.

These funds have become a highly effective way to access growth assets through investing in a diversified portfolio, managed to comply with the retirement regulations laid down by the Pension Funds Act. This has solidified their role as a critical building block in retirement saving solutions.

How have balanced funds, including the Allan Gray Balanced Fund, delivered for clients over time?

Real returns from balanced funds have averaged approximately 3% over the last 10 years, and 5% over the last 20. However, despite the growth in the category, there are few funds with very long-term track records. Morningstar tracks the performance of over 200 funds, but there are only 12 funds with a 20-year track record.

We do not take our responsibilities of investing your savings lightly, and we will continue to work tirelessly to ensure that your trust is well placed.

The Allan Gray Balanced Fund (“the Fund”) has delivered real returns of 4.4% and 7.9% over a 10- and 20-year period. Over the last year, the Fund returned 8.1% relative to a sector average of 0.1% – which was pleasing, given 2022 was a year when real returns were very difficult to achieve.

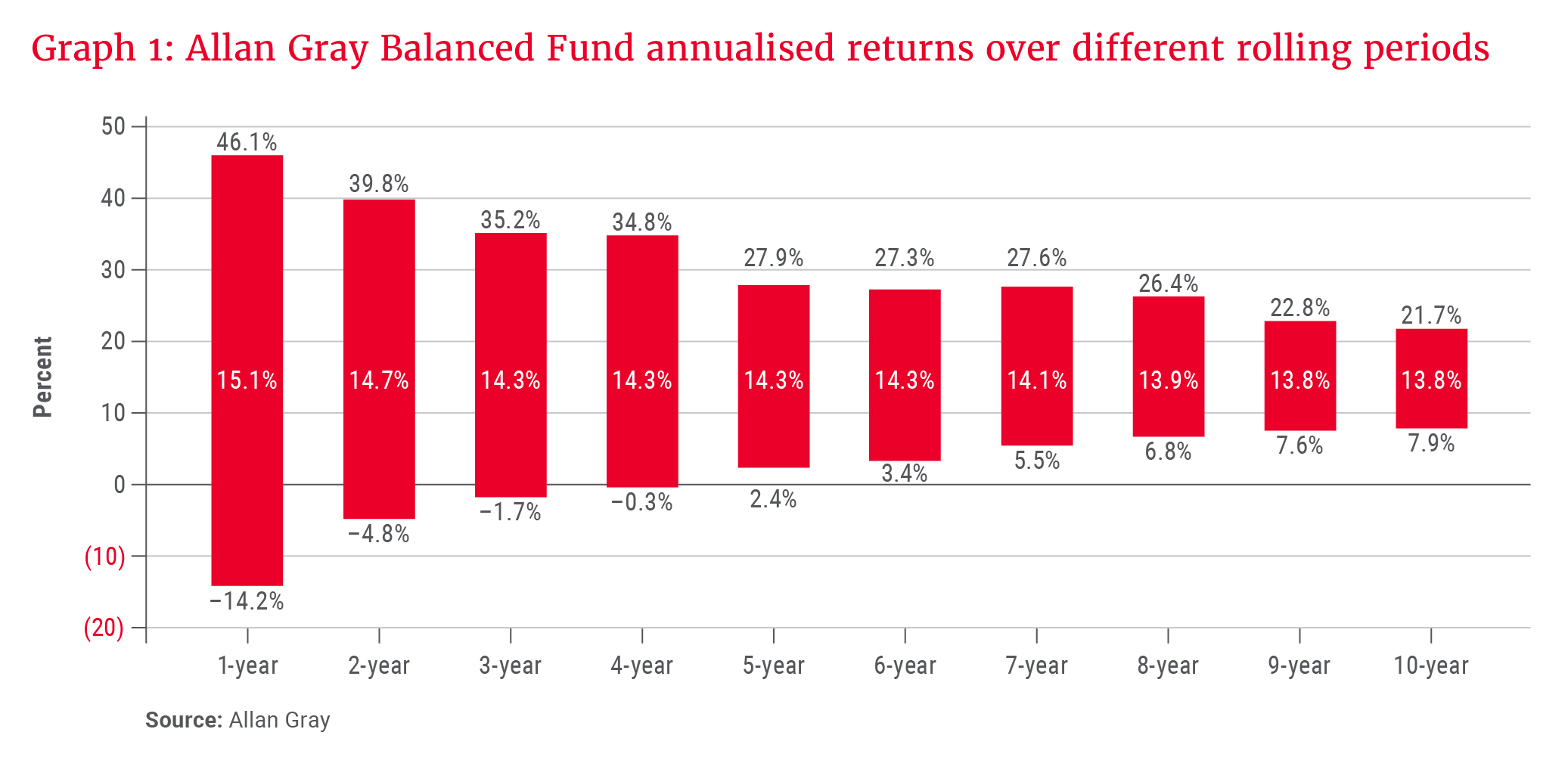

Since its inception and when measured using five-year rolling returns (shifted monthly), the Fund has performed better than its peer benchmark 93% of the time. While this represents a good outcome for clients who have remained invested, it does not adequately convey the bumpiness of the ride. We view this volatility in performance as an expected and natural outcome when your approach is to invest differently from the benchmark.

