In his annual president’s letter, Adam R. Karr, from our offshore partner, Orbis, discusses the performance of the Orbis Strategies during 2023, looks back at the investment backdrop over the same period, and glances ahead to what the future may hold.

“It is never intuitive how big something can grow with compounding over time from a small beginning.”

– Morgan Housel

Our founder, Allan Gray, set out to “invest differently” 50 years ago. In an industry dominated by salespeople, Allan took a contrarian approach. He built Allan Gray Investment Counsel on a philosophy of fundamental, in-depth research. And rather than charge commissions, in sharp contrast to industry convention, he charged fees based on the value added or alpha delivered. Allan’s mantra was that investment services should be “bought, not sold” – and he believed that the firm should always put clients first.

The results have been astonishing – a $1 000 investment with Allan Gray Investment Counsel in 1974 would be worth $1.2 million today. In November, I was in Cape Town to celebrate the firm’s 50th anniversary and had tears in my eyes at dinner reflecting on the tremendous impact of what Allan made possible. It is a testament to his enduring investment philosophy, but also to the power of alignment, patience, and a long-term perspective.

In recent client presentations, I have been speaking about the “Power of n”:

Returns to client = Invested capital x Rn

In managing your capital, we obsess over maximising your returns, or “R” in the equation above, without assuming greater risk than the market. Although good returns are critical, the true magic comes as “n” – the investment holding period – gets larger and returns compound over time. Our hypothetical investor, who started in 1974, had $28 000 in 1989 when Allan departed to launch Orbis – an impressive 28-fold return. The vast majority of their $1.2 million in wealth today, however, was compounded after Allan was no longer managing their savings. It is impressive to build a track record of excellent performance for a period, it is quite another feat to build a firm that can endure and deliver world-class results over generations.

We have big shoes to fill.

More important than the short term is a resolute focus on our North Star, which is to deliver world-class client alpha for you over the long term.

Looking back at performance

In 2023, client capital appreciated a robust 18.7% on a firm asset-weighted basis. On a relative basis, the Orbis Strategies slightly outperformed their respective benchmarks by 0.1% after fees and expenses, also on an asset-weighted basis. Over the past three years, we have generated 1.7% of annualised alpha on a firm asset-weighted basis and all our Strategies have outperformed their respective peer group averages over this time.

More important than the short term is a resolute focus on our North Star, which is to deliver world-class client alpha for you over the long term. And here we have more work to do, but looking more deeply at our recent results, I am encouraged by our progress and believe it will compound over time.

First, our regional Strategies delivered world-class performance. Indeed, the big story in 2023 was the performance of our Japan and Emerging Market Strategies, which both delivered more than 5% alpha while also contributing several big winners to our various Orbis Strategies. It has been gratifying to see our regional teams amp up the focus in their respective areas and harvest the compelling opportunities we have identified in the regions. Our Optimal (US$) Strategy, which hedges out stock market exposure, delivered a 5.7% absolute return after fees, demonstrating the value to be derived from superior stock selection as well as offering a compelling alternative to cash and bonds.

Despite limited exposure to the heady drivers of 2023 … we delivered a strong 20.8% return in Global through superior idiosyncratic stock selection.

Second, it is important to examine the context in which these results were delivered, particularly for our flagship Global Equity Strategy, which delivered a 20.8% return in 2023 but lagged the MSCI All Country World Index return by 1.2%. In Global, several stiff headwinds worked against us. We owned just one of the so-called “Magnificent Seven” stocks – Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia and Tesla – that propelled nearly all the benchmark’s concentrated gains. We were underweight the US market and US dollar, while overweight the dirt-cheap Japanese yen. And we had near our highest exposure to “value” shares since inception. The latter was especially painful with the MSCI Growth Index outperforming the MSCI Value Index by a staggering 22% in 2023.

Despite limited exposure to the heady drivers of 2023 – the “Magnificent Seven”, the US market and growth stocks – we delivered a strong 20.8% return in Global through superior idiosyncratic stock selection. Our internal performance attribution team notes that the realised results in the Strategy were well above average compared to the distribution of outcomes and opportunity set of simulated portfolios. In other words, Global’s performance in an adverse context gives me confidence in the actions taken over the past two years and our ability to deliver. With this foundation, we remain laser-focused on compounding this progress.

Looking back

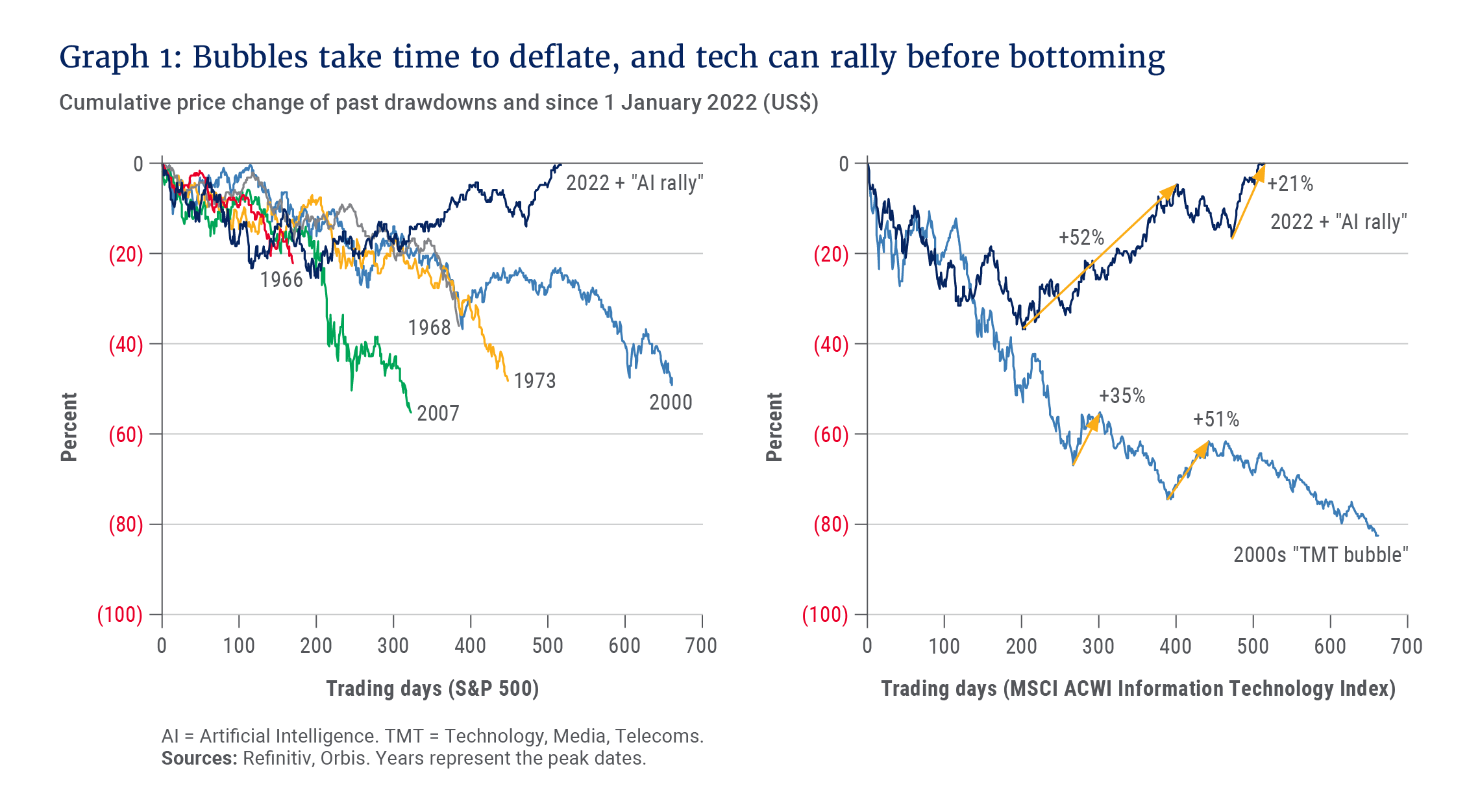

I stated last year that markets were at an “awkward juncture” – no longer a bubble, but nowhere near a bottom. This remains the case today. A few weeks ago, all our senior investors at Orbis came together to reflect on the year and to identify where we can improve. One exercise we did was to identify surprises and then suggest potential lessons and actions. Looking back, beyond the world’s obsession with Taylor Swift, 2023 contained several meaningful surprises:

The “most anticipated recession in history” did not materialise. The goldilocks US economy held up much better than most were expecting, shrugged off a banking crisis earlier in the year, and markets ended quite optimistic about a soft landing.