Graph 1 is a useful illustration of this feature. It shows the range of absolute annualised returns achieved over different rolling periods (shifted monthly). Over one year, the best-performing period has been 46.1% and the worst -14.2%. This can be uncomfortable, as was experienced in 2020. However, as you extend your time horizon by remaining invested in the Fund unsurprisingly, the range of returns you experience narrows. Over all one-year periods, the Fund has delivered positive returns 91% of the time. Over five-year and longer periods, however, it has always delivered positive returns. We believe this illustrates the benefit of our investment approach, which aims to limit the impact of losses while focusing on generating good long-term returns.

Foundation for ensuring we can deliver sustainable performance

When reflecting on a manager’s track record, two questions clients should ask are whether this performance is sustainable, and what has changed relative to the past.

At Allan Gray, we believe our organisational structure and the fact that we are privately owned are key to sustaining our ability to generate outperformance for clients over the long term. Fundamental to this structure is the concept of aligning our interests with those of our clients.

… we believe our organisational structure and the fact that we are privately owned are key to sustaining our ability to generate outperformance for clients over the long term.

In a world where incentives matter, one way to achieve alignment is through well-designed performance fees. A well-designed performance fee is one that varies up and down with performance, i.e. the performance component is both a positive and a negative. This way, the risk that clients pay fees for a service they don’t receive (the “fee risk”) is minimised. Conversely, if we don’t deliver long-term performance for clients, it materially affects the profits of the firm and, by extension, senior decision-makers who share in the profits.

A performance fee that adjusts to the downside also helps cushion the impact of any underperformance clients experience and helps ensure that fees paid over the lifetime of their investments correspond to the value they receive. Importantly, while we favour well-designed performance fees, this is not intended as a defence of all performance fee structures, nor as an indictment of all fixed-fee structures. Both structures can make sense under different circumstances.

How might the future be different? Navigating the additional flexibility to invest offshore

One way the future will be different from the past relates to the changes to the limits governing how much can be invested in foreign assets. In February 2022, balanced funds were given an injection of flexibility when the South African Reserve Bank changed the offshore investment limits from the previous 30% in foreign securities and an additional 10% in Africa ex-South Africa, to a combined 45% for all foreign investments outside South Africa. While technically this represents an increase of only five percentage points – from 40% to 45% – most funds had a relatively small exposure to Africa, given the liquidity constraints in the region, so this is a bigger relaxation than it may at first seem. Naturally, this has prompted questions about how funds will navigate these changes.

As investors, we prize flexibility and welcome the additional opportunity to diversify on our clients’ behalf. Greater flexibility should also mean more opportunities to be different from the peer group, which is likely to mean a higher dispersion in returns across funds in the industry.