The “Everything Bubble” did not burst. Instead, we got a massive stimulus catalysed by the ascendance of generative artificial intelligence. And as we closed the year, the US market was getting another boost from the Federal Reserve, which appears to be signalling an end to their interest rate tightening cycle. Growth stocks soared and the “Magnificent Seven” almost single-handedly propelled the benchmark to its previous peak.

We did not repeat the pattern of the 1970s – at least not yet. The market largely absorbed and looked through higher interest rates and inflation. The sharp rise in the cost of money and its impact on valuation multiples has been more muted than many feared, although it did have a severe impact on the renewables sector (including our holdings in AES and Sunrun).

… we focus on what we can control and emphasise playing to our strength, which is in-depth, fundamental company research.

Importantly, history shows that this non-linear pattern of an unwinding bubble, like we saw in 2023, is not unusual. Markets never move from peak to trough in a straight line. Often there are sharp counter-trend rallies along the way, and the process can take several years. See Graph 1.

One lesson, in the words of beloved New York Yankees legend Yogi Berra, is that “it’s tough to make predictions, especially about the future”. As such, we focus on what we can control and emphasise playing to our strength, which is in-depth, fundamental company research. We seek to understand the intrinsic value of a business and its drivers better than most, and then buy at a discount. This helps us to look through the macro noise and end up with a portfolio that has a margin of safety no matter what fortune throws our way. Some notable examples from 2023 were positions in Intel, Westlake and Constellation Energy that delivered idiosyncratic alpha despite a surprising and tumultuous macro environment. This focus on differentiated insights is the heart and soul of our investment process.

At the same time, we must be open-minded and adaptive. We must constantly question our assumptions and be mindful of the environment in which we operate to adapt the portfolio as appropriate. Our research always starts with bottom-up analysis, then we cross-check against the bigger picture. In that spirit, one hazard area where we have increasingly dedicated efforts is on the geopolitical front. It looks to us like we are seeing a fundamental change in the world order – in Europe, the Middle East and Asia – and we are dedicating efforts to sharpen our understanding. And on the economic side, should the Federal Reserve fail to stick the coveted “soft landing” and be forced back into a period of unparalleled monetary intervention, we must understand the implications and be ready to act accordingly.

Looking ahead

History rarely repeats but often rhymes. And the concentration we see in today’s stock market indices is reminiscent of the “nifty fifty” bubble that was collapsing 50 years ago when Allan started in South Africa. Like then, valuation spreads are wide versus history and, thus, we believe it will be a rewarding time for active, value-oriented stockpicking.

We also think it is a critical time – in the words of the late Charlie Munger – to simply avoid the stupid mistakes. One of the easiest ways to lose money is to buy something for more than it is worth. In this case, that is the above-average downside risk embedded in owning an index full of market darlings with high expectations.

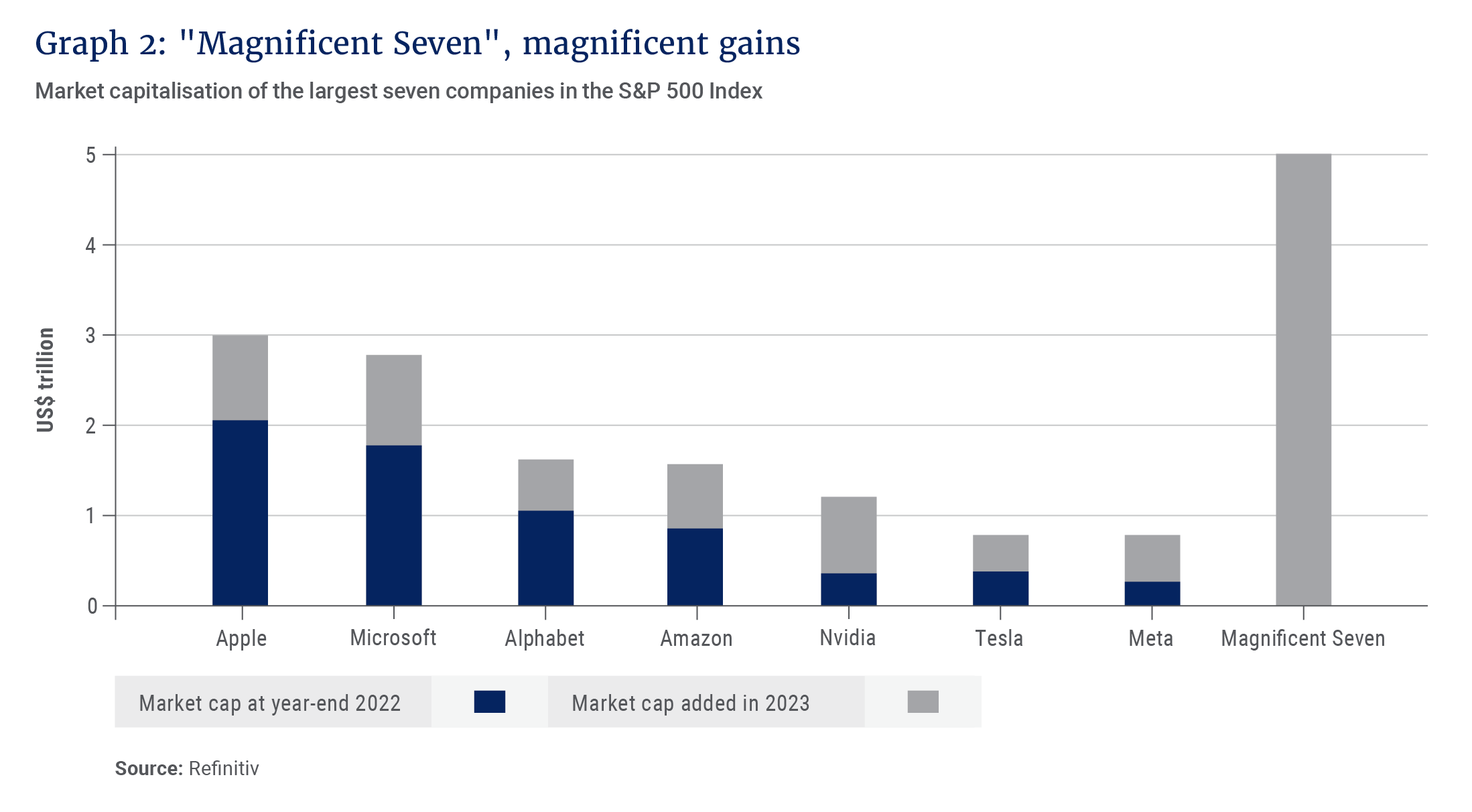

Let’s consider the “Magnificent Seven” more deeply as their massive appreciation this past year in percentage terms does not tell the whole story. Given the sheer size of their market capitalisations at the start of 2023, the incremental market cap added in the year was astonishing. Collectively, the “Magnificent Seven” added about $5 trillion in market capitalisation over the past year – roughly equivalent to the entire Japanese stock market. (See Graph 2.) Some of these gains are justified by the superior fundamentals that these companies have produced – but there is a natural limit to how long it can continue at this staggering pace. And to continue delivering attractive returns, they will need to add many more “Japans” worth of market value in the years to come. Possible, but the odds don’t strike us as compelling.