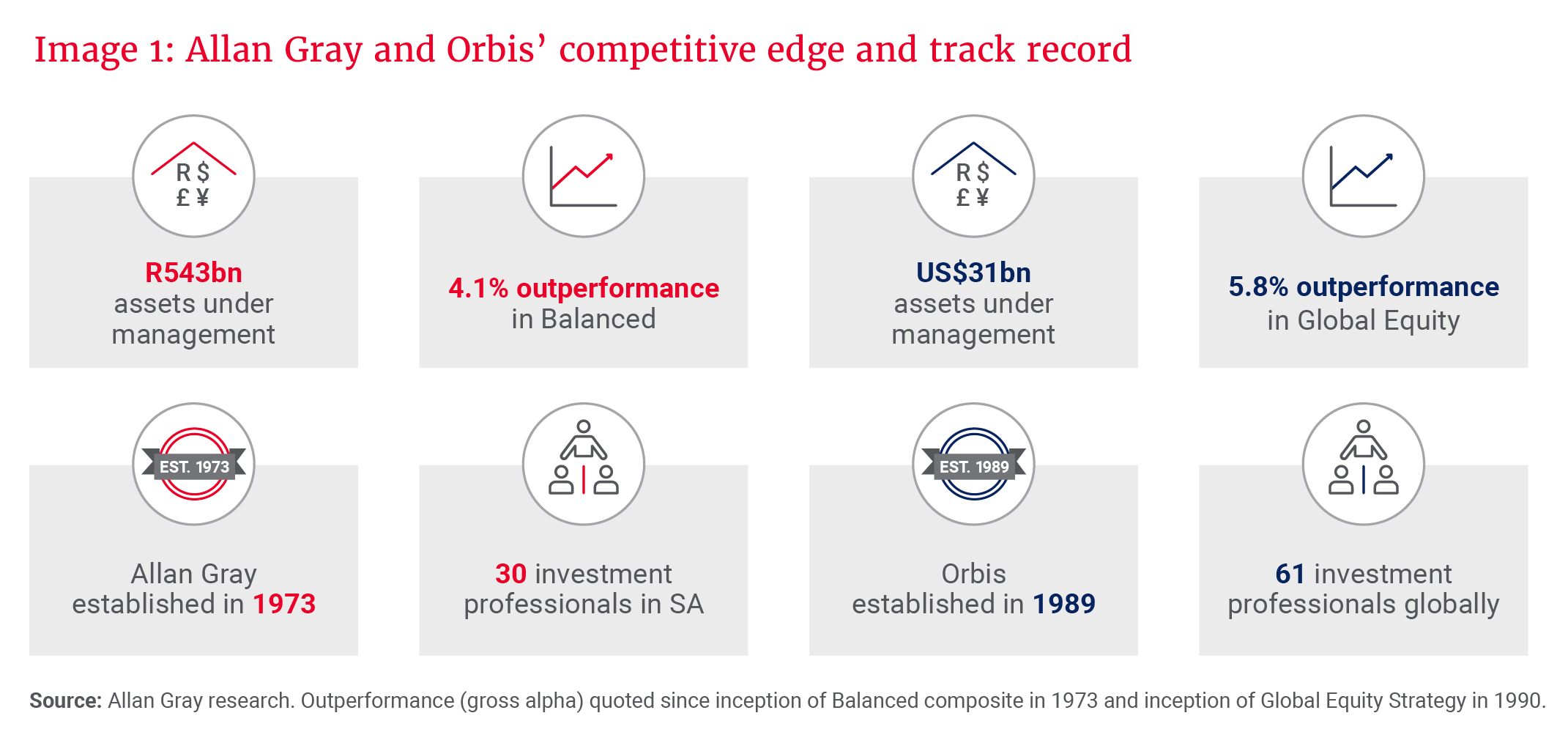

Like with any tool in a portfolio manager’s toolkit, it is important to ensure that it is seamlessly integrated into a tried-and-tested process, and to remain disciplined in execution. Allan Gray and Orbis have deep local and global investment capabilities, with long-term proven track records in each, as well as in combining these capabilities effectively to deliver global multi-asset solutions for South African clients (see Image 1).

2023 marks the 50th year since Allan Gray began in South Africa, and Orbis has been managing global securities since 1990. These independently run investment capabilities are joined by a common founder and ultimate owner, and a shared investment philosophy and approach.

Over our history, several generations of portfolio managers have been responsible for managing our clients’ capital; investing in our people is therefore also important to our long-term success. With just over 60 investment professionals globally and 30 in South Africa, we are well placed to cover the global universe and continue to develop the next generation of stockpickers. This research engine has helped us build a competitive advantage over time. By way of example, over the last 10 years, the Allan Gray and Orbis investment teams have written approximately 4 200 reports on South African, African and global businesses.

As investors, we prize flexibility and welcome the additional opportunity to diversify on our clients’ behalf.

We believe our bottom-up investment approach is ideally suited to navigating these latest changes, given our ability to have a holistic view across asset classes and exposures, and the importance we place on managing the risk of permanent capital loss in our funds. Rather than a top-down view on whether we should invest in equities or bonds, we focus on assessing the relative attractiveness – from both a risk and reward perspective – of the underlying security exposures. Should you own banking shares or SA bonds? Will Glencore outperform cash?

With a greater ability to invest offshore, we have more opportunities to compare against and diversify from the idiosyncratic risks that are ever-present in a market like South Africa.

Of course, as many of you know, the South African market is not as local as one might think: Over 70% of the earnings from South African-listed businesses are derived offshore. Therefore, deciding to invest in Philip Morris instead of British American Tobacco (BAT), or Vale instead of BHP Billiton, will not materially improve the diversification of the portfolio as the companies have similar risk and earnings profiles. It may improve the return prospects of the portfolio, of course, if one of these businesses were to trade on an undeservedly cheap multiple relative to the other. The JSE is also under-represented in sectors like technology, pharmaceuticals and certain consumer goods and services, and having increased offshore exposure allows us to include such companies, should we believe they are attractive relative to other opportunities.

We are proud of our history, but acutely conscious of not resting on the laurels of those who came before us.

Finally, we know that the world today looks like an uncertain place – locally and globally. Our response to concerns about this would be that the future always looks uncertain. As Rory Kutisker-Jacobson notes in our December Balanced Fund factsheet commentary, history has shown that trying to predict the exact path the future will take is not a great investment approach. Rather, we view the future as a range of possible outcomes, and the greater the uncertainty or risk, the wider that range will be. We spend our time ensuring the portfolio is positioned to do well within this range, focusing on the balance between the price we pay, investor expectations and ensuring we don’t get whipsawed by extreme events, big dislocations in asset prices or tail risks.

We don’t know what tomorrow’s headlines will be, but we have conviction that today’s positioning helps us protect against risks (local and foreign) and inflationary concerns and should enable our clients to capture the upside in the assets we think are undervalued.

Building and maintaining trust and confidence

As we enter our 50th year, we are reminded that complacency in our industry is a killer. Our founder, Allan W B Gray, was often heard saying: “We recognise that we must earn our clients’ trust and confidence, for without that our firm cannot, and should not, survive.”

We are proud of our history, but acutely conscious of not resting on the laurels of those who came before us. Trust in this business can be hard won, and easily lost. We do not take our responsibilities of investing your savings lightly, and we will continue to work tirelessly to ensure that your trust is well placed.