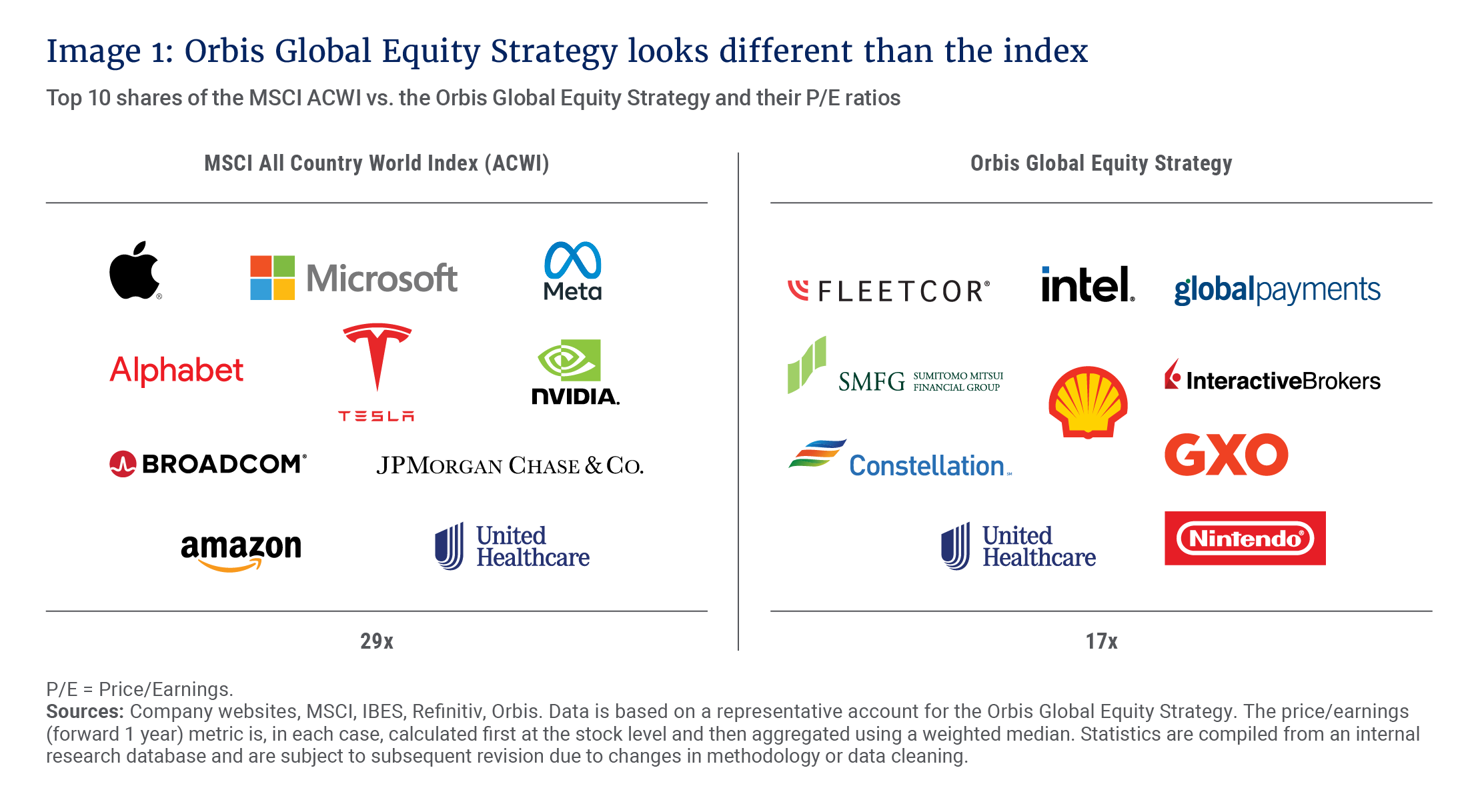

Historically, similar periods have ended badly. Expensive stocks lost 40% of their value following the Japan bubble in the late 1980s and 50% of their value following the dot-com implosion. Investors can look foolish for not owning the winners in the short term – and “FOMO” can be overwhelming. But paying too much for an asset with high expectations can be a recipe for disaster. We would rather own first-rate companies like Fleetcor at 16 times earnings and avoid those like Tesla at a frothy multiple of 80 times earnings. That is just one example, but it is exactly what we are doing across the portfolio in Global today. See Image 1 for more examples.

Our founding philosophy is contrarian-minded – that is to “invest differently”. There are times when these differences are more extreme than others, and today is one of those times. We own a portfolio of stocks that looks quite different to our peers and to an expensive index. We think our companies offer an attractive set of fundamentals and trade at a sizeable discount to the index. And we are excited by the opportunity this offers.

“A lack of patience changes the outcome.” – Shane Parrish

Our task is to remain patient and “stay on the bus”. I have said to our younger analysts that “the magic” is often found in the tail or last 10% of the research – that is pushing the work hard enough and far enough that you get to a variant insight. The same premise holds with investment compounding. The power of small gains compounded over time is dramatic. The longer the time horizon, the larger the success.

Always traveling

One of my favourite mantras from Allan was “always traveling” – a mindset that I interpreted as being curious, constantly learning and always striving to improve.

Importantly, our focus on patience and “staying on the bus” does not mean being complacent or stubborn. We are compulsive about continuous improvement. This DNA is from Allan and Will, who pioneered many of the structures and tools that we use today. Allan started with paper, pencil and rudimentary quant methods; today we are investing to stay on our front foot. Specifically, we are developing new portfolio construction and risk tools as well as using AI-enabled technologies to exploit our rich set of proprietary data from over 30 years of investment decisions tracked by our paper portfolio system. We also hired our first Chief Technology Officer and a new head of Quant and Data Insights; and we aim to accelerate our technology initiatives.

We continue to make progress simplifying and building for the future with a relentless focus on the initiatives I outlined in previous letters. First, we demonstrated more agility and accelerated the velocity of capital movement in Global. This includes directing capital to Japanese and Korean banks, which trade at a fraction of book value and are benefiting from an improving rate and capital cycle. We also did a better job seeing the whole, shifting capital away from areas of concern such as China. Second, we have aligned and re-organised the structure of our global research team in London, which intensifies our sector focus, and we introduced process enhancements including a new and more robust framework for assessing risk when recommendations are formally debated. It has also been inspiring to see such a strong bench of talent stepping up, embracing new responsibilities, and making a difference for clients.

This is our charge at Orbis – compounding small incremental improvements over time into world-class results.

Most of our efforts are less transparent and part of the daily grind. It is these small, almost imperceptible efforts that add up to a real difference over time when executed consistently. My colleague at Allan Gray Limited, Radhesen Naidoo, wrote about the power of 1%, which captures this well. Fascinatingly, he noted that achieving a long-term track record in investing has much in common with success in professional tennis. Both disciplines are about patience, hard work, and a commitment to refining your unique skill, as well as resisting the urge to make impulsive decisions.

Radhesen crunched the numbers of Roger Federer’s success on the tennis court. An interesting aspect of professional tennis, like investing, is that you can compound substantial advantages over time by simply being marginally better. There are many ways to analyse professional tennis players, but one that stands out and is easy to interpret is the percentage of points won compared to the percentage of matches won.

Federer started in 1999 ranked outside the Top 100. He won 49% of all points played, and 43% of all his matches in that year. In 2001, he was winning 52% of all points, and 70% of his matches. By 2005, he was dominating the game, winning an incredible 95% of his matches, despite winning only 55% of all points. Put differently, the improvement in points won from 49% to 55% catapulted him to world #1. He still lost 45% of the points played, but the marginal improvement in points won had an exponential impact on the number of matches won. More remarkable is that Federer continued to play at a high level for the rest of his career, which means he consistently improved and adapted as his competition evolved as well.

This is our charge at Orbis – compounding small incremental improvements over time into world-class results.

Our leadership and team

The pace of change across the firm over the past two years has accelerated. On the client and operating side, under Darren Johnston’s leadership, we undertook an intensive review of our processes, key operating systems, and alignment. The review affirmed the quality of our systems and people, but also highlighted opportunities to advance that we are actively seizing. Our investment in people is progressing as well. We implemented a new career pathways framework for our investment analysts and welcomed important new technology leaders as noted earlier.

As we look back on this year, Will, Darren and I want to share a full-throated “shout-out” to the team. Particularly, we want to deeply thank and acknowledge our general counsel, James Dorr, who retired from Orbis this year after 26 years of incredible service. We will miss his razor-sharp intellect, keen business acumen and passion for Orbis. James leaves the firm in steady hands, with a strong legal team led by David Gasperow

Our team and individuals like James are what propels our flywheel. It is energising to lead such talented and committed colleagues. I am grateful.

Conclusion

As always, I will close by reaffirming my commitment to you:

Our firm’s success begins and ends with delivering best-in-class investment performance. As it was on day one, I am certain that what we aspire to achieve will not be easy. But how we show up is in our control and we are determined to deliver. Here is my commitment to you: relentless focus; transparent and direct engagement; entrusting others; a culture of inclusion; the courage to be different; an appetite for feedback; and a willingness to change what isn’t working. You can expect me to do my part and to ensure that others do theirs. And we will keep showing up every day for you.

Thank you for entrusting us. With your support, we will harness the power of n.